Like many growth stocks in the technology sector, Smartsheet (NYSE: SMAR) was also expected to benefit from the worldwide lockdowns due to the coronavirus pandemic. Companies in this sphere have mostly benefited from the increased adoption of work-from-home norms and the absolute necessity to move operations from offline to online.

And riding on this optimism wave, the stock had gained 84% since mid-March. But following the Q1 results on Wednesday, the stock tumbled over 20% despite the cloud platform surpassing analysts’ expectations on the top and bottom line.

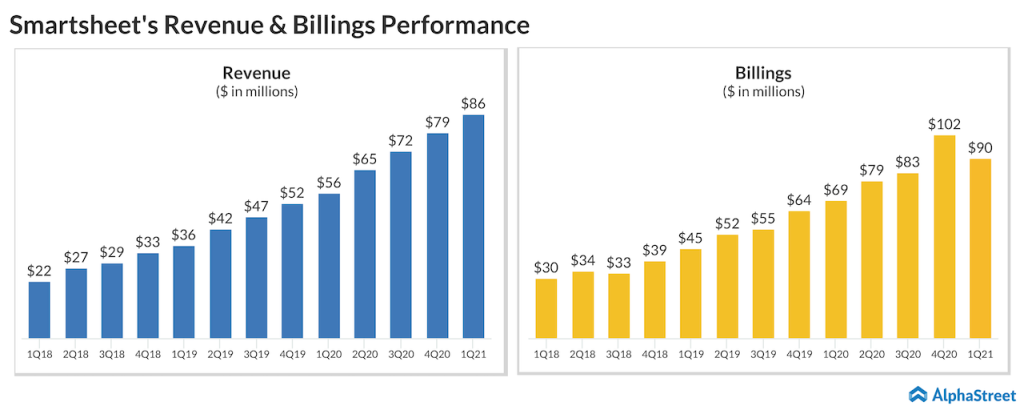

Investors were mainly upset over the company missing its own target on calculated billings as well as the weaker-than-expected outlook. Billings for the quarter came in at around $90 million, even though Smartsheet had projected it in the range of $97-98 million. Meanwhile, the annual revenue outlook of $360-370 million marks a significant decrease from its previously recorded growth rates. But does it warrant a 20% sell-off?

[irp posts=”62564″]

To start off, Smartsheet already enjoys a great valuation for a company with negative operating income and free cash flow. Hence, it would be difficult to allege value erosion. But the operating side is strong and the pandemic should ultimately help the company’s mission in the long run. Hence, there is no outright reason to be pessimistic about this stock.

According to the company, missing target on billings was primarily attributable to adjustments made for SMB clients that were affected by the pandemic. During the earnings conference call, CFO Jennifer Ceran said:

“We care deeply about the well-being of our customers, and as such supported those most impacted with extended terms or adjustments to quarterly and semi-annual billings. This support had a negative impact to our billings growth rate in the quarter.”

Notably, around 28% of its ARR came from SMEs

at the end of the first quarter.

Meanwhile, Smartsheet continues to be strong on the enterprise side despite COVID-based disruptions. Fifteen customers expanded their ARR by over 100,000, two customers more than what they had achieved a year ago. The company, on the other hand, agrees that customer spend might be low in the upcoming quarters due to the pandemic impact.

Net retention rate could fall below 130%

in the second quarter, but even this number is pretty good from an industry

perspective. Speaking on net retention rate trends, Ceran stated:

“So, you think about healthcare, telecommunications, finance, education, we actually saw acceleration in the dollar net retention rate. Where we saw a deceleration more pronounced were in the sectors that truly are being heavily impacted by COVID. So, the retail industry as well as travel and hospitality, both declined and that influenced the overall outcome of our business results.”

Wall Street analysts continue to be bullish on the stock despite the selloff. Post the earnings release, five analysts increased the price target on the stock, while two lowered theirs. Thanks to the positive sentiment from analysts’ end, the stock could witness a rebound in the coming days.

[irp posts=”62384″]

__

For more insights about Smartsheet, read the latest earnings transcript here