Shares of Hormel Foods Corporation (NYSE: HRL) have declined 26% year-to-date. The branded foods company is slated to report its earnings results for the fourth quarter of 2025 on Thursday, December 4, before the markets open. Here’s a look at what to expect from the quarterly report:

Revenue

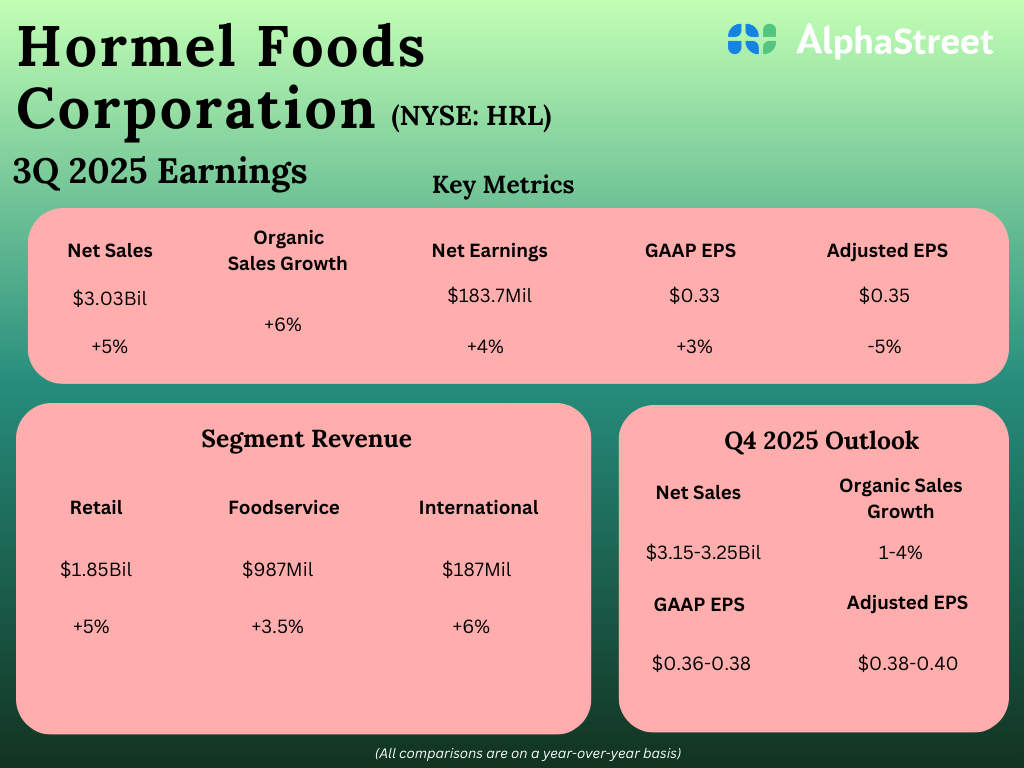

Hormel has guided for net sales to range between $3.15-3.25 billion in the fourth quarter of 2025. Analysts are projecting revenue of $3.24 billion for Q4, which indicates a growth of over 3% from the same period a year ago. In the third quarter of 2025, net sales increased nearly 5% year-over-year to $3.03 billion.

Earnings

Hormel has guided for adjusted earnings per share to range between $0.38-0.40 in Q4 2025. Analysts are predicting EPS of $0.31, which implies a decline of 26% from the year-ago quarter. In Q3 2025, adjusted EPS decreased 5% YoY to $0.35.

Points to note

Hormel continues to operate in a dynamic consumer environment, and although the food company’s top line is benefiting from its strong brand portfolio, higher input costs are weighing on its bottom line.

Hormel has guided for organic sales growth of 1-4% in the fourth quarter of 2025. The company expects continued sales growth supported by its leading positions in the marketplace. The Planters brand and the turkey portfolio are expected to be strong growth drivers of the top line.

In Q3, Hormel’s organic sales rose 6%, marking the third consecutive quarter of organic sales growth. This growth was broad-based, driven by all its segments. Last quarter, the company saw sales increase across all its segments, helped by the strong performance of its brands.

In the Retail segment, brands such as Wholly guacamole, SPAM, Black Label bacon, and Applegate, saw strong consumer volume demand. The Jennie-O lean ground turkey business benefited from consumers’ preferences for lean, affordable protein. The International segment witnessed growth driven by momentum in the China market. This segment continues to benefit from innovation in the snacking portfolio.

The Foodservice segment saw sales growth helped by gains from Planters snack nuts, Jennie-O turkey, and Hormel pepperoni. However, this segment continues to face pressure from soft traffic, inflation, and shifts in consumer behavior.

Hormel’s bottom line continues to be pressured by higher commodity input costs. The company is taking targeted pricing actions to counter this commodity inflation. It expects to see a recovery in profit only in the next year, as the pressures seen in the third quarter are anticipated to have persisted through the fourth quarter. Hormel has guided for GAAP EPS to range between $0.36-0.38 in Q4 2025. HRL is expected to see benefits from its Transform and Modernize initiative, which is projected to deliver $100-150 million of incremental benefits in fiscal year 2025.