The food industry is among the worst affected by the COVID-related disruption, as movement restrictions forced people to stay indoors, hitting footfall at restaurants. Things have improved since the pandemic sent the business world into a tailspin, but the food and beverage industry is now struggling to cope with high inflation. Darden Restaurants, Inc. (NYSE: DRI), the company that owns popular food brands like Olive Garden and LongHorn Steakhouse, has been increasing prices to tackle rising raw material costs.

The Stock

Unlike most Wall Street stocks, the Orlando-based company’s shares stayed on an upward spiral for most of 2022. In November, it came pretty close to last year’s peak but started losing steam since then. DRI suffered a big loss this week after the latest earnings report triggered a selloff. The drop came as a surprise to many because on the face of it everything looked good in the second-quarter report.

Read management/analysts’ comments on quarterly reports

While sales and earnings per share increased, net profit declined. That, together with the continuing squeeze on margins due to higher operating costs seems to have disappointed investors. Muted consumer sentiment and rising operating expenses are the main challenges facing the business, a trend that is likely to continue in the near future.

In Good Taste

But the short-term headwinds should not be a worry for long-term investors, for Darden is one of the most successful restaurant brands in America. Stable revenue performance and improving same-store sales growth point to Darden’s ability to withstand adversities. Citing its strong prospects of creating solid shareholder value, the majority of analysts recommend buying the stock. The company has an impressive track record of returning value to shareholders – offers a dividend yield of around 3.5%, after regular hikes.

