AlphaStreet Newsdesk powered by AlphaStreet Intelligence

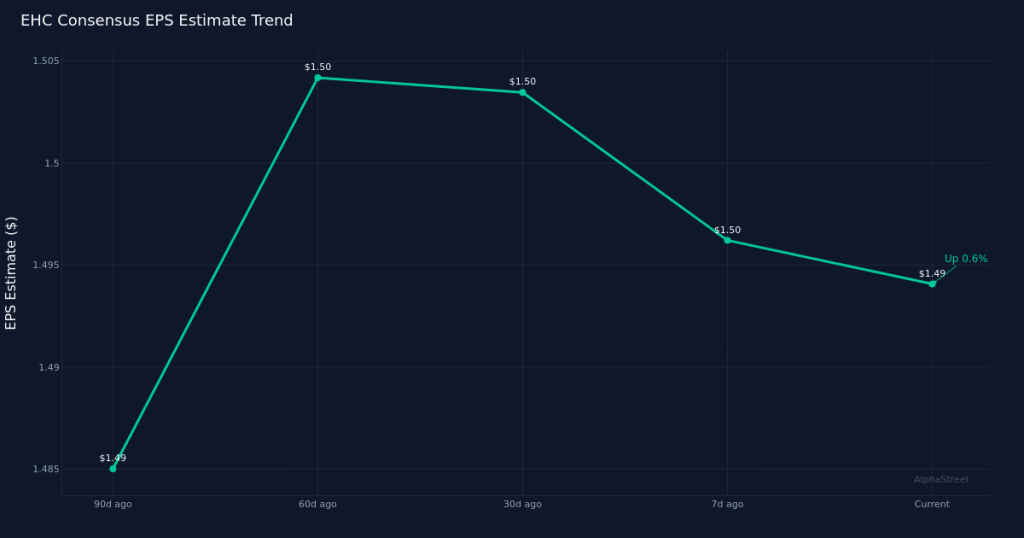

Wall Street is looking for Encompass Health Corporation to deliver $1.49 per share in earnings on revenue of $1.57 billion when the rehabilitation hospital operator reports first-quarter 2026 results on May 1st. Twelve analysts cover the stock, with EPS estimates ranging from $1.38 to $1.53 and revenue projections spanning $1.56 billion to $1.58 billion. The consensus figures suggest continued growth momentum for the nation’s largest operator of inpatient rehabilitation facilities as the company scales its network and captures demand from an aging patient population.

Analyst sentiment has shifted slightly bearish in recent weeks. The consensus EPS estimate has drifted down 0.7% over the past 30 days, declining from $1.50 to the current $1.49 expectation. This modest downward revision may reflect tempered near-term expectations around patient volumes, reimbursement pressures, or labor cost management. On a 90-day view, however, estimates have remained flat at $1.49, suggesting the recent pullback represents a tactical recalibration rather than a fundamental reassessment of the company’s trajectory.

The consensus implies healthy year-over-year expansion across both the top and bottom lines. Revenue is expected to climb 7.5% from the $1.46 billion Encompass Health generated in the first quarter of 2025, while earnings per share should advance 8.8% from the year-ago figure of $1.37. The year-ago quarter produced net income of $139.5 million and a net margin of 9.6%, establishing a profitability baseline against which investors will measure this quarter’s performance. The faster growth rate at the earnings line compared to revenue suggests Wall Street anticipates continued margin expansion or operational leverage as the company spreads fixed costs across a larger revenue base.

Encompass Health operates in the medical care facilities sector, where key performance indicators center on patient volumes, discharge metrics, and same-store revenue growth at existing hospitals. Investors typically scrutinize occupancy rates at the company’s inpatient rehabilitation facilities, length of stay trends, and revenue per discharge as leading indicators of both demand strength and pricing power. The company’s ability to expand its hospital footprint through acquisitions and de novo development while maintaining service quality and reimbursement rates from Medicare, Medicare Advantage, and commercial payers will be critical factors in sustaining the growth trajectory implied by consensus estimates.

The stock is trading at $103.84 as the report date approaches. Positioning ahead of earnings reflects investor confidence in the company’s post-acute care franchise, though the recent estimate drift suggests some caution is warranted. How the stock reacts to the print will depend not only on whether Encompass Health meets the $1.49 EPS bar but also on management’s commentary regarding patient admission trends, labor cost inflation, and the pipeline for new hospital openings throughout 2026.

Encompass Health’s track record on earnings surprises will influence how much room for error the market is pricing in. Companies with consistent beat histories often see their stocks rally even on modest upside, while those with volatile execution face steeper punishment for misses. Investors will be watching whether the company can sustain the profitability momentum evident in the year-ago net margin of 9.6%, particularly as wage pressures in healthcare persist and reimbursement negotiations with payers remain dynamic.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.