Domino’s Pizza, Inc. (NASDAQ: DPZ) has been navigating a challenging macroeconomic backdrop, which has weighed on its recent results. Investors remain concerned about the recent slowdown in comparable sales, particularly in the US. However, the company in a recent statement said it does not see any material impact from broader global macro or geopolitical uncertainties in the near term.

The fast-food chain, which operates more than 20,000 stores across 90 markets, is poised to publish its fourth-quarter results on Monday, February 23, at 6:05 am ET. On average, analysts following the business forecast revenues of $1.52 billion for the final three months of 2025, representing a 9.95% year-over-year growth. The consensus earnings per share estimate for Q4 is $5.38, versus $4.89 in the prior-year quarter.

For Domino’s stock, 2025 was a challenging year, marked by high volatility and range-bound movement. In recent months, the shares have constantly traded below their long-term average value of $443.25. The stock has declined more than 20% in the past twelve months. Analysts’ positive outlook indicates that DPZ is on track for a potential recovery this year.

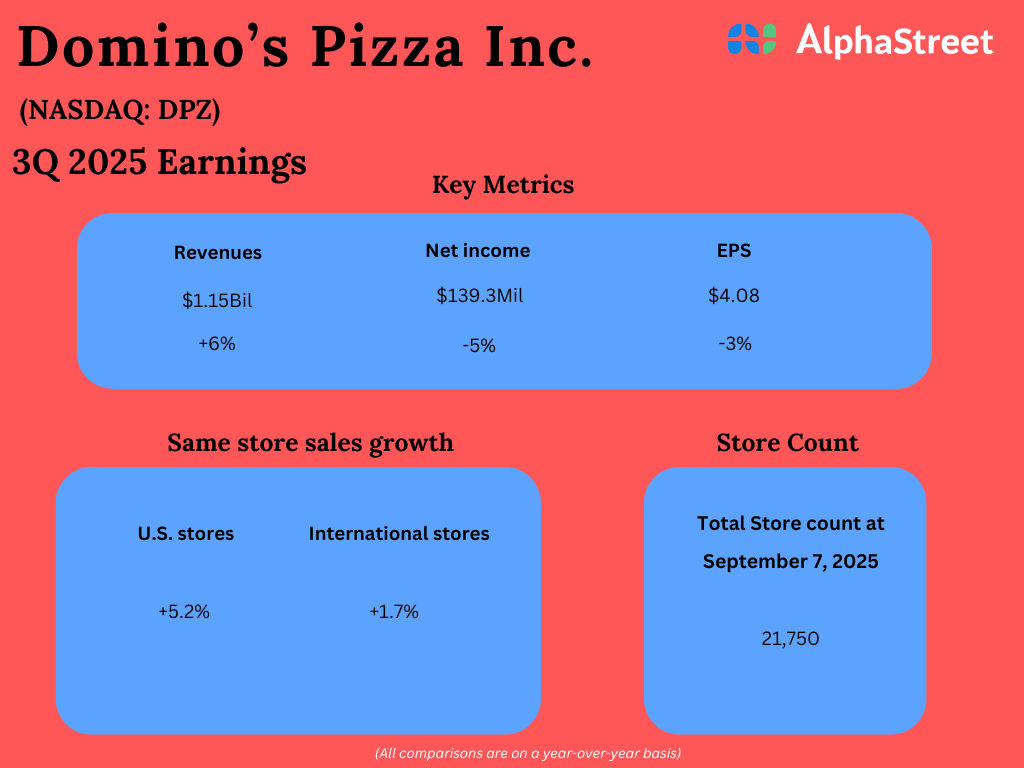

In the third quarter of FY25, the company’s revenues grew 6.2% from the prior year to $1.14 billion, beating estimates. US same-store sales and international same-store sales grew 5.2% and 1.7%, respectively. Global retail sales were up 6.3%. Meanwhile, net income declined to $139.3 million or $4.08 per share in Q3 from $146.9 million or $4.19 per share in the corresponding quarter of FY24. The bottom line exceeded Wall Street’s expectations.

READ MORE: Highlights of Domino’s Pizza’s Q3 2025 Earnings

From Domino’s Q3 2025 Earnings Call:

“We have best-in-class franchisee economics in QSR pizza, the largest advertising budget, a supply chain with incredible purchasing power, a rewards program that is bigger than ever. And we’re just getting started. As you know, we don’t usually do LTOs at Domino’s. So, everything we have launched over the last two years, aggregator ordering, new loyalty platform, stuffed crust, and more is a part of our base and will be part of our growth in the future. And we will continue to add new products, technology, and renowned value promotions on top of that.”

In a recent statement, Domino’s said it continues to expect its international same-store sales to grow a modest 1-2%, reflecting the volatile macro environment in the US. Management expects market share to continue benefiting from its ‘Hungry for More’ plan, designed to accelerate growth through the concepts of ‘Most Delicious Food, Operational Excellence, Renowned Value, and Enhanced Franchisees’

Domino’s stock has lost around 10% so far in 2026, extending the weakness experienced last year. On Monday, DPZ opened at $380.27 and was down more than 1% in the early hours.