With the economic slowdown extending into the new fiscal year, the technology sector continues to be impacted by the fall in IT spending. The latest quarterly report of PC maker HP Inc. (NYSE: HPQ) — marked by lower sales and squeezed margins — is indicative of the challenges facing the industry.

This week, The Palo Alto-based IT hardware company’s stock traded sharply below last year’s peak and the downtrend continued after it reported unimpressive numbers for the first quarter. Going by the unfavorable demand scenario, shareholders would have to wait for some time before getting better returns. It makes sense not to sell the stock now because HP’s initiatives to stay relevant in the promising IT market would pay off in the long run. The time is not ripe to buy either, due to lingering uncertainties.

Future Ready

The management is optimistic about the business effectively navigating the current headwinds, supported by the recently announced Future Ready plan that envisages strategic long-term investments while reducing costs. It expects the second half of the year to be stronger than the first half.

Meanwhile, the cost cuts, combined with sales recovery in China where the market is fast returning to the pre-COVID levels, should boost margins in the near term. The company issued second-quarter adjusted earnings above estimates and maintained its full-year guidance.

HP Inc. Q1 2023 Earnings Call Transcript

“The Future Ready plan we shared with you last quarter is already having an impact. As a reminder, the plan has two primary objectives. One is to further reduce our cost structure. The second is to continue to assess and optimize our overall portfolio and to develop the required operational capabilities to deliver long-term sustainable growth. We are making clear progress in both areas. In terms of costs, our teams have done an excellent job reducing spend and driving efficiencies,” said HP’s CEO Enrique Lores at the earnings call.

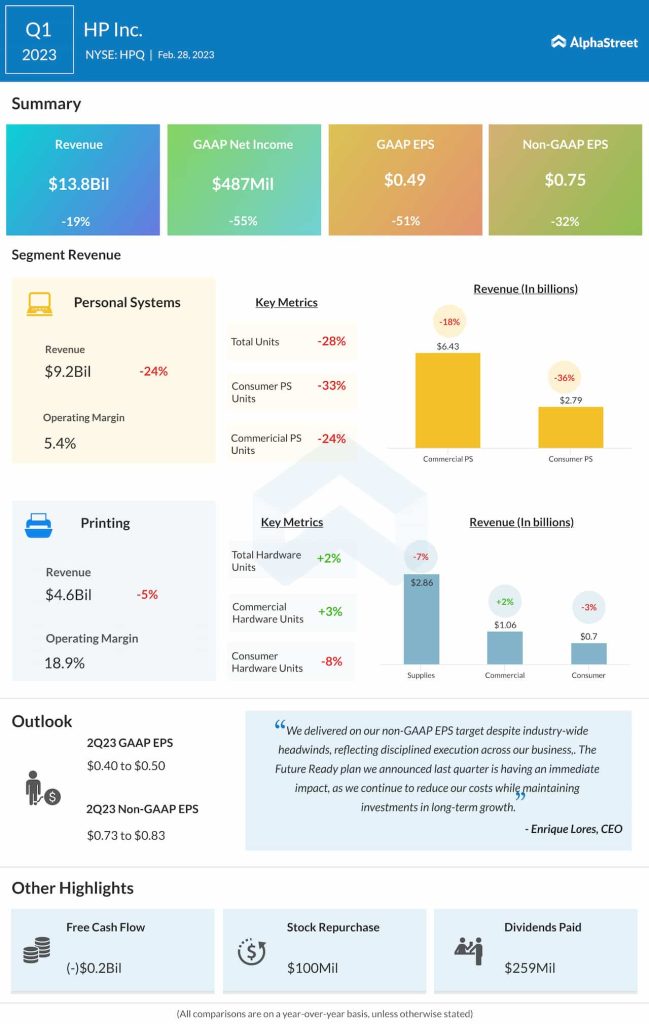

Financial Performance

First-quarter revenues declined 19% annually to $13.8 billion, which translated into a sharp fall in adjusted earnings to $0.75 per share. Both the Personal Systems and Printing segments contracted during the quarter but the latter fared relatively better, especially in the commercial segment. However, net profit exceeded the market’s projection by a penny, while the top line missed the estimates. The beat is significant since the bottom line had either missed or matched estimates in the trailing three quarters.

The stock traded lower on Wednesday, reflecting the muted investor sentiment. It has been languishing below the 52-week average for quite some time, and has lost about 20% in the past twelve months.