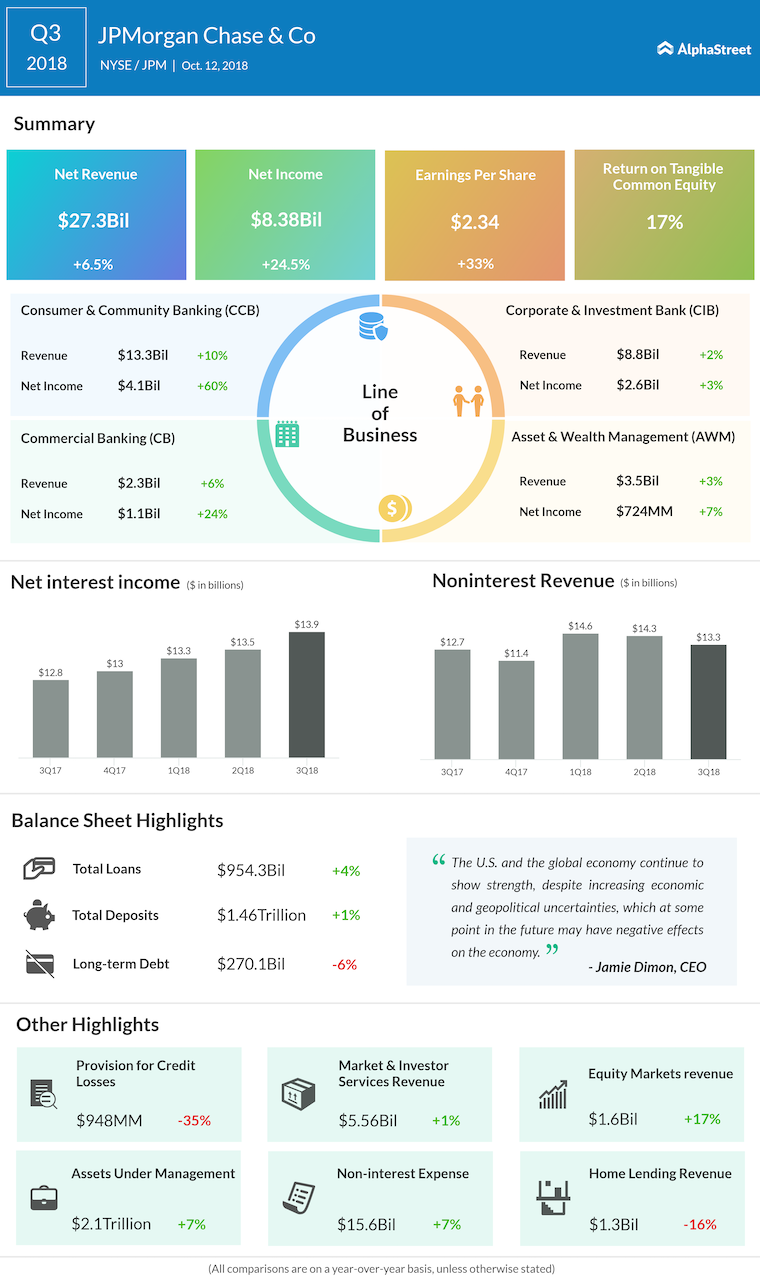

JPMorgan Chase (JPM) is scheduled to report fourth-quarter results on Tuesday, January 15, amidst high global economic tension and increasing market volatility. The global headwinds – including a slowing economic scenario leading to a potential recession, the Brexit crisis as well as the unending trade war scenario – have already taken its toll on the banking stocks.

Most banking stocks have declined since a year ago, with JPMorgan trading down 11%.

For the fourth quarter, analysts expect the banking giant to report earnings of $2.20 per share, compared to $1.76 per share it posted last year. Meanwhile, revenue is expected to increase by 6.7% year-over-year, primarily driven by trading revenues.

CEO Jamie Dimon had last month stated that the company expects trading revenues to be flat in the fourth quarter at an investors’ meet. Yet, the trading floors have mostly remained busy in the holiday quarter driven by the aforementioned macro-economic factors, the condition of the housing industry and a lack of clarity relating to interest rate hikes. This should work in favor of JPM, given trading revenues account for almost a quarter of its top line.

Strength in credit card business is another factor that is clearly going to boost results in Q4.

On the other hand, investors are likely to see some weakness in all the other segments. For example, seasonal headwinds are expected to play spoilsport in the financials relating to investment banking. Underwriting activities were generally slow towards the end of last year as companies planning to issue shares waited for a clearer market environment.

Meanwhile, debt origination fees, which contribute about 50% of JPMorgan’s investment banking revenues, were dented by an increase in the interest rates by the Federal Reserve.

Citigroup Q4 revenue drops on weak bond trading; earnings beat

JPM stock has a 12-month average price target of $121.21, suggesting a 21% upside from Friday’s close. Six out of 10 analysts have a Hold rating on the stock while the others recommend Buy.

On Monday, rival Citigroup (C) reported stronger-than-expected earnings for the fourth quarter when revenues dropped and missed estimates. The stock declined 1% in the premarket after the earnings report.