Darden Restaurants, Inc. (NYSE: DRI) delivered positive performance during the holiday season, which is probably the busiest time for the restaurant chain, and is preparing to report third-quarter results next week. Sales have come under pressure from cautious consumer spending lately, but the management is optimistic in their outlook for the fiscal year.

After a weak start to 2024, the Orlando-headquartered firm’s stock gained strength in recent weeks and climbed to an all-time high early this month. The uptrend is likely to continue as DRI has more room for growth. In general, analysts are bullish on the growth prospects of the stock which has long been a favorite among investors, thanks to the impressive returns and regular dividend hikes. It currently offers a yield of 3.8%, which is more than double the S&P 500 average.

What to Look for

It is estimated that revenues increased to $3.03 billion in the February quarter from $2.79 billion in the prior year period. On average, market watchers believe that third-quarter profit rose to $2.64 per share from $2.34 per share in the prior year period. The report is expected to be released on Thursday, March 21, at 7:00 a.m. ET. Interestingly, the company’s quarterly earnings have mostly beaten estimates in the past ten years.

“We have reached the halfway point in our fiscal year, and I’m pleased with our performance thus far. All of our brands remain focused on managing the business for the long term and the power of Darden positions us well for the future. We also continue to work in pursuit of our shared purpose, to nourish and delight everyone we serve. One of the ways we do this for our team members and their families is through our Next Course Scholarship program,” Darden’s CEO Rick Cardenas said in a recent statement.

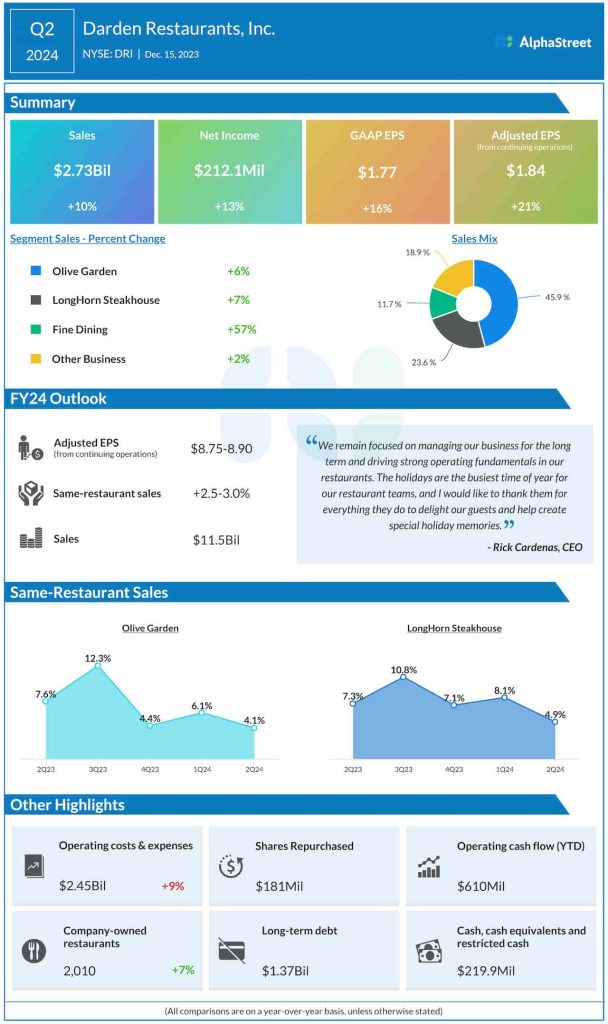

Having successfully transitioned some of its restaurants into distribution centers in the last quarter, the company is working to expand the distribution network further. The management has raised its full-year earnings per share guidance to $8.75-$8.90 from the earlier forecast of $8.55-$8.85 per share, excluding transaction and integration costs related to Ruth’s Chris Steak House which joined the Darden fold last year.

Solid 1H

In the November quarter, total sales increased 10% year-over-year to $2.73 billion and came in broadly in line with analysts’ estimates. The top-line growth was driven by a 6% sales growth in the core Olive Garden division, besides strong performance by all other operating segments. Consequently, there was a 21% jump in adjusted earnings to $1.84 per share. Same-store sales increased for both the Olive Garden and LongHorn Steakhouse businesses, but at a slower pace than in the previous quarter and prior-year period.

Darden Restaurants’ stock has gained about 30% in the past five months. It made modest gains in early trading on Monday, after opening the session just above $170.