GTIM Stock Declines 4.1% Following First Quarter Earnings Report

Shares of Good Times Restaurants Inc. (GTIM) fell 4.07% to $1.23 in midday trading on Friday. The decline follows the company’s release of its fiscal 2026 first quarter results, which highlighted a double-digit revenue contraction. The stock is currently trading near its 52-week low of $1.10, significantly below its annual high of $2.65.

Company Description

Good Times Restaurants Inc. owns and operates two distinct brands: Bad Daddy’s Burger Bar and Good Times Burgers & Frozen Custard. Bad Daddy’s is a full-service, “small box” gourmet burger concept with a full bar. Good Times is a regional quick-service restaurant (QSR) chain based primarily in Colorado and Wyoming, focused on all-natural beef and frozen custard products.

Current Stock Price: $1.23

Market Capitalization: $12.99 million

Valuation: Good Times currently trades at a forward P/E ratio of 12.5x. This valuation reflects a “micro-cap discount” compared to the broader restaurant sector, as investors weigh the company’s stable earnings against persistent negative same-store sales and a contracting top line.

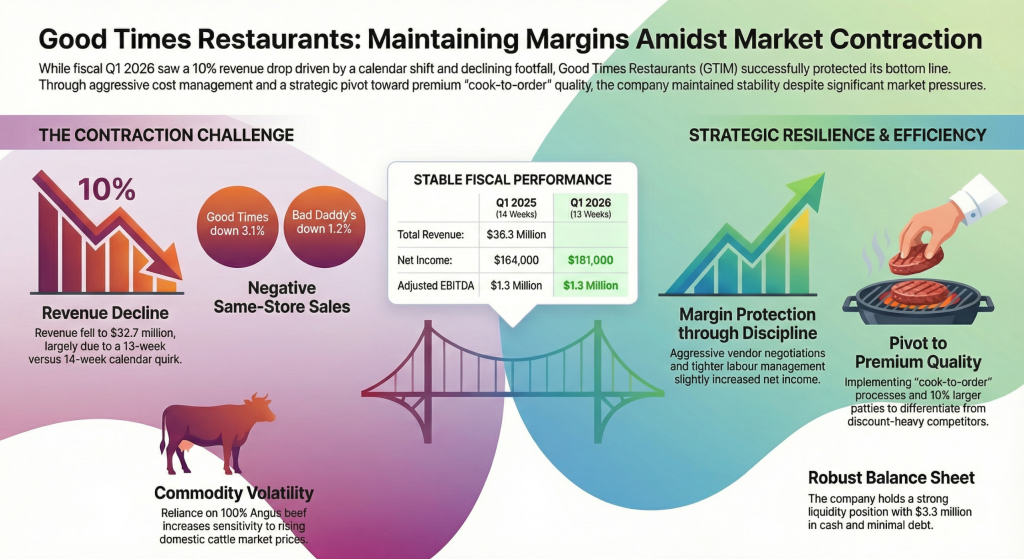

Cost Controls Sustain Profitability Amid 13-Week Calendar Shift

Good Times reported first quarter fiscal 2026 revenue of $32.7 million, representing a 10% decrease from $36.3 million in the prior-year period. Management attributed the decline primarily to a “calendar quirk,” noting that the current quarter included 13 weeks compared to 14 weeks in the first quarter of fiscal 2025.

Despite the revenue dip, the company maintained a stable bottom line. Net income attributable to common shareholders was $181,000, or $0.02 per diluted share, up slightly from $164,000 in the prior year. Adjusted EBITDA remained steady at $1.3 million. CEO Ryan Zink cited “aggressive negotiations with vendor partners” and tighter labor cost management as the primary drivers of margin resilience.

The restaurant sector continues to face broader macro pressures, specifically regarding labor inflation and shifting consumer spending patterns. GTIM faces the specific challenge of a 3.1% decline in same-store sales at its Good Times brand and a 1.2% decline at Bad Daddy’s, indicating a loss of traffic in both its QSR and full-service segments.

Analyst Consensus Remains Neutral as Volume Risks Persist

Market consensus on Good Times Restaurants remains Neutral, with no major rating upgrades or price target changes reported today. Analysts have highlighted that while the company is effectively managing its balance sheet—ending the quarter with $3.3 million in cash and only $1.8 million in long-term debt—the lack of top-line growth remains a deterrent.

To combat declining traffic, management announced a transition to a “cook-to-order” process for all burgers and a menu price increase of approximately 1.1% planned for later this year. Management expects these operational improvements to distance the brand from “mainline QSR” competitors who are currently engaging in aggressive discounting to lure price-sensitive consumers.

Supply Chain and Commodity Volatility Pressure Beef Costs

Good Times faces indirect exposure to shifting U.S. trade policies and commodity market volatility. The company’s reliance on 100% Angus beef makes it particularly sensitive to fluctuations in the domestic and international cattle markets.

In its risk disclosures, management highlighted the impact of supply chain constraints and the current inflationary environment. While the company currently sources the majority of its beef domestically, potential disruptions in agricultural trade or spikes in feed and fertilizer costs—which can be exacerbated by geopolitical instability—could lead to higher wholesale beef prices, further pressuring restaurant-level operating margins in late 2026.

GTIM SWOT Analysis

Strengths

- Balance Sheet Health: Low debt-to-equity ratio with long-term debt reduced to $1.8 million.

- Operational Discipline: Maintained steady EBITDA and slightly higher net income despite a 10% revenue decline.

- Brand Differentiation: Transition to cook-to-order and a 10% increase in burger patty size distinguishes the brand from value-tier QSR competitors.

Weaknesses

- Negative Comps: Same-store sales fell 1.2% at Bad Daddy’s and 3.1% at Good Times.

- Revenue Concentration: Heavy reliance on the Colorado and Wyoming markets leaves the company vulnerable to regional economic and weather disruptions.

- Micro-Cap Status: A market cap of ~$13 million limits institutional interest and stock liquidity.

Opportunities

- Bad Daddy’s Expansion: Potential to leverage the “small box” full-service model in high-growth markets.

- Menu Innovation: Introduction of new products like the “Giant Bavarian Pretzel” to increase average check sizes.

- Enhanced Loyalty: Partnership with Thanx to better segment and understand guest behavior to drive frequency.

Threats

- Commodity Inflation: Rising beef and packaging costs could erode recently improved margins.

- Discount Wars: Aggressive promotional pricing by larger QSR peers could further reduce market share.

- Macro Environment: Inflationary pressures and potential wage increases pose ongoing challenges to cost management.