Shares of Cencora, Inc. (NYSE: COR) fell 8.8% to close at $329.85 on Wednesday, as investors weighed a marginal revenue miss and a sharp decline in international operating income against an improved full-year operating outlook. The stock gapped down at the open despite an adjusted earnings beat, marking its steepest one-day decline in over a year.

Company Description

Cencora, Inc. is a global pharmaceutical solutions company that sources and distributes brand-name, generic, and specialty pharmaceuticals. The company provides services to healthcare providers and pharmaceutical manufacturers, including clinical trial logistics, market access consulting, and specialty physician services. It operates through two main segments: U.S. Healthcare Solutions and International Healthcare Solutions, following its strategic pivot toward high-margin specialty healthcare platforms.

Market Performance and Valuation

- Current Stock Price: $329.85 (Close Feb 4, 2026)

- Market Capitalization: Approximately $64.05 billion

- 52-Week Context: The stock has traded between $237.71 and $377.54 over the past year. Wednesday’s decline wiped out approximately $6 billion in market value.

- Valuation: Cencora trades at a forward P/E of 18.7x based on the $17.60 midpoint of its fiscal 2026 guidance. This multiple remains above its historical five-year average, reflecting the market’s premium on its expanding oncology and specialty medicine footprint.

Fiscal First Quarter 2026 Results

Cencora reported financial results for the quarter ended December 31, 2025:

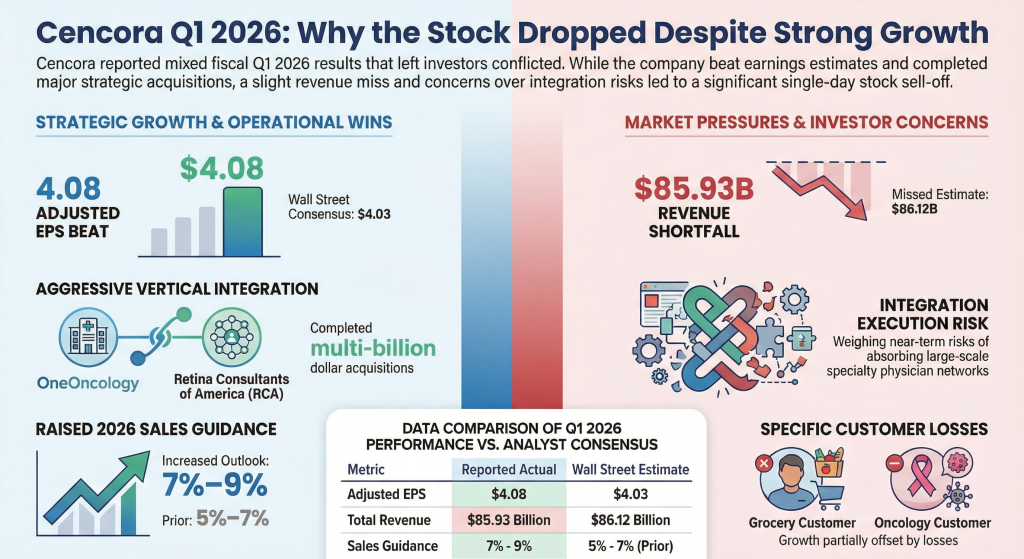

- Revenue: $85.93 billion, up 5.5% year-over-year, missing the $86.03 billion consensus estimate.

- Adjusted Diluted EPS: $4.08, up 9.4% from $3.73 in the prior-year period, beating the $4.04 analyst consensus.

- Adjusted Gross Margin: Expanded 37 basis points to 3.48%, primarily driven by the Retina Consultants of America (RCA) acquisition.

- Segment Performance:

- U.S. Healthcare Solutions: Revenue rose 5% to $76.2 billion; operating income surged 21% to $831.3 million, fueled by strong demand for GLP-1 (weight loss) and oncology therapies.

- International Healthcare Solutions: Revenue increased 9.6% to $7.6 billion, but operating income fell 13.9% (down 17% on a constant currency basis) due to unfavorable manufacturer price adjustments in a developing market.

Updated 2026 Guidance and Forecasts

The company updated its full-year outlook to reflect the completion of the OneOncology acquisition:

- Operating Income: Growth guidance raised to 11.5%–13.5% (from 8%–10%).

- Revenue Growth: Raised to 7%–9% (from 5%–7%).

- Adjusted EPS: Reaffirmed at $17.45 to $17.75, with the midpoint of $17.60 falling slightly below the analyst consensus of $17.62.

- Interest Expense: Full-year expectation increased to $480 million–$500 million due to financing costs for recent M&A.

Macro Pressures and Risk Factors

- Geopolitical/International: Profitability in the International segment was hampered by the timing of regulatory price resets in Europe and developing markets. Management expects this to unwind but remains cautious on currency volatility.

- Tariff & Trade: While not a direct importer of finished goods impacted by current electronics tariffs, the company noted that global logistics costs for its World Courier business remain sensitive to trade policy shifts.

- Leverage: The company reported negative adjusted free cash flow of $2.4 billion in the quarter (seasonal) and has paused share repurchases to prioritize debt paydown after the OneOncology closing.

SWOT Analysis

| Strengths | Weaknesses |

| Leadership in specialty/oncology distribution (OneOncology integration). | Revenue miss highlights sensitivity to high-volume pharmacy volume shifts. |

| Robust U.S. operating income growth (+21% in Q1). | High interest expense ($480M+) weighing on net income growth. |

| Opportunities | Threats |

| Continued high demand for GLP-1 and immunology therapies. | Regulatory scrutiny of PBM/Wholesaler pricing and “clawbacks.” |

| Expansion of high-margin commercialization services for biopharma. | International operating income volatility and currency headwinds. |