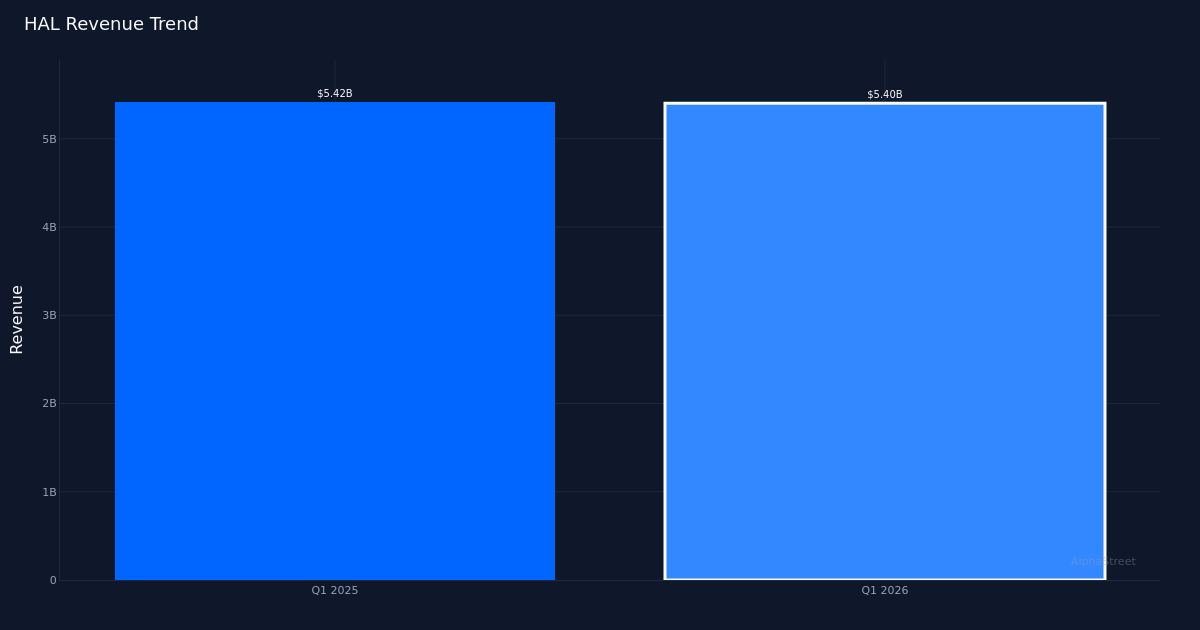

Solid Beat. Halliburton Company (NYSE: HAL) delivered Q1 2026 adjusted earnings of $0.55 per share, surpassing the $0.50 consensus estimate. The oilfield services giant generated $5.40B in revenue for the quarter against essentially flat market conditions, with net income reaching $461.0M. The earnings outperformance demonstrates management’s ability to extract profitability even as revenue remained under pressure from subdued drilling activity across key markets.

Flat Revenue Environment. The company’s weak topline reflects the challenging backdrop facing the oil and gas equipment and services sector, with revenue remaining flat year-over-year. This virtual standstill in year-over-year growth underscores the tepid investment climate as E&P operators maintain capital discipline despite relatively stable commodity prices. The absence of meaningful revenue expansion makes the earnings beat more notable, suggesting Halliburton has successfully managed its cost structure and operational efficiency to protect margins in a sideways market.

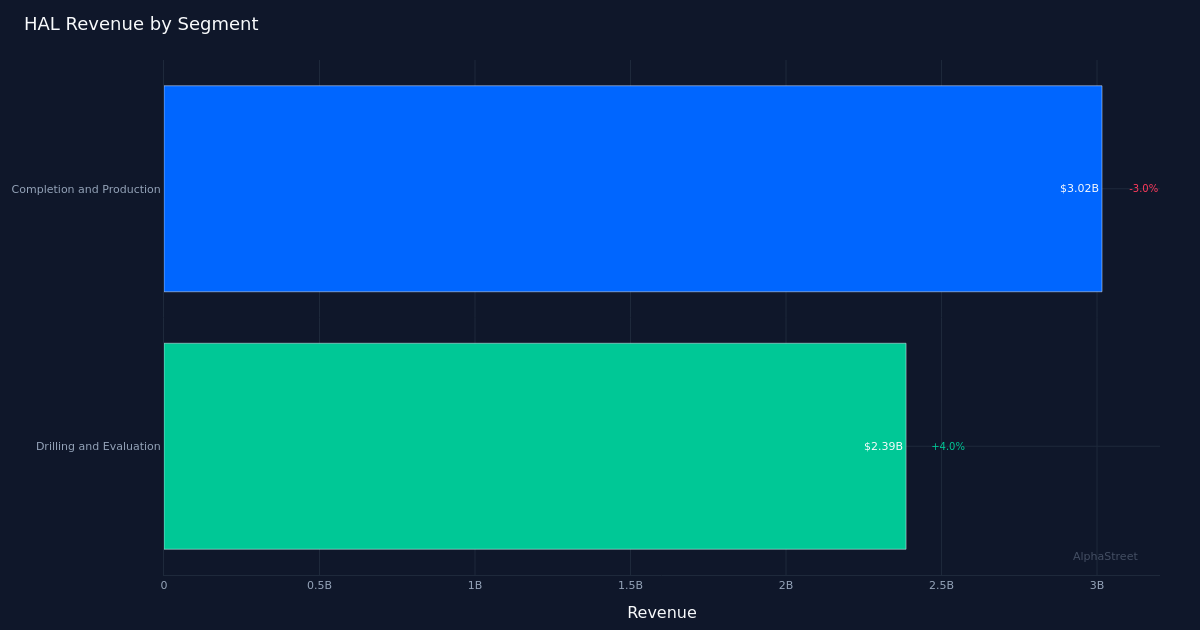

Completion and Production Pressures. The company’s largest segment, Completion and Production, generated $3.02B in revenue but experienced a 3.0% year-over-year decline. This segment, which encompasses hydraulic fracturing and completion technologies critical to unconventional resource development, faces headwinds from reduced completion activity as operators prioritize returns over growth. The modest contraction in this core business line highlights the broader industry trend toward maintenance-mode operations rather than aggressive field development, particularly in North American shale plays where completion intensity has moderated.

Market Sentiment Cautious. The stock traded at $36.68, down 1.3% following the results, suggesting investors remain focused on the revenue trajectory despite the earnings upside. Wall Street consensus stands at 16 Buy, 9 Hold, and 1 Sell ratings, reflecting a generally constructive but not overwhelmingly bullish view on the shares. The muted price reaction indicates that market participants are weighing near-term execution strength against concerns about activity levels and pricing power in a stagnant growth environment for the services sector.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.