When FedEx Corporation (NYSE: FDX) reports fourth-quarter report Monday afternoon, after an unimpressive start to the year, it will likely reflect the multiple challenges the cargo giant has been facing. The market sees a 17% decrease in earnings in the May quarter to $4.93 per share. The estimate for revenues is $17.88 billion, up 3.3% from the fourth quarter of 2018.

The company, which conducts its air and ground services as two separate divisions, is on a mission to revamp facilities so as to stay relevant in the fast-changing logistics space. The initiative requires heavy investment and that will have a negative impact on the company’s cash position.

Also, margins have come under pressure from the rising operational costs, including those related to the yet-to-be-completed integration of TNT. That justifies analysts’ negative outlook for the bottom line performance. Too much strain on cash flow does not bode well for the company whose debt level is relatively unhealthy.

Margins have come under pressure from the rising operational costs, including those related to the integration of TNT

The shipping industry continues to face headwinds from the ongoing trade dispute between Washington and Beijing and the slowdown in the global economy. It needs to be noted that FedEx has high exposure to the Chinese market, where the company last year opened a center for streamlining operations.

The main operating segment that caters to the international market – FedEx Express – is estimated to have generated lower revenues in the to-be-reported quarter, as it did in the preceding quarter.

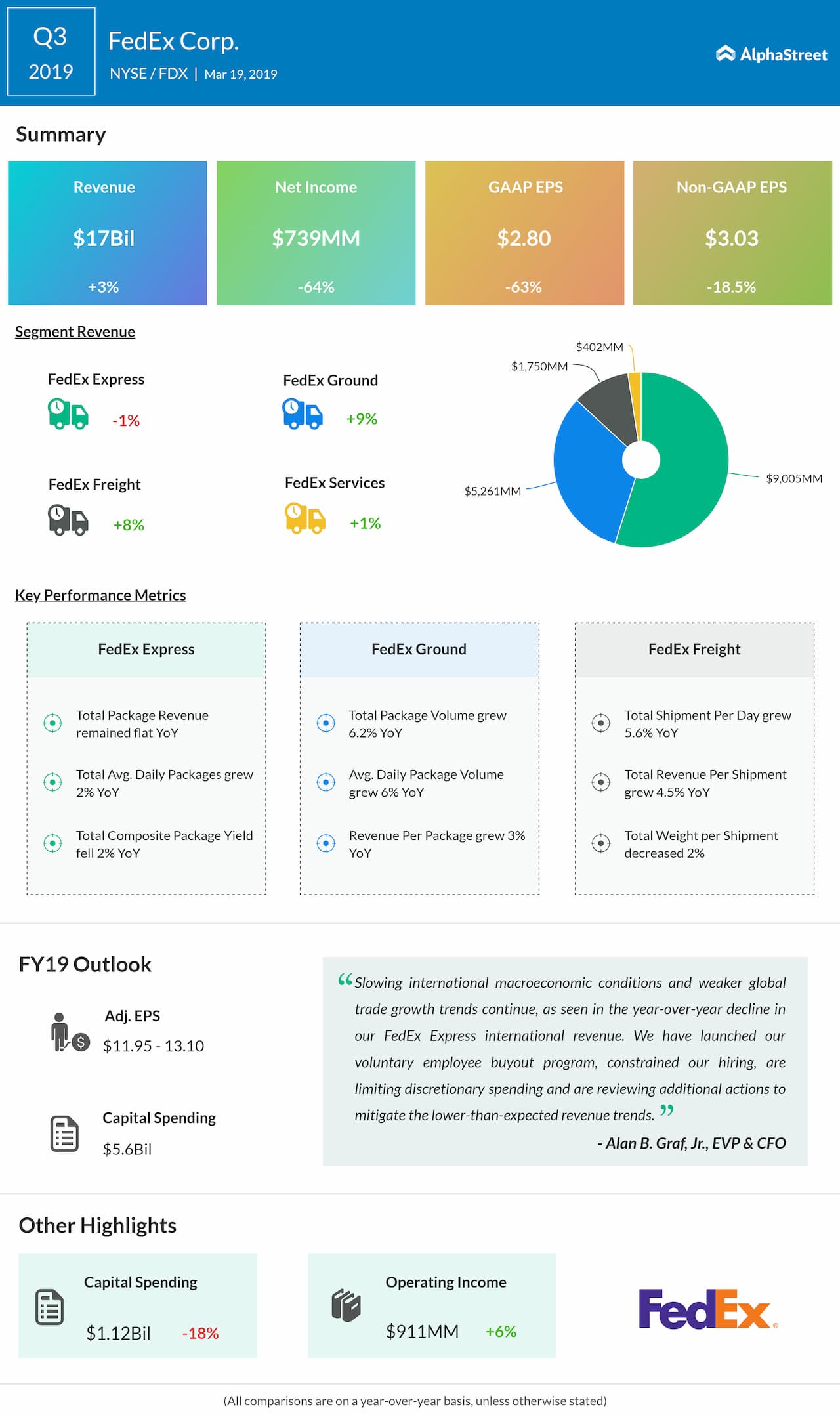

In the third quarter, the weak performance of FedEx Express was more than offset by revenue growth at the other business divisions, driving the top-line higher by 3% to $17 billion. However, earnings plunged about 19% to $3.03 per share as margins were hurt by higher costs and tax-related charges. The dismal bottom-line performance prompted the management to lower its full-year earnings guidance to $11.95-$13.10 per share.

FedEx recently severed its long-term partnership with Amazon (AMZN), whose growing interest in logistics is turning out to be a double whammy for the cargo industry. The retail giant is not only cutting down its reliance on the leading freight companies but is also doing the groundwork to compete with them.

FedEx’s arch-rival United Parcel Services (UPS) reported flat revenues of $17.2 billion for the first quarter, hurt by a marked slowdown in international operations and adverse weather conditions in North America. Consequently, earnings declined 10% annually to $1.39 per share.

FedEx stock plummeted to a six-year low last month, paring the gains it made in the early months of the year after slipping to a multi-year low towards the end of 2018. Over the past twelve months, the shares dropped about 30%, underperforming the market.