Digital adoption and cloud migration accelerated during the pandemic as movement restrictions changed the way businesses function, which in turn necessitated effective solutions to prevent cyber t threats. CrowdStrike Holdings Inc (NASDAQ: CRWD), a leading provider of cybersecurity solutions, has been delivering stable earnings and revenue performance, though growth has slowed down recently.

Currently, CrowdStrike’s stock is trading well below the record highs of November 2021. It made modest but steady gains since the beginning of 2023, marking a recovery, but experienced weakness in recent weeks. The valuation is quite reasonable considering the potential for strong earnings growth going forward. Also, demand conditions remain encouraging despite economic uncertainties. So, CRWD seems to be one of the safest investment options currently. It has what it takes to create good shareholder value in the long term.

On Track

The Austin-headquartered company that is specialized in cloud security and threat hunting is investing in the business to expand capacity and optimize the platform, thanks to the healthy cash flow. It is focused on coming up with advanced solutions capable of dealing with today’s sophisticated threats.

Spending on cybersecurity has been stable for quite some time, even while most areas of the technology sector witnessed a slowdown in spending due to economic uncertainties and muted customer sentiment. CrowdStrike started incorporating artificial intelligence and machine learning into its products long ago, which has made it better positioned to deliver effective cloud-based protection services.

Competition

Meanwhile, the cybersecurity market is becoming increasingly competitive, which is the main reason behind CrowdStrike’s slowing growth and dip in share price, lately. But the company has outperformed its main rivals in the recent past, leveraging the software-as-a-service business model that helps generate decent recurring revenues and margins.

“For years, our use of AI has enabled us to rapidly scale that business to a leadership position with an exceptional product margin that exceeds our overall company gross margin. The margin profile and scale we have achieved for our managed offering would not have been possible without our innovations in AI. While others are just now jumping on the AI bandwagon, we have transformed cybersecurity with an AI-powered cloud business from inception,” said CrowdStrike’s CEO George Kurtz during his post-earnings interaction with analysts a few months ago.

