AlphaStreet Newsdesk powered by AlphaStreet Intelligence

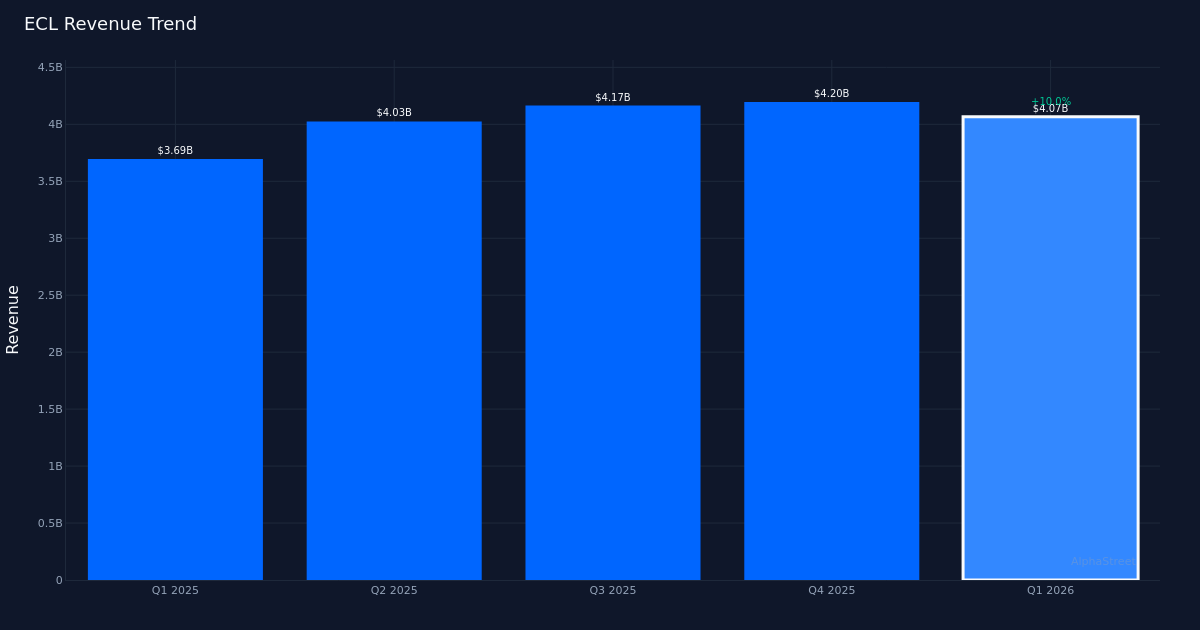

Narrow miss. Ecolab Inc. (NYSE: ECL) reported Q1 2026 adjusted diluted EPS of $1.70 per share, falling short of the $1.71 consensus estimate by 0.6%. Revenue totaled $4.07B for the quarter, representing a 10.0% increase from the $3.69B recorded in Q1 2025. Bottom-line profit came in at $482.5M. The specialty chemicals company’s shares traded down 1.5% at $263.77 following the release, though the modest shortfall appears largely tied to timing rather than fundamental deterioration.

Revenue strength. The top-line performance proved the quarter’s bright spot, with the double-digit revenue expansion driven by a combination of pricing discipline and volume recovery across key end markets. Organic sales growth of 4.0% for the quarter demonstrates genuine underlying momentum beyond the benefits of acquisition activity or foreign exchange tailwinds. This quality of growth suggests Ecolab’s value proposition continues to resonate with customers navigating heightened hygiene and water stewardship requirements across industrial and institutional settings.

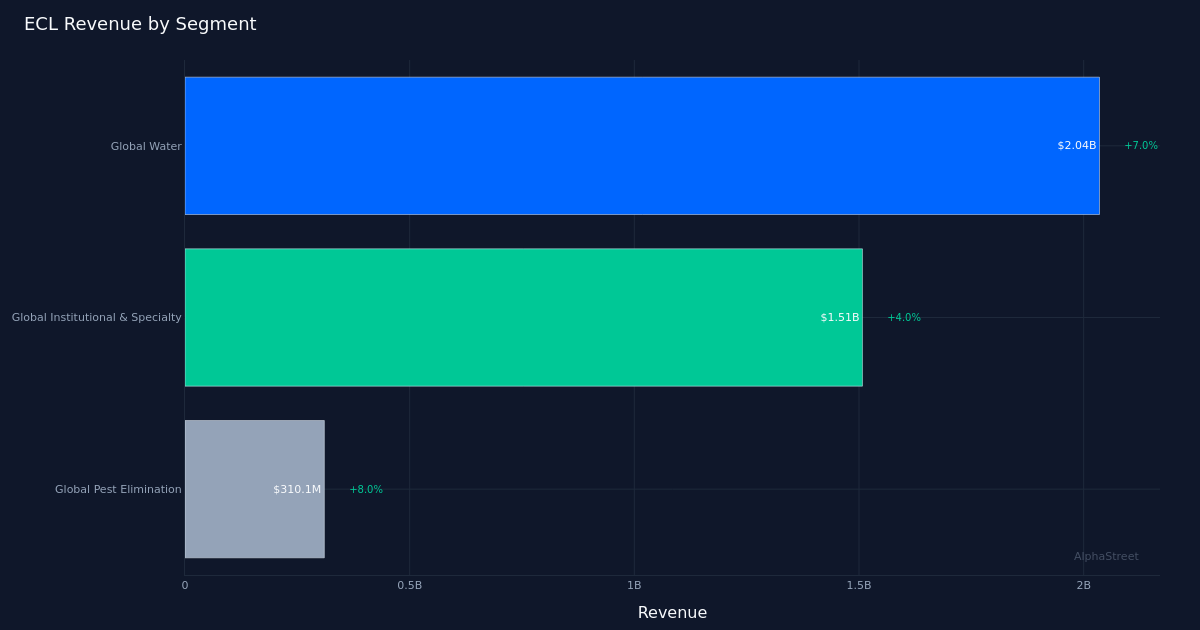

Global Water dominates. The company’s largest segment, Global Water, led with $2.04B in revenue, up 7.0% year-over-year. This unit remains the engine of Ecolab’s growth story, capturing accelerating demand for water treatment and process optimization solutions as industrial customers face both regulatory pressures and resource scarcity concerns. The segment’s performance underscores management’s strategic positioning at the intersection of sustainability and operational efficiency, where customer return on investment calculations increasingly favor Ecolab’s premium-priced solutions.

Guidance provided. For FY 2026, management guided adjusted EPS to a range of $8.43 to $8.63. The midpoint of this guidance implies meaningful acceleration from the Q1 run rate, suggesting management anticipates margin expansion and operational leverage to build throughout the year. This cadence aligns with historical seasonality patterns in the specialty chemicals sector, where first-quarter results typically represent the lightest period before stronger performance in the second half as industrial activity intensifies and price increases fully annualize.

Wall Street positioned. Analyst sentiment remains constructive, with consensus standing at 13 buy ratings, 11 hold ratings, and zero sell recommendations. This distribution reflects broad recognition of Ecolab’s durable competitive advantages in mission-critical applications, though the balanced buy-to-hold ratio suggests some caution around valuation following the stock’s recent run. The marginal earnings miss may prompt modest estimate revisions, but the revenue trajectory and intact guidance should limit any meaningful downgrades to investment theses.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.