Shares of The Home Depot (NYSE: HD) have gained 9% in the past three months. The home improvement retailer is scheduled to report its earnings results for the fourth quarter of 2025 on Tuesday, February 24, before the market opens. Here’s a look at what to expect from the earnings report:

Revenue

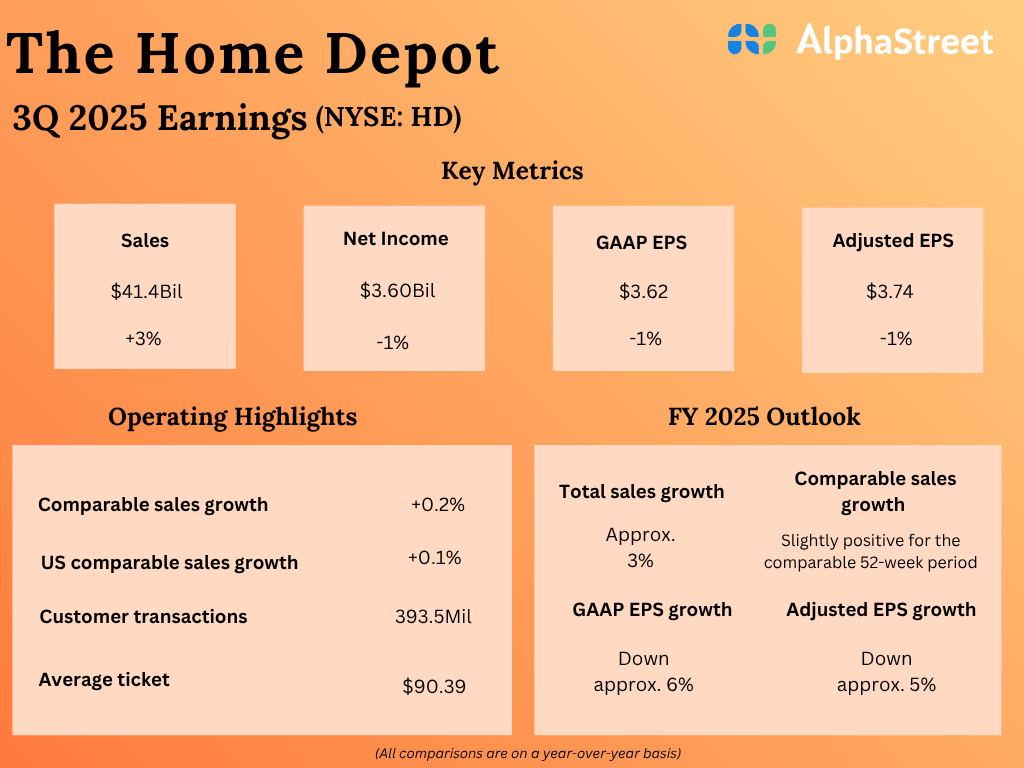

Analysts are projecting revenue of $38 billion for Home Depot in the fourth quarter of 2025, which indicates a 4% decline from the same period a year ago. In the third quarter of 2025, sales increased 2.8% year-over-year to $41.4 billion.

Earnings

The consensus estimate for earnings per share in Q4 2025 is $2.52, which implies a decrease of 16% from the prior-year period. In Q3 2025, EPS was down 1% YoY to $3.62.

Points to note

Home Depot’s results in the fourth quarter are expected to be pressured by lack of storm-related demand, economic uncertainty, and housing market headwinds. The softness in larger discretionary projects is likely to have continued as consumers put off larger repairs and remodels amid inflationary pressures.

The company has been seeing positive performances from its Pro and DIY, or do-it-yourself, customer segments. Its increased investments to boost the Pro ecosystem are expected to help expand its offerings, improve its capabilities and drive sales and growth in the segment.

The home improvement retailer continues to roll out new tools and capabilities that help Pros with their order and fulfilment needs. Its recent launches include Blueprint Takeoffs, an AI-powered tool that helps Pro customers create material lists and estimates faster and then complete all their purchases through Home Depot stores, thereby simplifying the process significantly. It also launched Material List Builder AI, another AI tool that helps Pros create lists of materials needed for entire projects.

Its acquisitions of SRS and GMS, which expand its capabilities with specialty Pro customers will also help contribute to its growth in this segment. Home Depot expects to benefit from pent-up demand once the challenges in the housing market abate and the home improvement market sees a rebound.