Shares of Hormel Foods Corporation (NYSE: HRL) gained over 3% on Thursday. The company delivered mixed results for the fourth quarter of 2025, as earnings came ahead of expectations while revenue fell short. The branded foods provider expects top line growth in the upcoming fiscal year. The bottom line is expected to remain pressured in the first quarter and then see a recovery thereafter.

Earnings beat, revenues miss

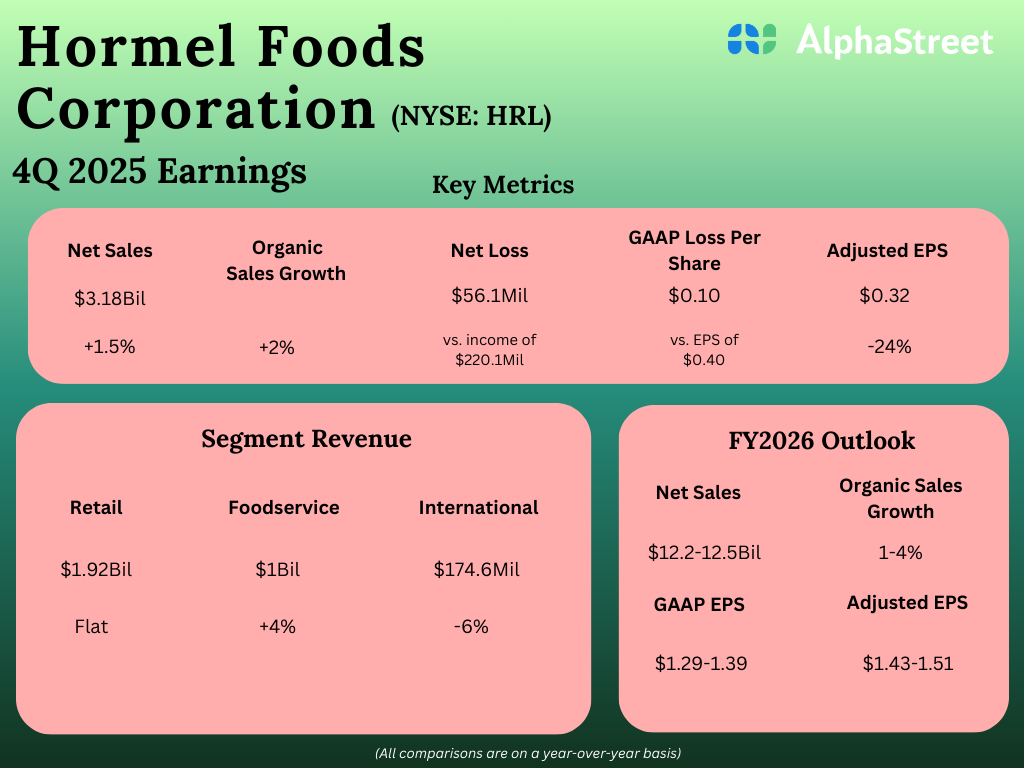

Hormel reported net sales of $3.18 billion for the fourth quarter of 2025, which was up 1.5% from the previous year but below estimates of $3.24 billion. Organic sales grew 2%. On a GAAP basis, the company posted a net loss of $0.10 per share. On an adjusted basis, earnings per share fell 24% year-over-year to $0.32, but managed to surpass projections of $0.31.

Brand strength

In Q4, Hormel’s top line benefited from strength in its brand portfolio while its bottom line continued to be pressured by persistent input cost inflation as well as a challenged consumer environment.

During the quarter, sales in the Retail segment grew 1%, driven by gains from the turkey portfolio, and the Planters and Applegate brands. These were partly offset by the discontinuation of certain private label snack nuts offerings.

In Foodservice, sales increased 4% on a reported basis and 6% on an organic basis. Organic sales growth was driven by gains from the customized solutions business, branded bacon and pepperoni, premium prepared proteins, and the Jennie-O turkey portfolio. This segment continues to benefit from a wide range of products and a diverse channel presence.

The International segment saw sales decline 6%, as growth in SPAM luncheon meat and the refrigerated portfolio was more than offset by declines in fresh pork exports. While the company saw volume and sales growth in China, it experienced competitive pressures in Brazil during Q4.

Top and bottom line growth next year

For fiscal year 2026, Hormel expects net sales to range between $12.2-12.5 billion. Organic sales are expected to grow 1-4%. The company expects sales growth for all its segments despite a pressured consumer environment. The Retail segment is expected to see low-single-digit organic sales growth for the year. The Foodservice segment is expected to see sales growth in the mid-single-digits while the International segment is projected to see high-single-digit sales growth.

HRL expects to see continued earnings pressure in the first quarter of 2026 and a growth in earnings for the remainder of the year. The company expects GAAP EPS of $1.29-1.39 for FY2026. Adjusted EPS is expected to range between $1.43-1.51, representing a growth of 4-10%.