Shares of Lowe’s Companies, Inc. (NYSE: LOW) were up over 1% on Friday. The stock has gained 19% over the past three months. The home improvement retailer saw sales and comps decline in the fourth quarter of 2023 while profits increased year-over-year. The pullback in DIY spending had a meaningful impact on the business during the quarter.

Quarterly performance

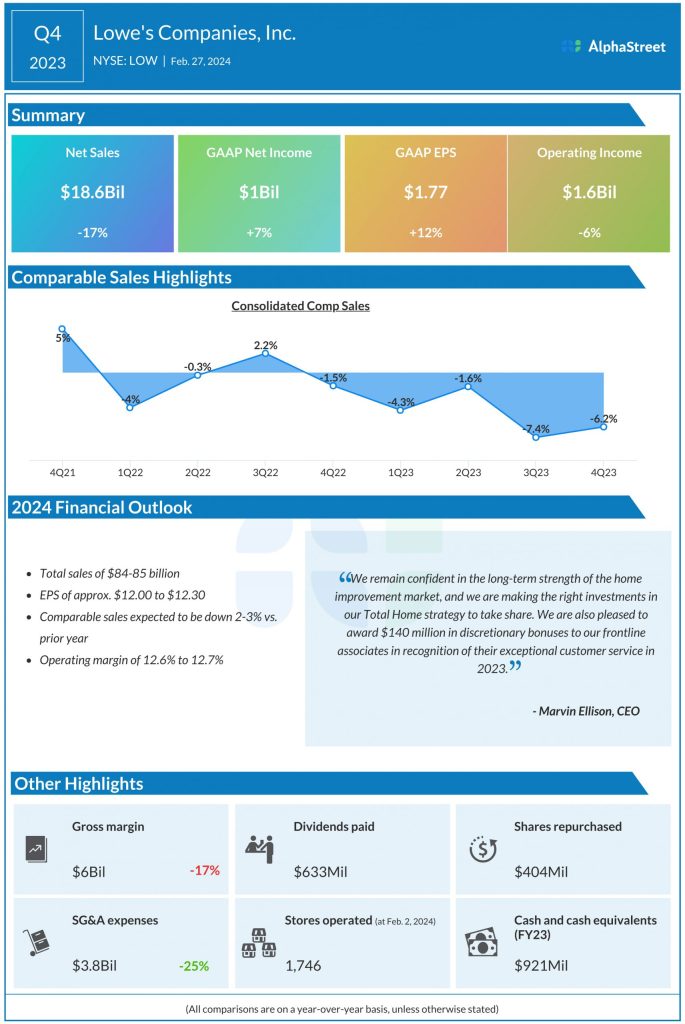

Lowe’s net sales decreased 17% to $18.6 billion in Q4 2023 compared to the same period last year. Sales in the prior-year quarter included contributions from the additional 53rd week and the Canadian retail business. Comparable sales declined 6.2% due to a slowdown in DIY demand and harsh winter weather in January. EPS increased 12% year-over-year to $1.77.

DIY spending remained pressured by factors like inflation and a stagnant housing market, with customers putting off big-ticket purchases and taking on smaller and non-discretionary projects. This impacted categories like home décor, kitchen and bath, and flooring and appliances the most.

DIY sales were also hurt by extreme weather in January, which caused a sharp drop in traffic compared to the November and December months which had witnessed an improvement from the third quarter. The slowdown in DIY and harsh January weather led to a 6.1% decline in comp transactions during the quarter.

In the Pro segment, comparable sales remained flat in Q4, despite macro headwinds and tough weather. As stated on its conference call, a recent survey by Lowe’s indicated that its Pro customers’ backlogs were in line with last year, and that they remain cautiously optimistic about their ability to generate and close leads in 2024.

Outlook

Looking ahead, Lowe’s faces uncertainty in the near term with regards to potential interest rate cuts and the pace of inflation and their impact on consumer spending. These factors, along with a depressed housing turnover, are expected to weigh on home improvement spending in 2024, particularly in the DIY segment. Pro sales are expected to outpace DIY.

For the full year of 2024, Lowe’s expects total sales of $84-85 billion and EPS of $12.00-12.30. Comparable sales are expected to decline 2-3% from last year. The company expects comp sales to remain pressured in the first half of the year due to the weak DIY demand. However, in the second half of 2024, comp sales comparisons are expected to be better year-over-year as the retailer laps a steep pullback in DIY demand seen in last year’s third quarter.

Lowe’s continues to be optimistic in its outlook for home improvement over the medium to long term as its core demand drivers – disposable personal income, home price appreciation, and the age of housing stock – remain supportive. In addition, factors like shortage of homes, millennial household formation, baby boomers aging in place, and remote work provide confidence that home improvement demand will improve over time.