Shares of Pinterest Inc. (NYSE: PINS) have gained 211% over the past 12 months and 21% since the beginning of this year. Pinterest fared well during the pandemic and it continues to grow with the potential for expansion into areas such as ecommerce. The general sentiment around the stock is bullish and here are four factors that give good reason to keep an eye on it:

User growth and engagement

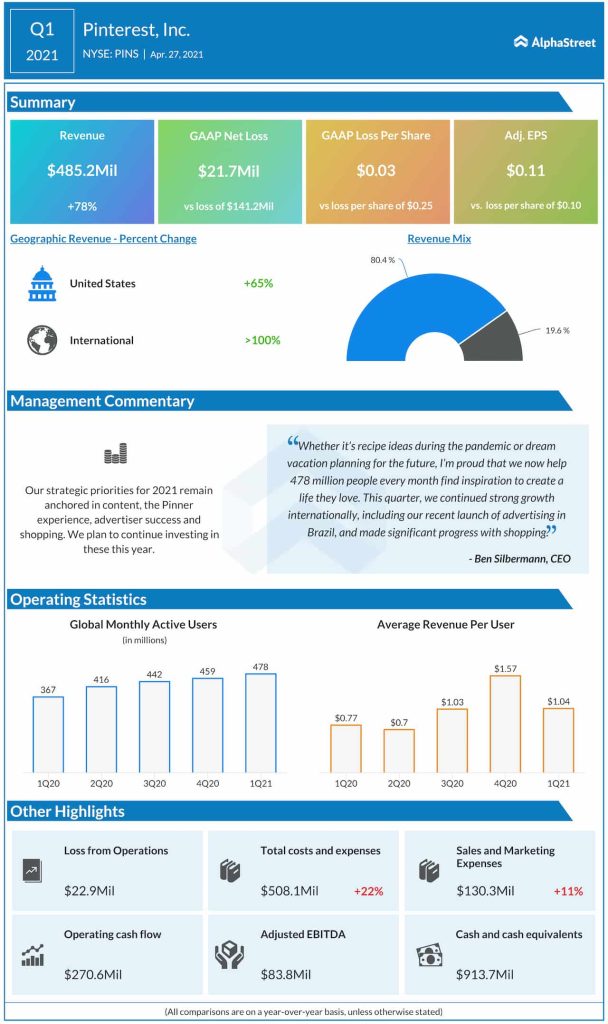

Pinterest continues to see strong user growth and engagement and it is immensely popular with the young generation, particularly those under 25. User growth and engagement gained traction during the pandemic and although it has slowed down since the crisis started to subside, the company managed to retain most of this engagement during the early part of this year. In the first quarter of 2021, monthly active users (MAU) grew 30% year-over-year to 478 million. In the US, MAUs grew 9% YoY while international MAUs were up 37% YoY. In Q2, Pinterest expects global MAUs to grow in the mid-teens.

Revenues

Pinterest continues to drive strong revenue growth. In Q1, total revenues grew 78% YoY to $485 million, nearly half of which came from small and medium-sized advertisers. Around 20% of total revenue came from international markets. Growth in number of users and average revenue per user helped drive a 170% year-over-year increase in international revenue during the first quarter. Revenues in the US rose 65% YoY driven by higher ARPU.

International expansion

Pinterest has significant potential for international expansion. The number of international users continues to grow faster than the number of US users. In Q1, international users grew 37% YoY to 380 million. International ARPU grew 91% YoY to $0.26. Although international ARPU is much less compared to US ARPU of $3.99, the rapid growth in users will help drive significant traction for the company.

Scope for ecommerce

Aside from helping people pursue various interests and projects on its platform, Pinterest is working on enabling commerce on its website. In Q1, product searches on Pinterest grew over 20 times YoY. The company believes that post-pandemic shopping engagement is likely to remain more stable than overall engagement. Pinterest plans to start on-platform transactions later this year.

According to TipRanks, the majority of analysts have rated Pinterest as Buy and the average price target on the stock is $86.33, which represents a 7.5% upside from the current level.

Click here to read the full transcript of Pinterest Q1 2021 earnings conference call