Pinterest’s stock (NYSE: PINS) has gained 136% since the beginning of this year and 78% over the past three months. The stock is trading just 3% below its 52-week high of $45.83. There appears to be a bullish sentiment in general towards the stock despite the prevailing uncertainty.

Tailwinds

Like most companies in the social media and ecommerce space, Pinterest has benefited in general during the COVID-19 pandemic period witnessing growth in users and engagement levels. This trend is expected to continue going forward as the environment remains favorable for social media and ecommerce companies.

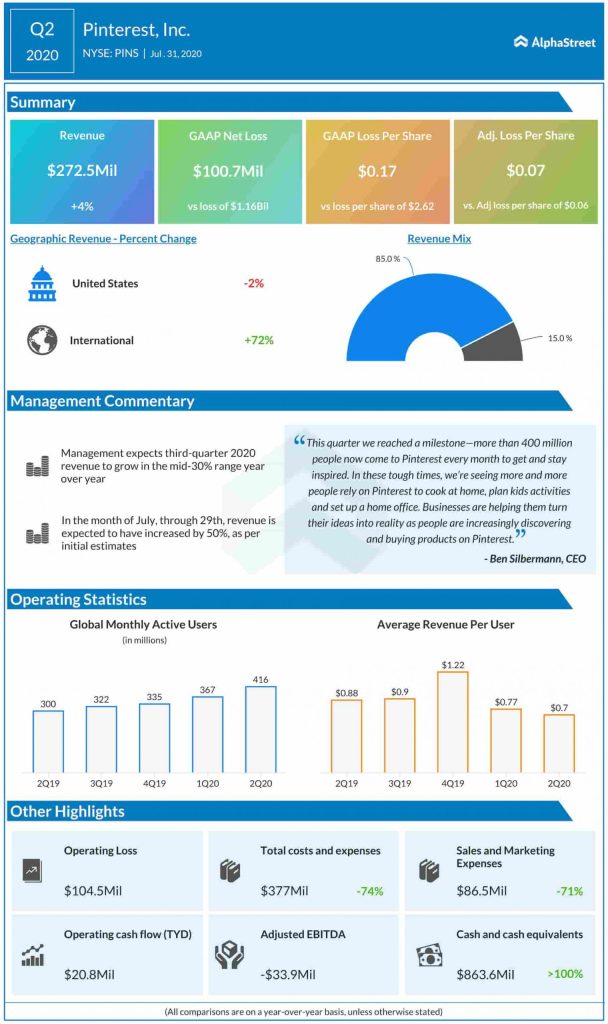

Pinterest has managed to see consistent growth in users in almost every quarter over the past three years. In the most recent quarter, monthly active users (MAU) totaled 416 million, reflecting a year-over-year increase of 39%.

Engagement levels were at their peak in mid-April and early May and although they slowed down slightly with the easing of restrictions, they still remained above pre-COVID 19 levels. In mid-July, searches were up 50% and board creates were up 40%. Users who discovered the platform during the pandemic are likely to stay on even after the crisis subsides.

In the US, MAUs increased 13% year-over-year as the company gained strength from resurrected users, meaning those who returned to the platform after a gap of several years. International MAUs jumped 49%, pointing to a strong opportunity for Pinterest for growth and expansion in regions outside the US. Pinterest also witnessed a growth in international average revenue per user which was up 21% in the second quarter of 2020.

Looking ahead, experts believe there is strong scope for growth in the online shopping space and Pinterest stands to benefit from this trend as it not only helps people find things that they need but also the means to purchase them as it connects sellers with potential buyers through its platform.

Pinterest will benefit from momentum in advertising, which is expected to pick up with the recovery in macro conditions, as the company makes efforts to optimize conversion. The company also has no outstanding debt which provides it the financial flexibility to reinvest its cash in content, ads diversification and use-case expansion.

Pinterest expects revenues to grow in the mid-30% range year-over-year for the third quarter of 2020.

Headwinds

Pinterest generates the majority of its revenue from advertising and the COVID-19 pandemic has hurt the advertising sector significantly. Although advertising is likely to see a recovery going forward, there is still uncertainty as advertisers reduce their budgets or postpone their advertising plans for the time being. This can impact Pinterest negatively.

Looking at ARPU, despite the year-over-year increase in international ARPU, it still remains much lower than the ARPU generated from the US. In Q2, US ARPU amounted to $2.50 while international ARPU was $0.14. Despite the spike in international users which help drive ARPU growth, the gap is still pretty wide. Also, decreases in domestic ARPU can hurt the company meaningfully.

Pinterest faces heavy competition in the advertising and social media space from the likes of Amazon (NASDAQ: AMZN), Facebook (NASDAQ: FB), Google, Snap (NYSE: SNAP) and Twitter (NYSE: TWTR). These companies have far more financial flexibility and resources to operate in this space and Pinterest has to keep up with them which is a challenge. Pinterest also continues to deliver net losses despite its increases in revenue which is another cause of concern for investors.

Click here to read the full transcript of Pinterest Q2 2020 earnings call