Shares of General Mills Inc. (NYSE: GIS) were up 2.9% on Wednesday after the company beat earnings expectations for the third quarter of 2022. Revenue, however, fell short of estimates. The company also raised its guidance for the full year based on the year-to-date performance and expectations for strong top and bottom line growth in the fourth quarter.

Quarterly performance

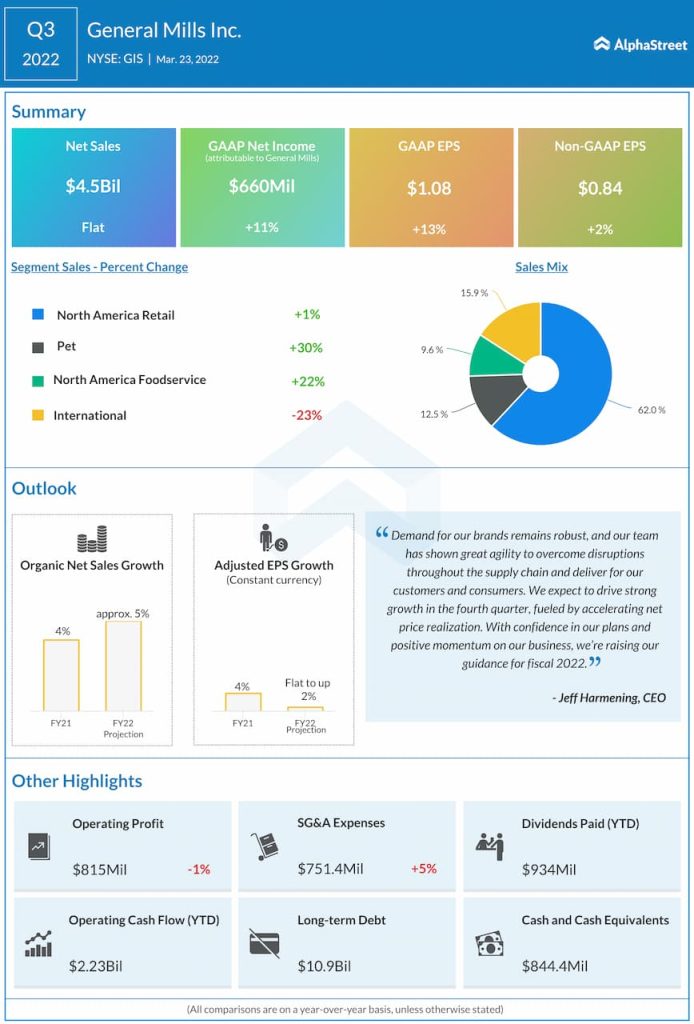

Net sales remained comparatively flat at $4.5 billion compared to last year, reflecting headwinds from acquisitions and divestitures. The top line narrowly missed estimates. Organic net sales increased 4%, driven by positive price/mix. Adjusted EPS increased 2% to $0.84, surpassing expectations. Gross margin declined 350 basis points to 30.9% of net sales, driven mainly by higher input costs.

Trends

General Mills has reorganized its segments in order to streamline its operations. The company will now report results through four new segments – North America Retail, Pet, North America Foodservice, and International.

In the third quarter, sales for North America Retail increased 1%, helped by favorable net price realization and mix. The US Cereal and US Yogurt units have been combined into a single division called US Morning Foods which recorded a sales increase of 4%. Sales in US Snacks grew 3%. Sales in the Pet and North America Foodservice segments increased 30% and 22% respectively while International sales fell 23%.

General Mills has continued to see momentum in its business through the pandemic. It has grown household penetration on many of its biggest brands and it has held or grown market share in 66% of its priority businesses thus far.

In Q3, the company recorded double-digit growth in cat food and treats and high single-digit growth in dog food and treats. Higher demand in away-from-home food channels helped drive double-digit sales growth in the North America Foodservice division.

GIS continues to face input cost inflation and supply chain disruptions but its SRM actions are expected to help offset a step-up in inflation during the fourth quarter as well as drive growth.

Outlook

General Mills expects price/mix to step up again in the fourth quarter of 2022, reflecting a full quarter of benefit from Strategic Revenue Management (SRM) actions rolled out in recent months. The company also expects double-digit input cost inflation in the fourth quarter.

General Mills raised its outlook for FY2022 and now expects organic net sales to grow approx. 5% versus its previous range of 4-5% growth. Constant-currency adjusted EPS is estimated to range between flat to up 2% compared to the previous outlook of down 2% to up 1%.

Constant-currency adjusted operating profit is expected to range between down 2% and flat versus the prior range of down 4% to down 1%. The company expects input cost inflation of 8-9% for the full year.

Click here to access the full transcript of General Mills’ Q3 2022 earnings conference call