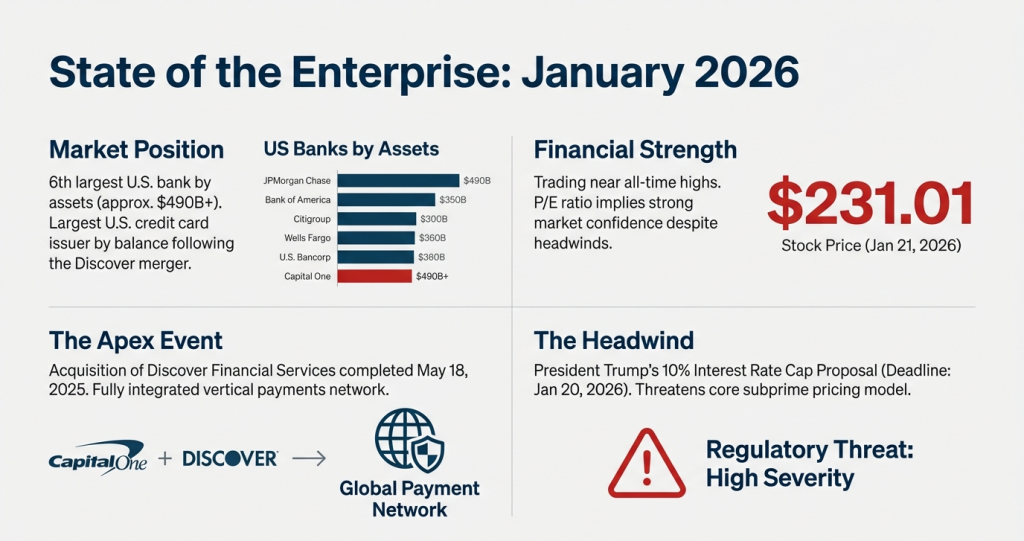

Company Description

A financial giant leading in U.S. credit cards, auto lending, and digital banking. It is currently navigating a high-volatility environment for unsecured consumer credit.

Current Stock Price

~$239.14

Market Capitalization

~$152 billion

Valuation

Trading at a forward P/E of ~13.6x. The market has assigned a higher multiple due to dominant scale and high-single-digit revenue growth.

Reporting its Q4 2025 results on Jan 22, COF showed robust revenue of $15.4 billion (+48% YoY, though this reflects a low 2024 base). The Net Interest Margin remains a powerhouse at 8.36%, significantly higher than traditional regional banks, though it is slightly down from the 8.43% adjusted peak earlier in the year.

Credit normalization is the primary headwind. Net charge-offs rose to $3.5 billion in the most recent reporting period. However, management offset this with a $760 million loan reserve release, signaling that they believe the “peak” of delinquency is nearing or has passed.

Reasons to Pass on COF

- Unsecured Exposure: Unlike BANR or GSBC, COF is highly sensitive to the “bottom 50%” of US consumers, where delinquency rates are rising fastest.

- Operating Expense Growth: Operating expenses jumped 22% recently, limiting the “earnings leverage” typically expected from such a large revenue base.