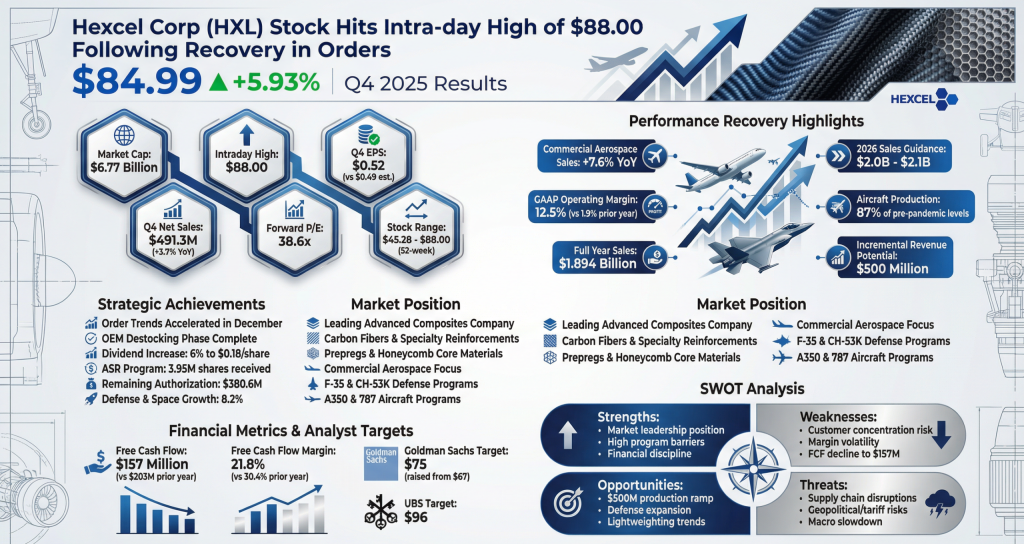

Strengths

- Market Leadership: Dominant position in carbon fiber and honeycomb reinforcements for the commercial aerospace sector.

- High Barriers to Entry: Long-term qualifications on major aircraft programs (A350, 787) provide recurring revenue.

- Financial Discipline: Consistent dividend increases and active share repurchase programs.

Weaknesses

- Customer Concentration: Heavy reliance on Airbus and Boeing production schedules; “nearly 3 times” more exposure to Airbus.

- Margin Volatility: Susceptible to unfavorable cost leverage when sales volumes or build rates fluctuate.

- Free Cash Flow Decline: Full-year 2025 free cash flow fell to $157 million from $203 million in 2024.

Opportunities

- Production Ramp: Significant revenue upside ($500 million) as OEMs move toward peak production rates in 2026–2027.

- Defense Expansion: Continued growth in international fighter and space programs.

- Lightweighting Trends: Secular demand for fuel-efficient aircraft supports long-term composite adoption.

Threats

- Supply Chain Disruptions: Ongoing fragility in the aerospace tier-two supply base could delay Hexcel’s product deliveries.

- Geopolitical/Tariff Risks: Potential for increased costs of raw materials or energy in European manufacturing hubs.

- Macro Economic Slowdown: A broader recession could lead airlines to defer new aircraft orders, impacting the current 17,000-unit backlog.