Cisco Systems Inc. (NASDAQ: CSCO) reported an 18% drop in earnings for the first quarter of 2020 due to higher costs and expenses. Despite the results exceeding analysts’ expectations, the company guided second-quarter earnings below the consensus estimates.

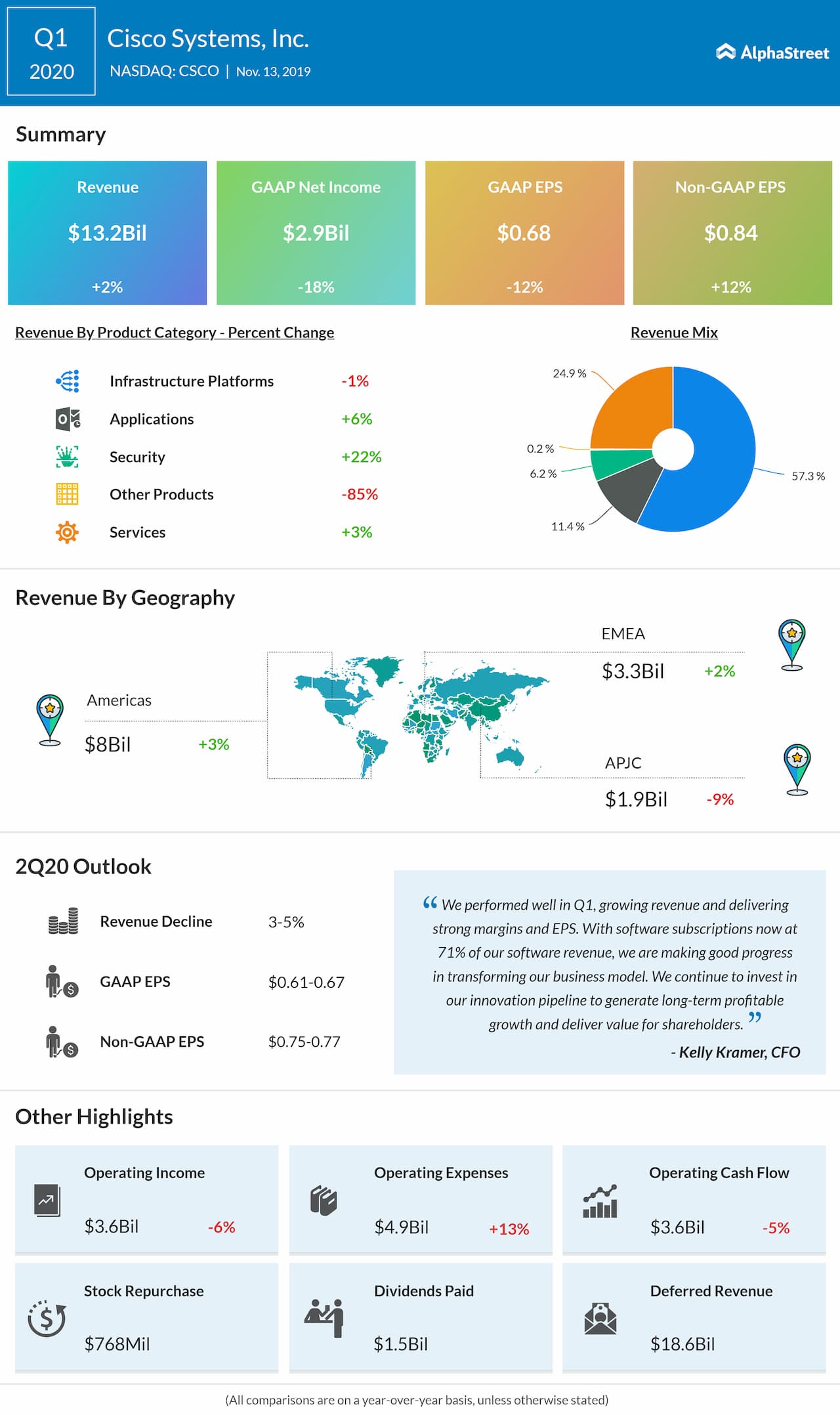

Net income plunged by 18% to $2.9 billion or $0.68 per share. Adjusted earnings increased by 12% to $0.84 per share. This is much better than the analysts’ expectations of $0.81 per share.

Revenue rose by 2% to $13.16 billion, which topped the consensus estimates of $13.09 billion. Product revenue rose by 1% and service revenue increased by 4%.

Looking ahead into the second quarter, the company expects revenue to decline in the range of 3% to 5% year-over-year, and earnings in the range of $0.61 to $0.67 per share. Adjusted earnings are anticipated to be in the range of $0.75 to $0.77 per share. Analysts expect earnings of $0.79 per share on revenue growth of 3% for the second quarter.

The cloud, Internet of Things (IoT), and security remained the high-growth businesses and Cisco has been investing in these heavily. The strategic deals, including acquisitions, turned out to be the breadwinner of its Applications and Security divisions.

For the first quarter, by geographic segment, revenues in the Americas and EMEA each was up by 4% while that in APJC declined by 8%. Product revenue was led by a 22% growth in Security and a 6% rise in Applications. However, Infrastructure Platforms were down 1%.

The company completed several acquisitions in the first quarter of fiscal 2020. In addition, in the fourth quarter of fiscal 2019, Cisco announced its intent to buy Acacia Communications, a publicly-traded fabless semiconductor company. The acquisition is expected to close during the second half of fiscal 2020.

Cisco has been transforming its business model from a hardware company to a networking service provider with the primary focus remained on software as a subscription. This is likely to increase customer monetization and recurring revenues. The transformation is expected to yield better returns in the future.