AlphaStreet Newsdesk powered by AlphaStreet Intelligence

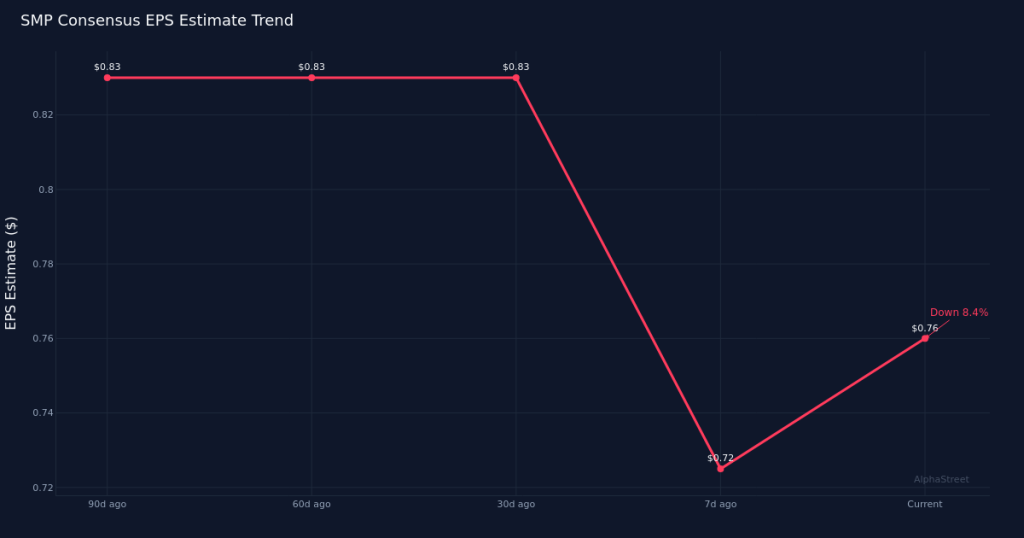

Wall Street is expecting modest top-line growth when Standard Motor Products, Inc. (NYSE:SMP) reports first-quarter 2026 results on April 30. The consensus among 3 analysts calls for earnings per share of $0.76 on revenue of $429.1M. The revenue estimate implies year-over-year growth from the $413.4M reported in the prior-year quarter. Analyst estimates for EPS range from $0.72 to $0.83, while revenue projections span $422.4M to $434.0M, reflecting relatively tight conviction around the core outlook for the automotive aftermarket parts supplier.

Analysts have grown more cautious heading into the print. The consensus EPS estimate has drifted down 8.4% over the past 30 days, falling from $0.83 to the current $0.76. The same downward revision is evident over the 90-day window, signaling sustained pressure on earnings expectations rather than a momentary reset. This negative estimate trajectory suggests analysts are either building in margin headwinds, incorporating weaker demand signals, or reflecting management commentary that may have tempered near-term profitability assumptions. The revision pattern warrants attention as it indicates deteriorating confidence in the company’s ability to deliver on earlier projections.

The year-over-year comparison shows revenue advancing but profitability under scrutiny. Consensus revenue of $429.1M represents growth of 3.8% from the $413.4M generated in the first quarter of 2025. That growth rate, while positive, is modest for a company operating in the replacement parts market, which typically benefits from an aging vehicle fleet and steady repair demand. The year-ago quarter produced net income of $18.0M and a net margin of 4.4%. With the consensus EPS estimate of $0.76 now sitting below the revised figures from just weeks ago, investors will be watching whether margin compression is materializing or if the company can maintain profitability levels despite any cost or competitive pressures in the supply chain.

Standard Motor Products operates in a fragmented aftermarket environment where brand strength and distribution matter. The company’s portfolio spans engine management and temperature control products sold through traditional wholesale distributors, retail chains, and increasingly through e-commerce channels. As vehicle complexity increases with emissions regulations and electrification trends, the company’s ability to innovate and maintain pricing power becomes critical. The first quarter typically reflects seasonal patterns in the automotive aftermarket, with winter-related repairs driving temperature control demand while engine management products see steadier year-round activity. How these segments performed relative to each other and whether any channel mix shifts occurred will provide clues about underlying business health.

Investor focus will center on whether the company can reverse the estimate revision trend. The downward drift in EPS expectations suggests either input cost inflation, pricing pressure, or volume shortfalls are weighing on near-term profitability. Standard Motor Products has historically managed through cyclical pressures by leveraging its established distribution relationships and broad product lineup, but the current estimate trajectory indicates the Street is penciling in a softer outcome than initially anticipated. Any commentary on inventory levels at key customers, pricing actions, or raw material costs will be scrutinized for signals about the balance of the year.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.