AlphaStreet Newsdesk powered by AlphaStreet Intelligence

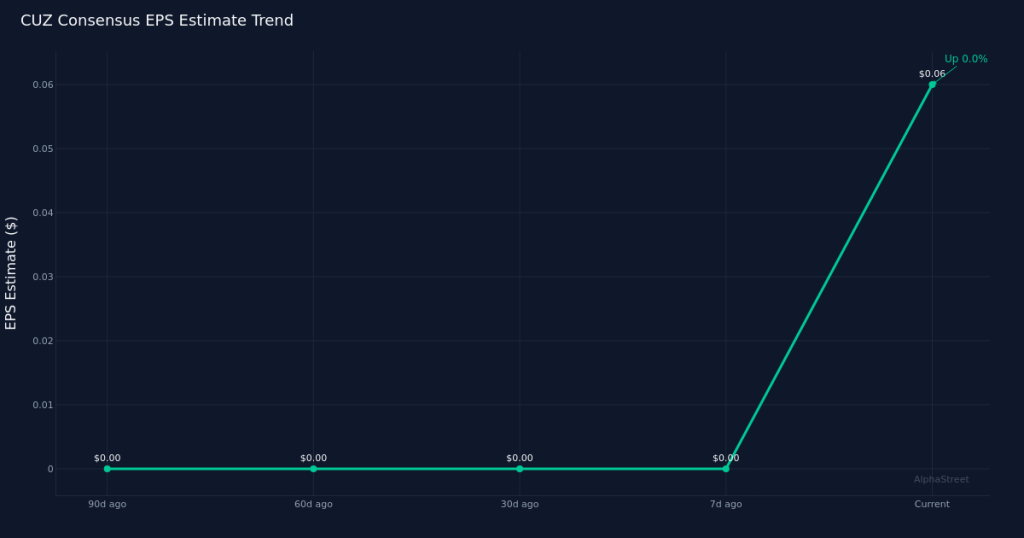

Wall Street expects a sharp year-over-year decline when Cousins Properties Incorporated reports first-quarter results on April 30. The lone analyst covering the office REIT ahead of the print expects earnings of $0.06 per share on revenue of $258.3M. Revenue estimates span from $252.9M to $268.1M, reflecting some uncertainty about top-line performance in what remains a challenging environment for office landlords.

The consensus represents a stark deceleration from year-ago profitability. In the first quarter last year, Cousins posted earnings of $0.12 per share on revenue of $243.0M, translating to an implied year-over-year EPS decline of negative 50.0% despite an implied revenue increase of positive 6.3%. That divergence—rising revenue paired with sharply lower earnings—points to margin compression and higher costs eroding profitability. The year-ago quarter generated net income of $20.9M on a net margin of 8.6%, providing a baseline against which investors can measure operational efficiency in the upcoming print.

The revenue growth story masks underlying profitability pressure. An office REIT posting modest revenue gains while earnings halve suggests several potential headwinds: lower occupancy and pricing power forcing concessions, elevated operating expenses as landlords invest to retain tenants, or higher interest costs as floating-rate debt reprices. The year-ago net margin of 8.6% offers a reference point, but without current guidance on margins or expense trends, investors will need to parse the line items carefully to understand whether the earnings decline reflects transitory costs or structural challenges in the office sector.

Office REITs face persistent occupancy and leasing headwinds that shape the operating backdrop. While Cousins focuses on Sun Belt markets that have shown relative resilience, the broader office sector continues grappling with elevated vacancy rates and tenants downsizing or delaying lease commitments. The revenue estimate implies modest organic growth, but the composition matters: whether gains come from rent escalations on existing leases, new leasing activity, or contributions from acquisitions will signal the health of the portfolio. Without prior quarter data available, investors lack a sequential performance snapshot, making the year-over-year comparison and management commentary on leasing velocity and tenant demand critical.

The stock’s positioning heading into the report will influence how investors interpret any variance from consensus. Without current price or range data available, the setup remains opaque, but office REITs broadly have faced valuation pressure as investors reassess the sector’s structural trajectory. A single analyst covering the name suggests limited buy-side attention, which can amplify volatility on earnings surprises in either direction. Thin coverage also means the consensus may not fully capture recent leasing trends or portfolio-level developments that management will detail on the call.

Track record data would provide context on whether Cousins typically beats or misses estimates, but that history is unavailable for this preview. In the absence of beat/miss patterns, investors should focus on management’s tone regarding leasing pipelines, renewal rates, and capital allocation priorities. Office landlords face strategic crossroads: whether to invest in amenities and renovations to compete for flight-to-quality tenants, harvest cash flows from stabilized assets, or pivot capital toward other property types. Commentary on these fronts will matter as much as the quarterly numbers.

The quality of revenue growth deserves scrutiny beyond the headline figure. If the implied positive 6.3% revenue increase stems primarily from contractual rent steps on long-term leases signed years ago, that’s less encouraging than growth driven by new leasing at current market rates. Similarly, any revenue contribution from lease termination fees—one-time payments from tenants exiting space early—would flatter the top line but signal underlying tenant attrition. Occupancy trends, leasing spreads, and rent collection rates will paint a fuller picture of portfolio health.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.