Discount store operator Dollar General Corporation (NYSE: DG) is preparing to report second-quarter results on Thursday morning, a week after Dollar Tree, another leading low-price retailer, reported mixed results for its most recent quarter. While sales of consumables remain largely stable, the other categories experience weakness as customers continue to cut back on discretionary spending.

Dollar General’s stock has declined steadily since hitting a record high ten months ago, losing around 40% since then. DG suffered a selloff a few months ago after the company reported unimpressive results for the first three months of the fiscal year and issued cautious guidance. Going forward, investor sentiment will likely remain weak as economic uncertainties and the growing competition in the retail sector weigh on sales.

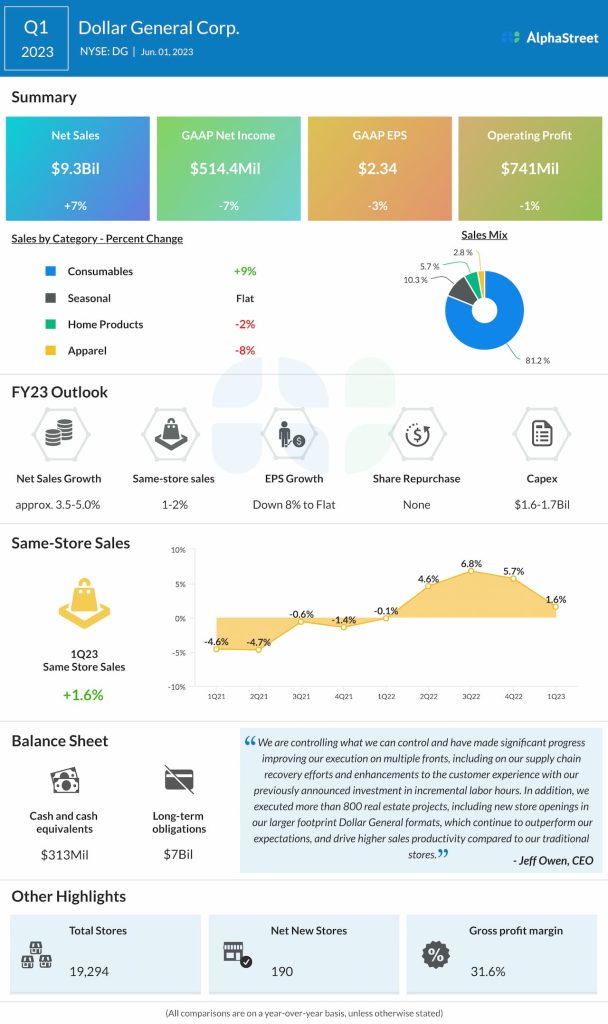

Q2 Report Due

Dollar General will be publishing its second-quarter 2023 results on Thursday before the market opens. It is widely expected that the company would report earnings of $2.46 per share for the July quarter, down 17% from the prior-year period when it posted net income per share of $2.98 per share. The consensus revenue estimate is $9.93 billion, which is up 5.30% from the second quarter of 2022.

The top line could benefit from the low prices, positive inventory position, and private-label offerings. With more than 19,000 stores spread across the country, the company is well-positioned to continue attracting low-to-middle-income-group consumers to its stores. Also, having the right balance between the consumables and non-consumables categories should drive store traffic. These factors are expected to offset the impact of the challenging market conditions to some extent.

Our same-store sales results were driven by increased basket size, partially offset by a decrease in customer traffic. While we gained market share in non-consumables again this quarter, our share in consumables was essentially flat as we believe the macro headwinds have had a disproportionate impact on our core customers. From a monthly cadence perspective, same-store sales growth was strongest in February at 4.8% and ahead of our expectations,” said Dollar General’s CEO Jeff Owen at the Q1 earnings call.

Earnings Fall

Earnings dropped to $2.34 per share in the first quarter and came in below Wall Street’s projection. It marked the third consecutive earnings miss, after beating the estimates almost regularly for about three years. Meanwhile, revenues moved up 7% annually to $9.3 billion but fell short of expectations. Comparable sales growth decelerated for the second time in a row. The company opened 190 new stores during the quarter.

Anticipating the mixed trend to continue in the remainder of the year, the management expects fiscal 2023 revenues to grow modestly in the 3.5-5% range, reflecting a 1-2% comparable sales growth. Full-year earnings growth is expected to be flat to down 8%.

Dollar General shares traded slightly higher in the early hours of Monday’s session. It has lost 28% in the past six months and mostly stayed below its 52-week average during that period.