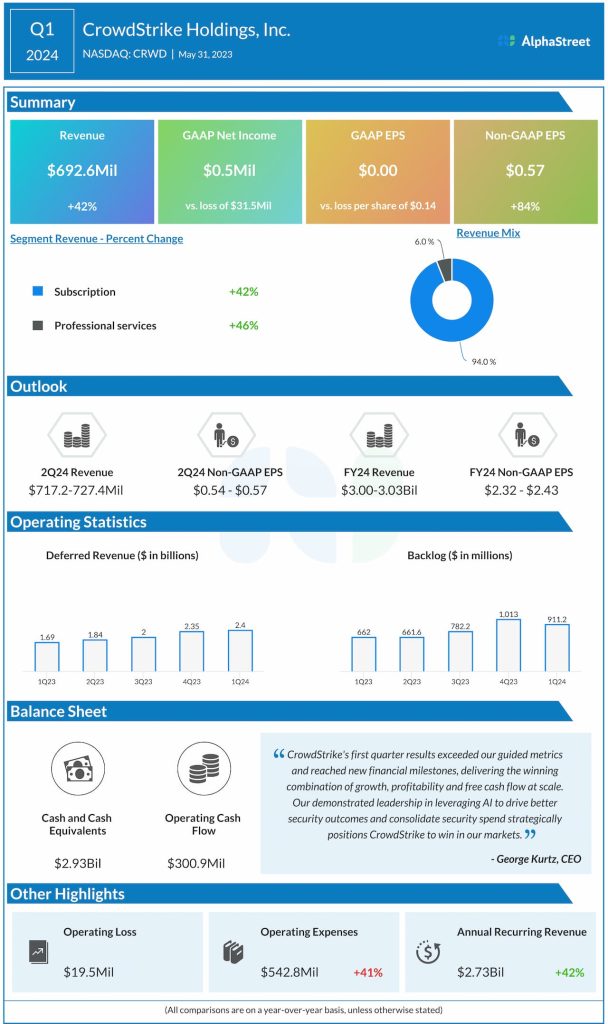

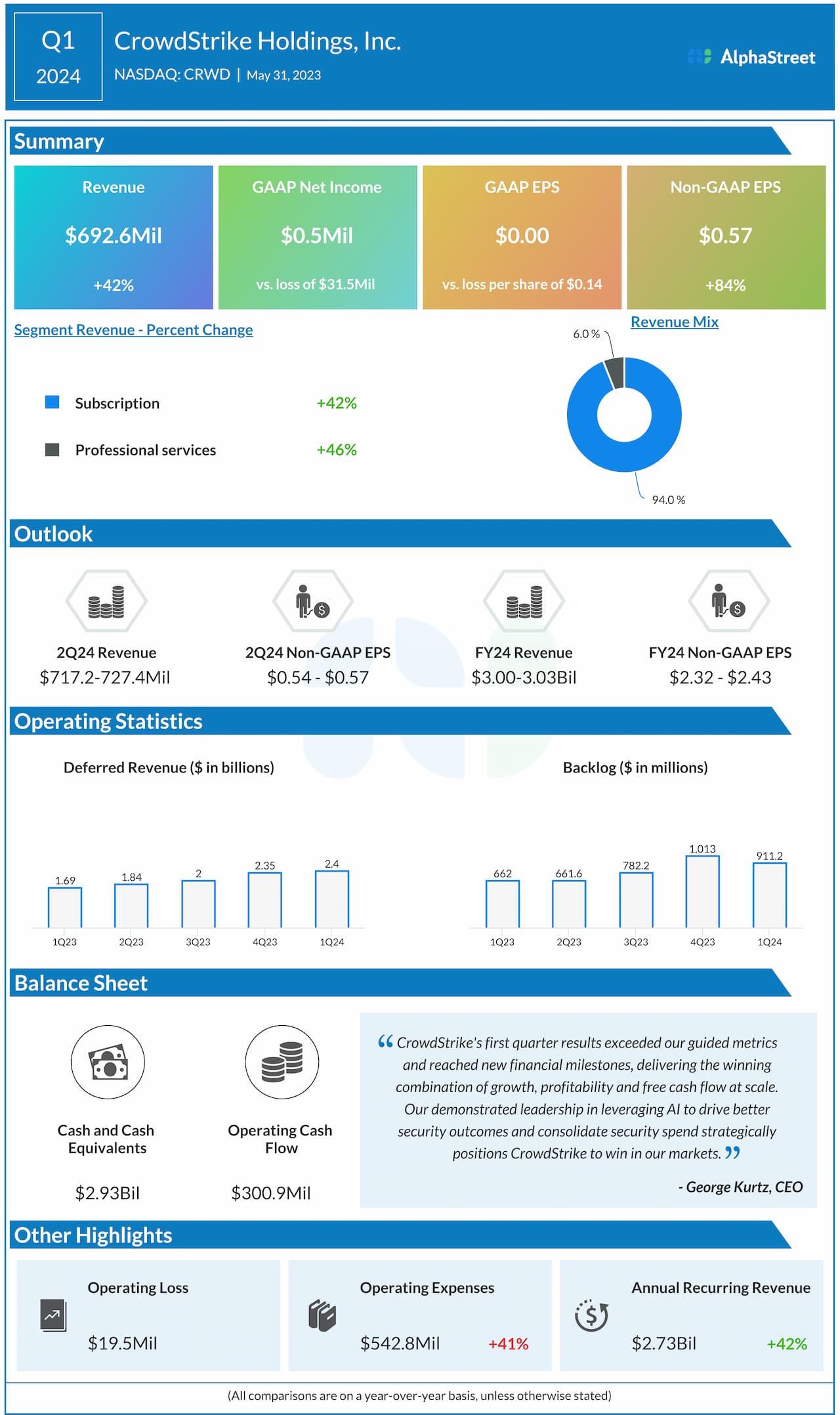

In the first three months of fiscal 2024, the company’s core subscription business grew an impressive 42%. That, combined with an almost similar increase in Professional Services revenues, resulted in a 42% growth in total revenues to $692.6 million. At $0.57 per share, adjusted profit was up 84%.

Guidance

The management issued strong guidance even as the first-quarter backlog and deferred revenue increased from last year. It expects second-quarter revenues to be between $717.2 million and $727.4 million, and adjusted earnings per share in the range of $0.54 to $0.57. Full-year earnings per share is forecast to be in the $2.32-$2.43 range. The consensus revenue estimate for fiscal 2024 is $3.0-3.03 billion.

Shares of CrowdStrike opened Tuesday’s session higher, after starting the week on a low note. In the past six months, however, they have gained about 26%.