JetBlue Airways Corporation (NASDAQ: JBLU) is scheduled to report second quarter 2019 earnings results on Tuesday, July 23, before market open. The Street estimates earnings will grow 50% year-over-year to $0.57 per share while revenue is projected to increase 8% to $2.10 billion. The company has consistently topped earnings estimates in the last four quarters.

The airline has reported growth in traffic and capacity for all three months of the quarter. Revenue per available seat mile (RASM) is expected to grow around 3.1% in the second quarter from the prior-year period. This will come within the company’s guidance of 2-4%. Also, passenger revenues have not been affected much by the hike in baggage fees last year.

The company is also expected to benefit from lower oil

prices which is likely to help margins. JetBlue has been relatively unaffected

by the Boeing crisis as the company does not have any Boeing 737 Max jets in

its fleet. However fluctuations in its load factor remain a concern.

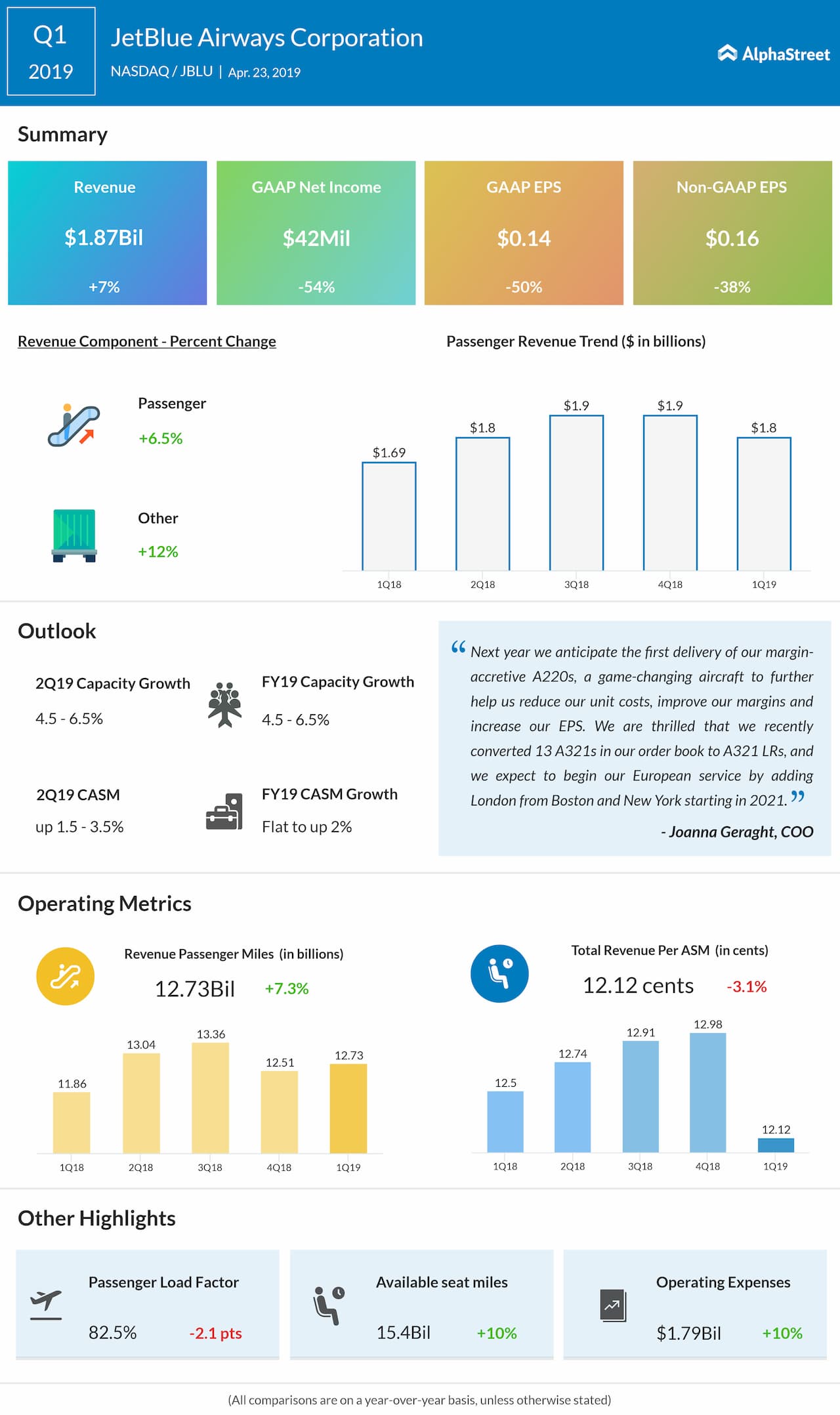

In the first quarter of 2019, JetBlue beat earnings estimates despite adjusted EPS falling 38% to $0.16. Revenue increased 7% to $1.87 billion. RASM declined 3.1% year-over-year while cost per available seat mile (CASM), ex-fuel, rose 0.9%.

For the second

quarter of 2019, capacity is expected to increase between 4.5% and 6.5%

year-over-year. For full-year 2019, capacity is expected to grow in the

range of 1% to 4%. JetBlue is expected to see a 6.5% growth in revenues for

fiscal-year 2019, which is higher than most of its peers in the airline

industry.

JetBlue’s shares have gained 19% so far this year and 12% in the past three months. According to TipRanks, out of seven analysts covering the stock, three have rated it Buy while four have rated it Hold. None have rated it Sell. The average one-year price target on the stock is $22.21.