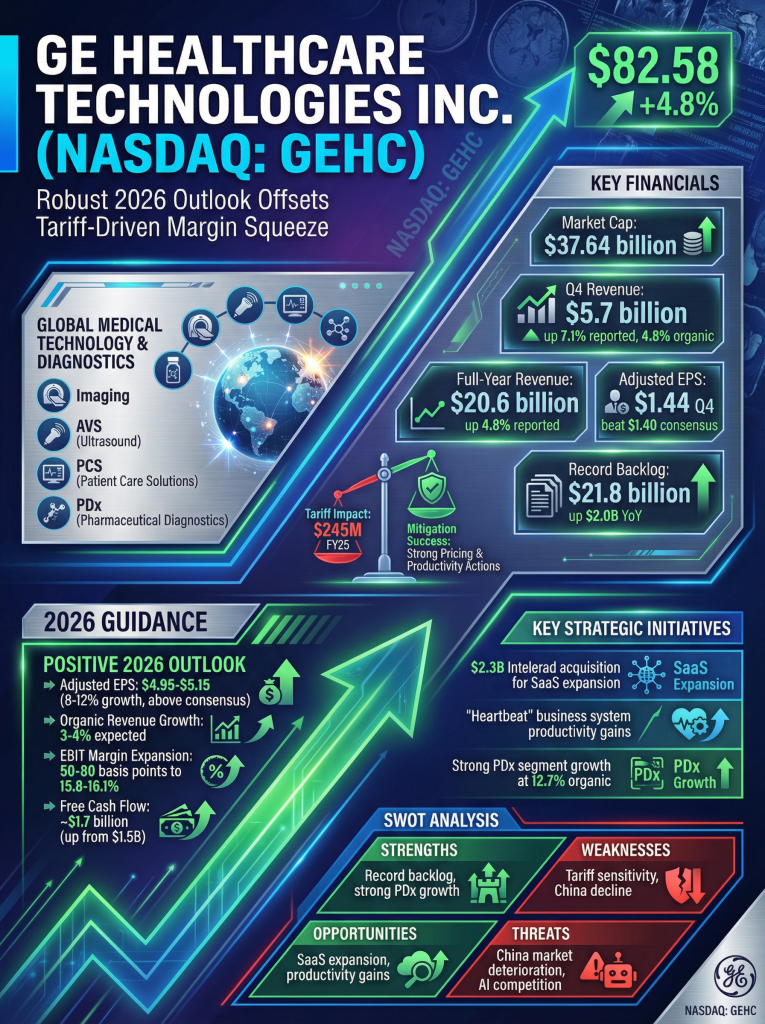

Shares of GE HealthCare Technologies Inc. (NASDAQ: GEHC) rose 4.8% to close at $82.58 on Wednesday following the release of its fourth-quarter and full-year 2025 results. The company’s better-than-expected 2026 profit guidance outweighed concerns over a year marked by significant margin contraction due to import tariffs.

Company Description

GE HealthCare Technologies Inc. is a global medical technology and pharmaceutical diagnostics company. It operates across four primary segments: Imaging, Advanced Visualization Solutions (AVS), Patient Care Solutions (PCS), and Pharmaceutical Diagnostics (PDx). The company provides medical imaging, digital solutions, and diagnostic agents to hospitals and healthcare providers globally, with its largest markets in North America, Europe, and China.

Market Performance and Valuation

- Current Stock Price: $82.58 (Close Feb 4, 2026)

- Market Capitalization: Approximately $37.64 billion

- 52-Week Context: Shares have traded between a low of $57.65 and a high of $94.80 over the past year. The stock has gained 11.5% in the last six months, significantly outperforming the broader medical device industry.

- Valuation: The stock carries a forward price-to-earnings (P/E) ratio of 17.1x. This reflects a moderate valuation as the market balances a record backlog against the “cautious” stance on China.

Fiscal Year 2025 and Q4 Financial Summary

GE HealthCare reported results for the period ended December 31, 2025:

- Q4 Revenue: $5.7 billion, up 7.1% as reported and 4.8% organically.

- Full-Year 2025 Revenue: $20.6 billion, up 4.8% as reported and 3.5% organically.

- Adjusted EPS: $1.44 for Q4, beating the $1.40 consensus estimate; full-year adjusted EPS rose 2.2% to $4.59.

- Margins: Q4 adjusted EBIT margin contracted 200 basis points to 16.7%, driven by $100 million in tariff expenses. Full-year EBIT margin was 15.3%, reflecting a total tariff impact of $245 million.

- Order Book: The company ended the year with a record backlog of $21.8 billion, up $2.0 billion year-over-year.

2026 Guidance and Forecasts

The company issued a positive outlook for the upcoming fiscal year:

- Adjusted EPS Guidance: Projected at $4.95 to $5.15, representing 8% to 12% growth and exceeding the $4.93 consensus.

- Organic Revenue Growth: Expected in the range of 3% to 4%.

- Margin Expansion: Adjusted EBIT margin is projected to expand 50 to 80 basis points to reach 15.8% to 16.1%.

- Free Cash Flow: Forecast at approximately $1.7 billion, up from $1.5 billion in 2025.

Geopolitical and Macro Pressures

- Tariff Impact: Incremental tariffs were the primary 2025 headwind, impacting adjusted EPS by $0.43. Management noted that without mitigation actions, the gross impact would have been approximately $1.75 per share.

- China Outlook: Revenue in China declined 4.6% in 2025. The 2026 outlook remains conservative, assuming continued market deterioration.

- SaaS Strategy: GE HealthCare announced the planned $2.3 billion acquisition of Intelerad to accelerate its shift toward a high-margin recurring SaaS (Software as a Service) model.

SWOT Analysis

| Strengths | Weaknesses |

| Record backlog of $21.8B provides high revenue visibility. | Margin sensitivity to U.S.-China tariffs ($245M FY25 impact). |

| Strong 12.7% organic growth in Pharmaceutical Diagnostics. | Declining revenue in China (-4.6% FY25). |

| Opportunities | Threats |

| High-margin SaaS expansion via Intelerad acquisition. | Ongoing market deterioration and volume pressure in China. |

| Productivity gains from the “Heartbeat” business system. | Intensifying competition in the AI-enabled imaging market. |