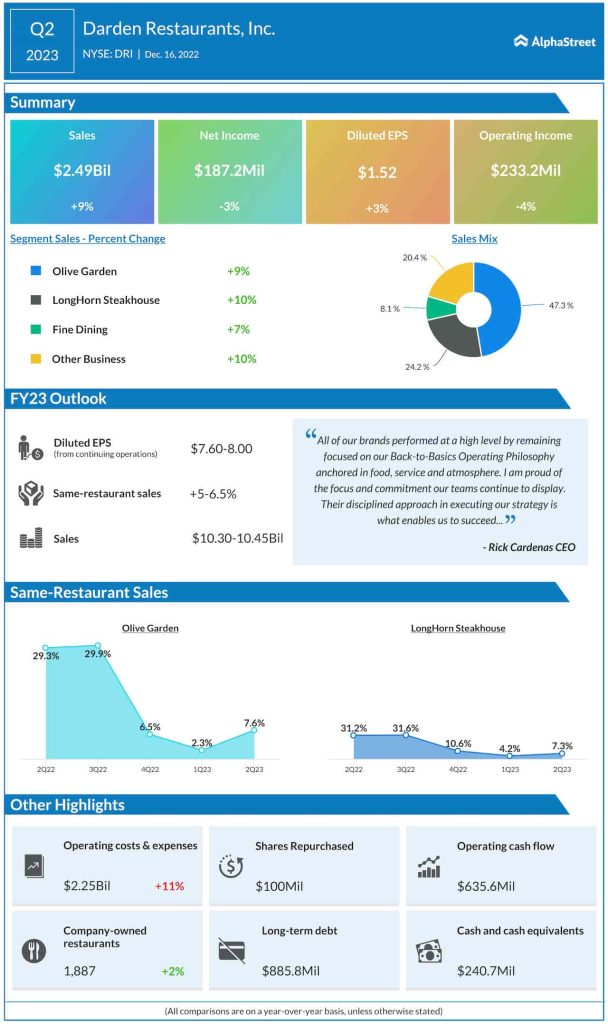

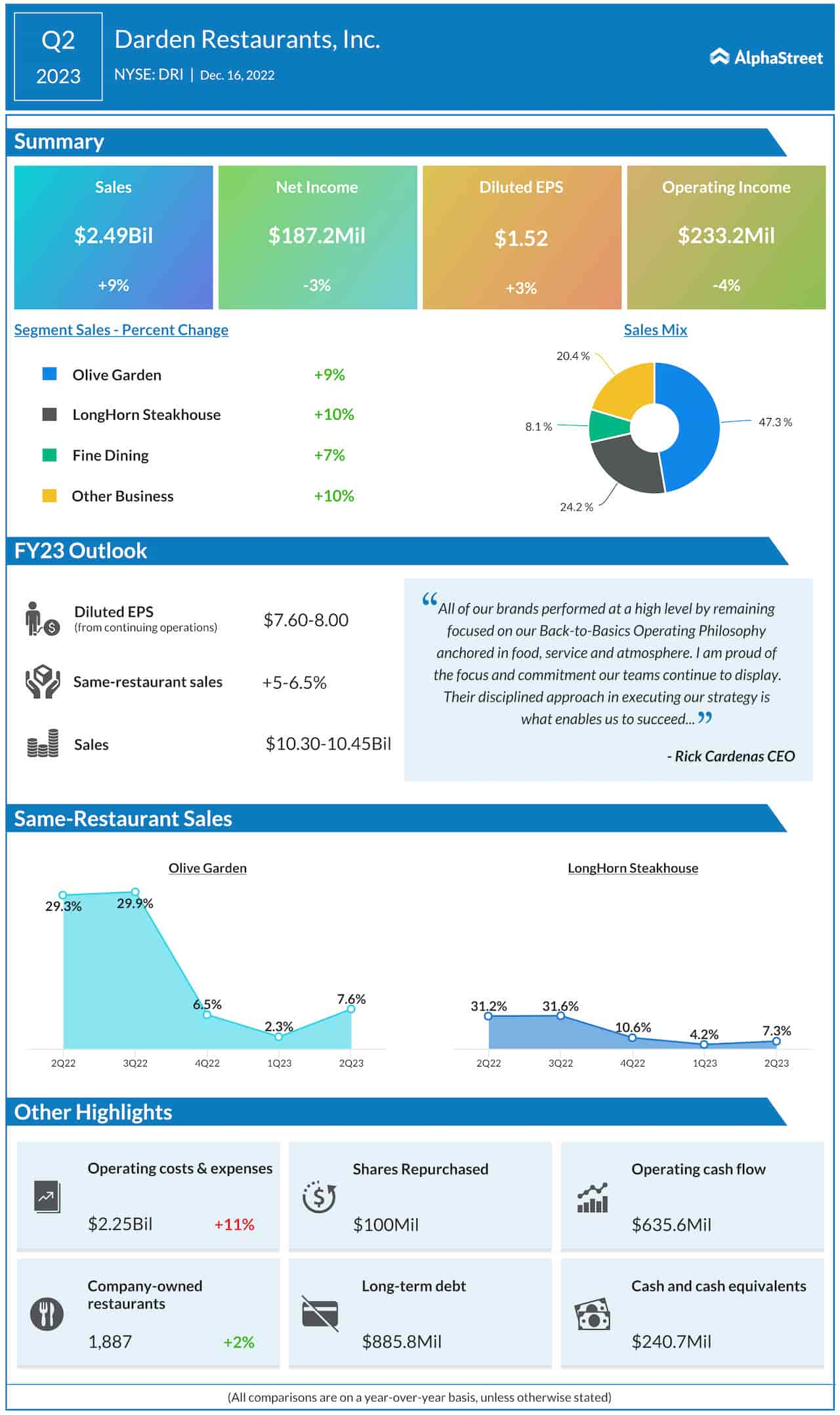

Commenting on the results, Darden’s CEO Rick Cardenas said, “all of our brands performed at a high level by remaining focused on our Back-to-Basics Operating Philosophy anchored in food, service, and atmosphere. I am proud of the focus and commitment our teams continue to display. Their disciplined approach in executing our strategy is what enables us to succeed, evidenced by the fact that, just last week, we surpassed $10 billion in sales on a trailing 52-week basis for the first time in Darden’s history.”

Key Numbers

Overall, Darden has maintained better profitability than estimated in recent years, but it was a hit-and-miss journey for the top line. In the second quarter of 2023, all the business units registered growth, which translated into a 9% rise in total sales to $2.49 billion. While net profit dropped, adjusted earnings moved up to $1.52 per share, defying expectations for a decline. The increase reflects a dip in the number of shares outstanding. Same restaurant sales, which excludes the effects of restaurant openings and closings, rose 7.3%, with strong contributions from Olive Garden and LongHorn Steakhouse.

McDonald’s Corporation Q3 2022 Earnings: Key financials and quarterly highlights

DRI dropped soon after the earnings announcement and traded down a dismal 3% on Friday afternoon. The stock has gained about 24% in the past six months.