Shares of General Mills Inc. (NYSE: GIS) were up 5% on Wednesday after the company delivered fourth quarter 2022 earnings results that surpassed expectations. The stock has gained 10% year-to-date and 22% over the past 12 months. The company faced challenges from inflation and supply chain disruptions through the year and these are expected to continue into the next year as well.

Quarterly performance

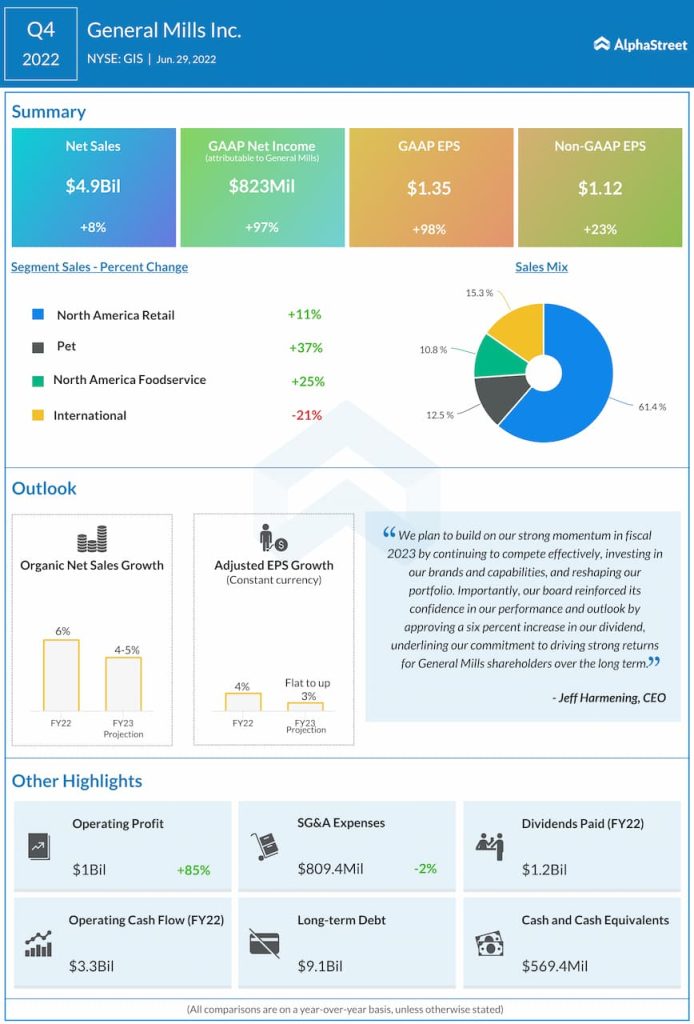

Net sales increased 8% year-over-year to $4.9 billion, beating estimates. Organic net sales rose 13%. Adjusted EPS increased 23% in constant currency to $1.12, also exceeding projections, driven by higher adjusted operating profit and lower average diluted shares outstanding. Gross margin rose 120 basis points to 36.2% helped by favorable net price realization.

Trends

Through FY2022, General Mills was able to hold or grow market share in 70% of its priority businesses including cereal, pet food and US fruits snacks. During the year, the company continued to focus on its portfolio reshaping actions which are expected to increase its top and bottom line growth profile over the long term.

The acquisitions of the Nudges True Chews and Top Chews dog treat brands from Tyson Foods and the TNT Crust frozen pizza crust business are expected to strengthen General Mills’ positions in the US pet food category and the US foodservice business.

The company is also divesting some of its slower growth businesses which will help it focus more on priority businesses. These include the divestitures of its European yogurt business and its dough businesses in Europe and Israel as well as the sale of its Helper main meals and Suddenly Salad side dishes business to Eagle Foods.

Outlook

Looking into FY2023, General Mills expects its performance to be impacted by the economic health of customers, inflation and supply chain disruptions. The company expects inflation in the upcoming year to be 14% and is working on tackling this through cost savings and price hikes.

GIS expects the impact of its portfolio reshaping transactions will lower adjusted operating profit growth and adjusted EPS growth by around 3% each in FY2023. Organic net sales for the year are expected to increase 4-5% while adjusted EPS is expected to range between flat to up 3% in constant currency. Adjusted operating profit is estimated to range between down 2% and up 1% in constant currency.

Click here to access the full transcripts of latest earnings conference calls