AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street is bracing for a challenging comparison as InterDigital (IDCC) prepares to report first-quarter results on April 30th. The consensus among 4 analysts calls for earnings per share of $2.52 on revenue of $196.9M. The EPS estimate carries a tight range from $2.39 to $2.58, while revenue estimates span $196.1M to $197.8M, reflecting relatively modest disagreement about the company’s near-term trajectory.

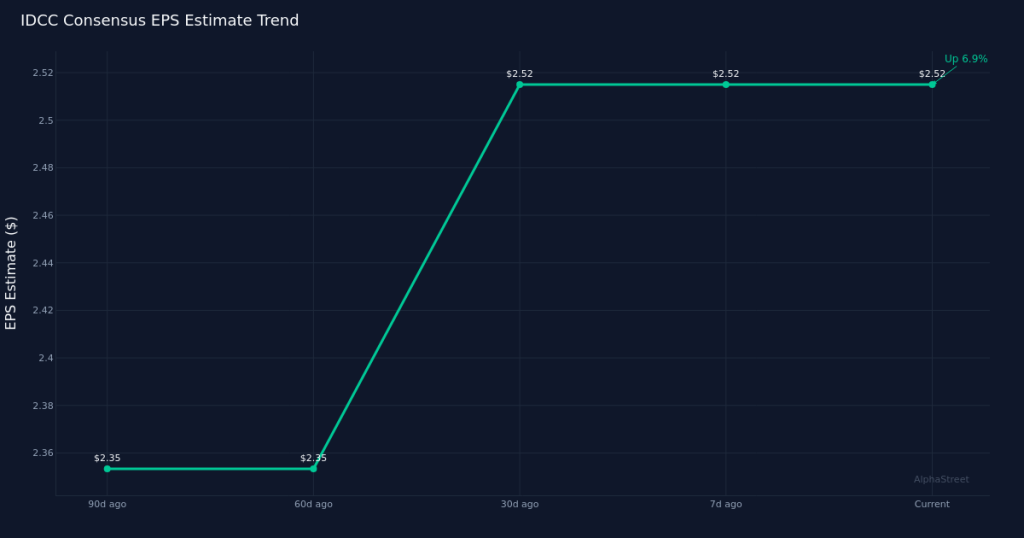

Analyst conviction has firmed over the past three months despite flat recent sentiment. EPS estimates have held steady over the past 30 days at $2.52, showing no drift from the prior month’s forecast. The 90-day view tells a more constructive story, with estimates climbing 7.2% from $2.35 three months ago. This upward revision pattern suggests analysts have grown incrementally more confident in InterDigital’s earnings power as visibility into the quarter improved, though the stabilization in recent weeks indicates that reassessment may have run its course.

The year-over-year comparison presents significant headwinds that will dominate the narrative. Consensus EPS of $2.52 represents a sharp decline from the year-ago quarter, while the revenue forecast of $196.9M marks a contraction of 6.5% from the prior year’s $210.5M. The magnitude of the earnings decline substantially exceeds the revenue pullback, pointing to margin pressure that extends beyond simple top-line deceleration. Last year’s first quarter delivered a net margin of 59.7% on net income of $125.7M, establishing a formidable benchmark. The divergence between revenue and earnings growth rates suggests InterDigital faces either mix shifts, elevated cost structures, or both as it cycles a particularly strong period from twelve months prior.

The profitability compression warrants close examination given the company’s business model dynamics. Software companies in the application space typically command attention for their ability to convert revenue into cash, and InterDigital’s year-ago net margin of 59.7% demonstrated exceptional efficiency. Whether the implied margin contraction reflects temporary investment cycles, changes in licensing revenue composition, or structural shifts in the cost base will be critical for investors assessing the sustainability of the company’s earnings power. The path from revenue to net income becomes the central question when top-line headwinds of 6.5% translate into bottom-line pressure.

Track record and execution consistency will factor heavily into how the market interprets results. Companies that consistently beat or miss estimates train investors to adjust expectations accordingly, and any deviation from historical patterns tends to trigger outsized stock reactions. InterDigital operates in a sector where licensing agreements, patent portfolios, and royalty streams can create lumpiness in quarterly results, making quarter-to-quarter comparisons particularly sensitive to timing effects that may not reflect underlying business momentum.

The estimate range itself signals measured analyst disagreement on key variables. With EPS estimates spanning $2.39 to $2.58, the high-end forecast sits roughly 8% above the low end, a spread that reflects differing assumptions about revenue recognition timing, operating leverage, or tax rates. The revenue range of $196.1M to $197.8M demonstrates tighter alignment on the top line, suggesting the earnings dispersion stems more from profitability assumptions than fundamental demand uncertainty.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.