Share Performance

Shares of Graco Inc. (NYSE: GGG) were up modestly after the manufacturer of fluid handling and coating equipment posted fourth-quarter 2025 results that met expectations and showed year-on-year growth in key metrics. The stock rose about 1.8% at $88.50 in intraday trade, off recent lows but below its 52-week high near $89.67, and above its low around the mid-$70s from late 2025.

Quarterly Results

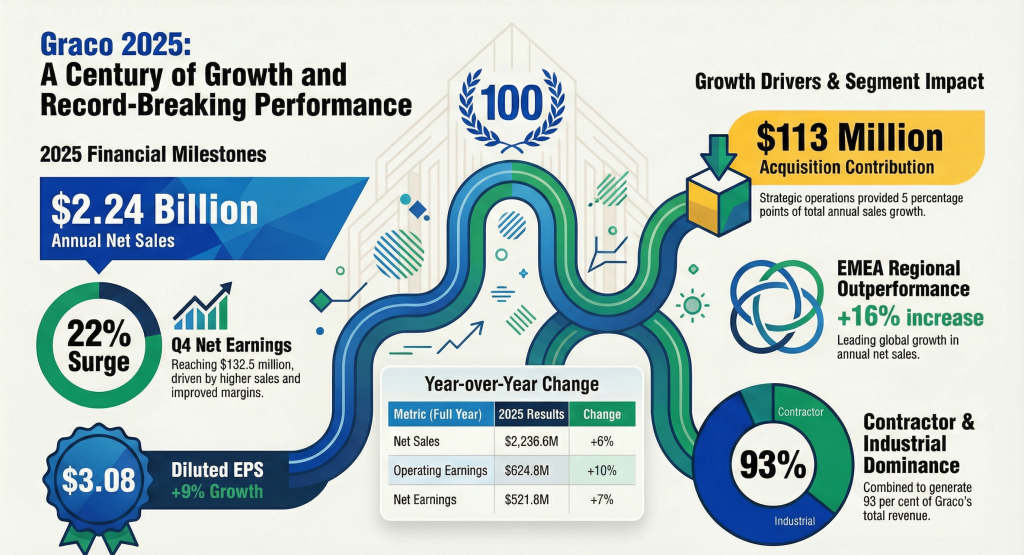

Graco reported net sales of $593.2 million in the fourth quarter ended Dec. 26, 2025, marking an 8.1% increase from $548.7 million in the year-ago period. Adjusted earnings per share came in at $0.77, in line with the consensus estimate, and up from $0.64 a year earlier. On a GAAP basis, diluted EPS was $0.79, compared with $0.63 in the prior year. Net earnings rose about 22% year-on-year to $132.5 million. Graco’s gross profit margin expanded modestly, helped by price realization that offset higher input costs.

Operating earnings for the quarter increased about 22% to $158.6 million, with operating margin improving on a year-over-year basis. The company noted contributions from acquired operations and currency benefits in its segment performance. Sales growth was broad-based across its Contractor and Industrial segments, though the smaller Expansion Markets segment saw a slight year-on-year decline.

Full-Year Performance

For the full fiscal year 2025, Graco reported net sales of $2.237 billion, up about 6% from $2.113 billion in 2024. Full-year net earnings rose roughly 7% to $521.8 million, and diluted EPS increased about 9% to $3.08. On an adjusted basis, EPS for the year was $2.95, up from $2.77 a year earlier. Operating earnings and adjusted results also showed mid-single-digit growth for the full year, supported by pricing actions and acquisitions.

Segments & Regions

Graco’s Industrial segment drove double-digit sales growth in the quarter, with an approximately 11% rise, while the Contractor segment grew about 8%. Expansion Markets sales declined about 6% on a year-over-year basis, though results were still near record quarterly levels due partly to prior strong comparisons. Regionally, sales rose in the Americas and EMEA, with Asia Pacific showing modest increases. Organic sales growth was positive but modest once acquisition and currency impacts were excluded.

Cash Flow & Capital Allocation

Graco’s operating cash flow for 2025 reached about $684 million, up from $622 million in 2024, driven in part by inventory reductions. Capital expenditures for the year were $46 million, down from $107 million the prior year. The company returned capital to shareholders through $423 million in share repurchases and $183 million in dividends during the year, ending with a net cash position of about $600 million.

Guidance

For 2026, Graco provided conservative guidance, projecting low single-digit organic growth on a constant currency basis. Management said current exchange rates could have a slightly positive impact on both net sales and earnings. The outlook does not assume additional upfront licensing revenue from electric motor technology, which management described as potentially “lumpy” in timing.

Sector & Macro Context

Graco’s results come amid broader mixed sentiment in industrial and manufacturing stocks, where capital spending patterns remain uneven across end markets. Unlike high-growth SaaS and software peers that face valuation pressure from rising interest rates and slowing enterprise IT spending, equipment manufacturers such as Graco are more closely tied to cyclical investment in infrastructure and construction. Broader macroeconomic factors including durable goods orders and commodity prices continue to influence industrial demand. There were no specific references in Graco’s report to software or SaaS pressures, though industrial peers face their own set of cost and supply chain variables.

Outlook

Investors will likely focus on Graco’s ability to sustain organic growth and margin improvements in 2026 while balancing capital returns with reinvestment needs. With results meeting expectations and showing year-on-year gains, the company’s performance underscores resilience in a mixed demand environment.