Network gear maker Cisco Systems, Inc. (NASDAQ: CSCO) has made significant progress in its transition from a hardware company to a subscription business, in line with the rapid transformation the information technology market is witnessing. The recurring revenue model has been successful so far and is expected to gain traction this year as economic recovery picks up pace amid the COVID vaccination drive.

Supply Chain Woes

Revenues of the Silicon Valley tech firm grew in the April quarter after registering negative growth in the trailing five quarters, but the management expects margins to remain under pressure from supply-chain issues and elevated costs. The cautious outlook triggered a sell-off this week and the stock slipped. The weakness is expected to extend into the coming weeks, but the stock should recover in the long term supported by the underlying strength of the business. CSCO looks like a good bet for long-term investors.

Read management/analysts’ comments on Cisco’s Q3 earnings

The company expects to resolve the supply-chain issues to a large extent by revising existing arrangements with key suppliers, thereby gaining smooth access to important components like microprocessors. That will also ease the pressure from high costs related to shipments. Meanwhile, the recovery in enterprise spending, buoyed by market reopening and removal of virus-related curbs, will have a positive effect on top-line performance. In the most recent quarter, product orders grew at the fastest pace in a decade. Also, more than 80% of software revenue was in the form of subscriptions, indicating that the new model is gaining steam.

Internet for the Future

Earlier this year, the company closed its previously announced acquisition of optical networking solutions provider Acasia Communications for $4.5 billion, as part of the Internet for the Future strategy. Recent buyouts and diversification into new areas like cybersecurity and cloud applications have also created significant cross-selling opportunities.

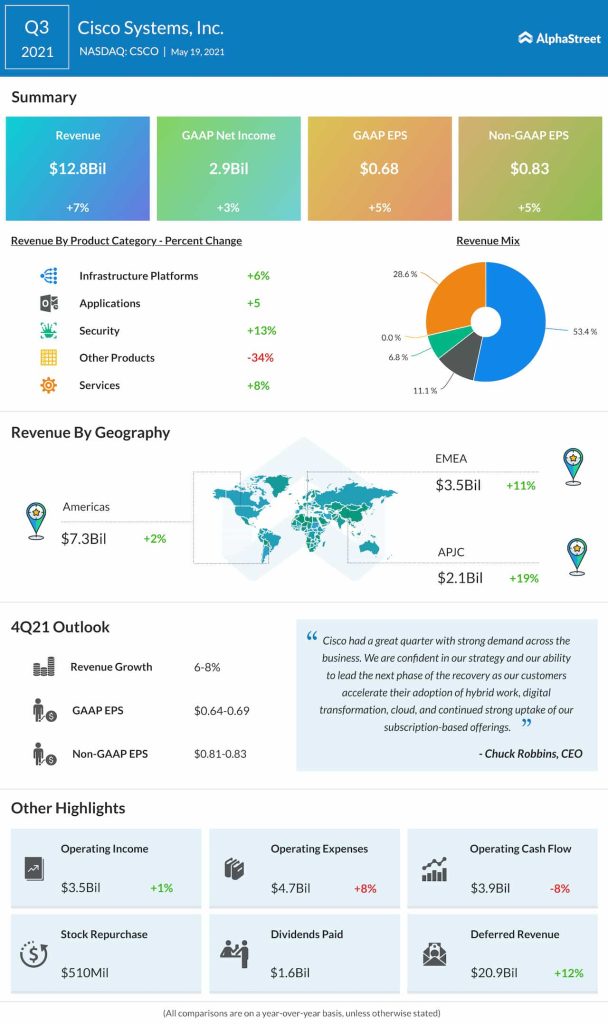

“The next phase of the recovery and the future of work will be heavily reliant on our technology. Cisco’s end-to-end portfolio will serve as the foundation for next-generation infrastructure solutions as well as cloud-enabled delivery models and innovation, allowing our customers to move with even greater speed and agility. This will require a significant investment cycle and reinforces the strength of our strategy while driving greater opportunity to create a world that is more connected, inclusive, and secure.” said Chuck Robbins, chief executive officer of Cisco, during his interaction with analysts at the third-quarter earnings conference call.

Top-line Rebounds

Ending a year-long streak of declines, revenues rose 7% annually to $12.8 billion in the third quarter, which translated into a 5% growth in adjusted earnings to $0.83 per share. The core operating segment —Infrastructure Platforms — expanded 6% and the services business, which accounts for 29% of total revenues, grew by 8%. The numbers also surpassed the market’s projection, but investors were not impressed by the management’s outlook guiding fourth-quarter earnings below the consensus estimate.

Key quarterly highlights from IBM’s Q1 2021 financial results

As a result, the stock suffered a big loss and continued the downtrend early Thursday, reversing a part of the recent gains. The shares are trading above their 52-week average, but well below the record highs of 2000. The stock has gained 18% since the beginning of the year, all along outperforming the S&P 500 index.