General Electric Company (NYSE: GE) is slated to release its third-quarter earnings results on Wednesday before the bell. The industrial conglomerate’s results will be hurt by constant weakness in the Power segment, poor margin from Renewable Energy, and unfavorable foreign currency movements.

Check out GE’s live earnings coverage: General Electric (GE) outpaces Q3 2019 estimates; progresses on transformation

However, the company could be positively impacted by the efforts in debt reduction and restructuring, solid international presence, and digital business. GE has decided to freeze pension plans in order to cut down debt and improve its financial position. The GE Capital business will experience solid liquidity position and lower exposure initiatives.

The top line will be hurt by sales of Industrial Solutions, Value-Based Care and Distributed Power businesses. On the other hand, the bottom line will be impacted by non-cash goodwill impairment charge, increased losses from disposed or held for sale businesses, and investments. This also includes adjusted corporate operating costs.

Analysts expect the company’s earnings to drop by 21.40% to $0.11 per share and revenue will dip by 22.5% to $22.93 billion for the third quarter. The company has surprised investors by beating analysts’ expectations twice in the past four quarters. The majority of the analysts recommended a “strong-buy” or “buy” rating with an average price target of $10.11 per share.

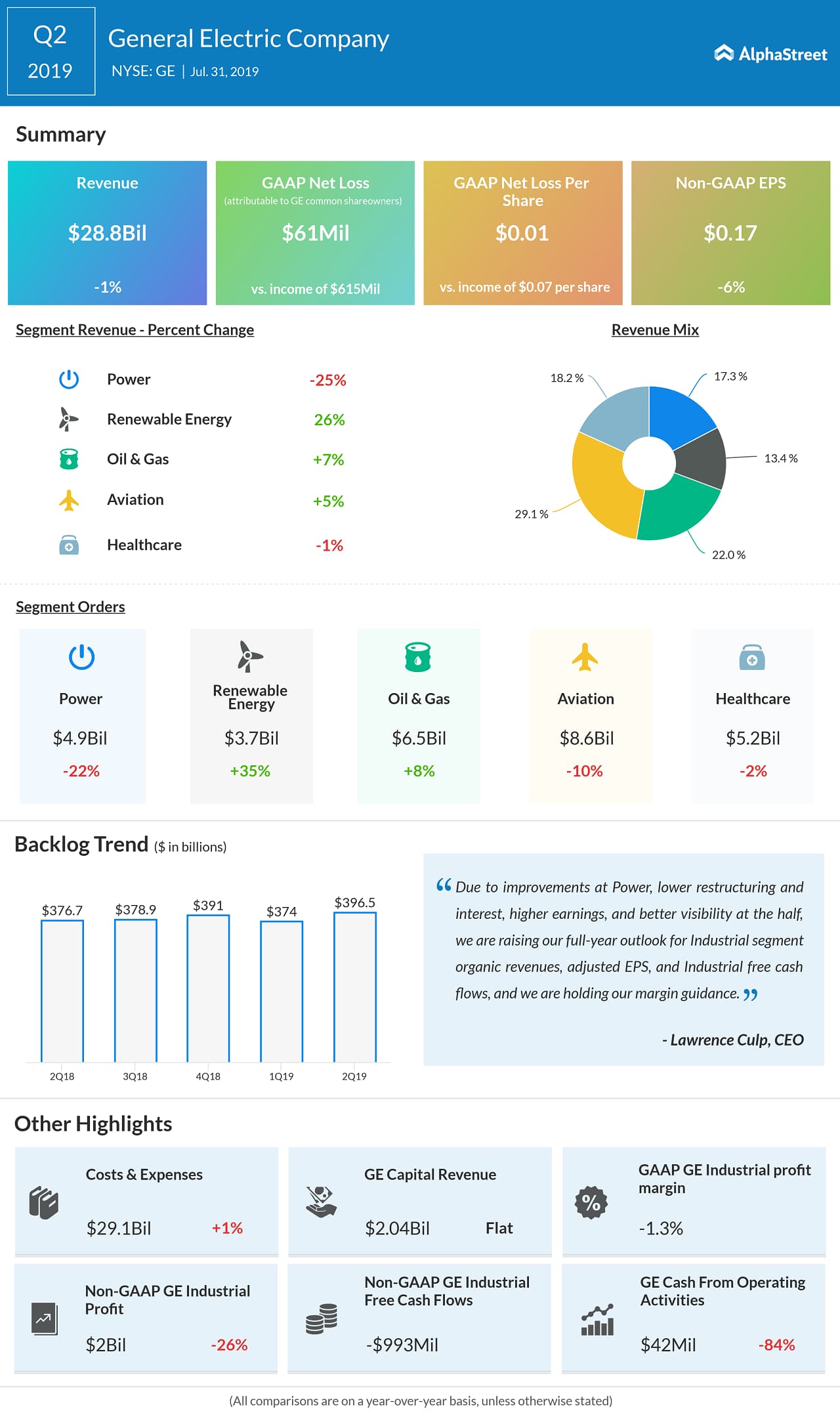

For the second quarter, General Electric slipped to a loss from a profit last year, due to a non-cash goodwill impairment charge related to Grid Solutions equipment and services. A 4% decline in the total orders dragged the total revenues down by 1%. Margins contracted due to declines in Power, Renewable Energy and to a lesser extent Aviation.

For the full year 2019, the company expects Industrial segment organic revenue growth in the mid-single digits range. Adjusted earnings are anticipated to be in the range of $0.55 to $0.65 per share for the full year. GE continues to expect adjusted Industrial free cash flow to be in positive territory in 2020 with further acceleration in 2021.