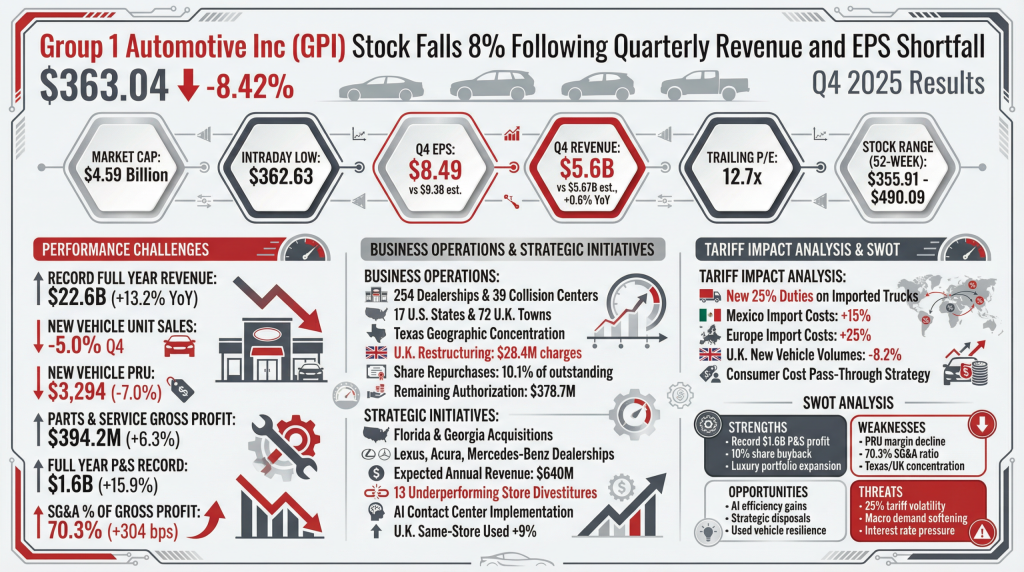

Group 1 Automotive Inc (GPI) reported fourth-quarter 2025 revenue of $5.6 billion, up 0.6% from the prior-year period but below the Zacks Consensus Estimate of $5.67 billion. Adjusted diluted earnings per share (EPS) from continuing operations fell to $8.49, missing the projected $9.38 and down from $10.02 in the fourth quarter of 2024. For the full year 2025, the company achieved record total revenue of $22.6 billion, a 13.2% increase year-over-year.

The quarterly miss was driven by a 5.0% decline in new vehicle unit sales and a 7.0% drop in new vehicle gross profit per retail unit (PRU) to $3,294. Parts and service revenue provided a partial offset, with gross profit rising 6.3% to $394.2 million in the quarter. For the full year, parts and service generated a record $1.6 billion in gross profit, up 15.9% from 2024. Selling, General and Administrative (SG&A) expenses as a percentage of gross profit rose to 70.3% for the full year, a 304-basis-point increase reflecting higher labor costs and acquisition integration.

While Group 1 is a retail-heavy entity, its performance is being evaluated against broader macro pressures often seen in high-growth software and SaaS sectors, specifically concerning rising operational overhead and “seat-count” or headcount rationalization. The company’s U.K. operations underwent restructuring in 2025, incurring $28.4 million in related charges to streamline transactional accounting and contact centers.