Independent Bank Corporation (NASDAQ: IBCP), a Michigan-based bank holding company with $5.5 billion in total assets, reported fourth quarter 2025 net income of $18.6 million, or $0.89 per diluted share. The company announced strong operational metrics including net interest margin expansion and robust loan growth. The Board of Directors authorized a 5% stock repurchase plan, demonstrating confidence in the organization’s earnings trajectory and capital strength.

MARKET POSITION AND COMPANY OVERVIEW

Independent Bank Corporation operates through its subsidiary, Independent Bank, as a state-chartered bank providing comprehensive financial services across Michigan’s Lower Peninsula. Founded as First National Bank of Ionia in 1864, the organization maintains total assets of $5.51 billion as of December 31, 2025. The bank serves as a significant financial institution in the regional banking sector, offering commercial banking, mortgage lending, investment, and insurance services.

LATEST QUARTERLY RESULTS — Q4 2025

Financial Performance Highlights

1. Net Income: Fourth quarter 2025 net income totaled $18.6 million, or $0.89 per diluted share, compared to $18.5 million, or $0.87 per diluted share in the prior-year period. Full-year 2025 net income reached $68.5 million, or $3.27 per diluted share, versus $66.8 million, or $3.16 per diluted share in 2024.

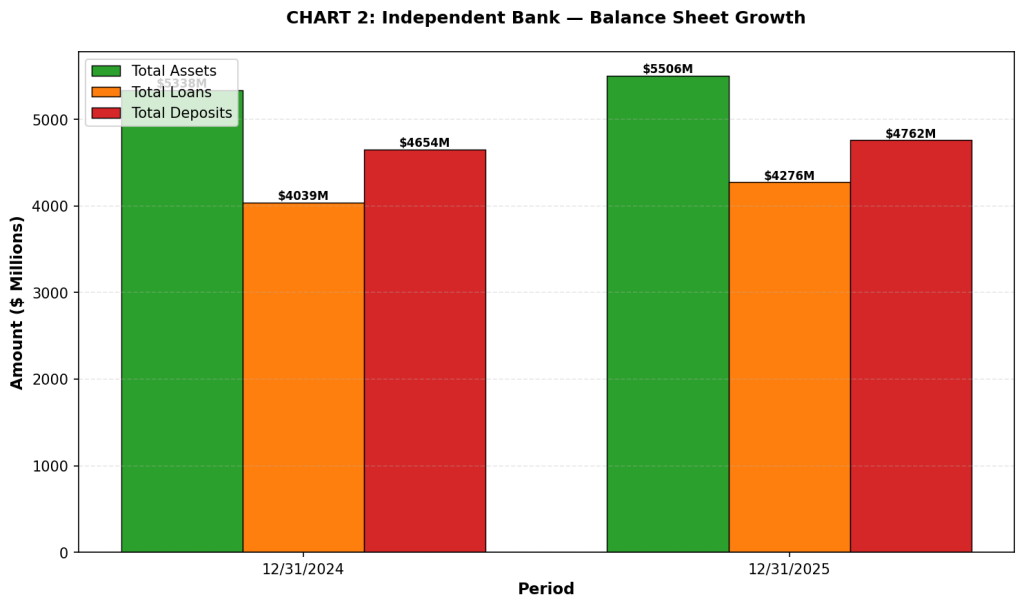

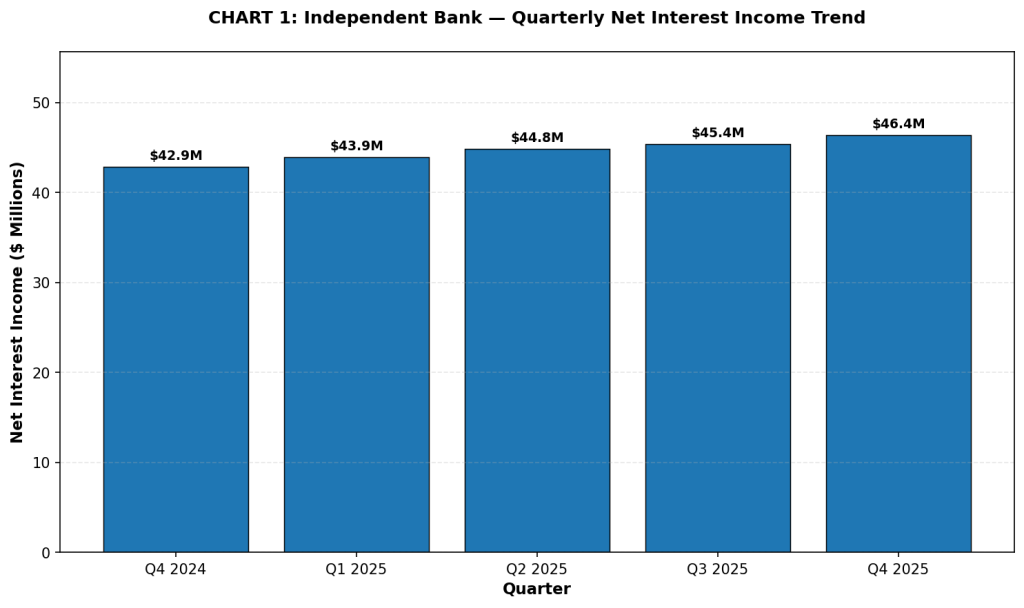

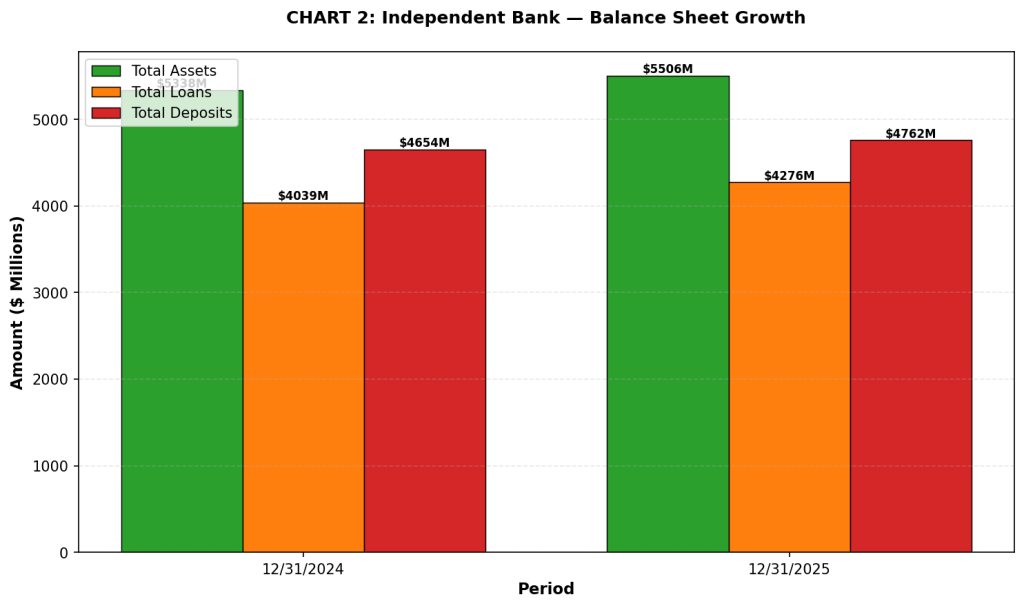

2. Net Interest Income: Q4 2025 net interest income totaled $46.4 million, an increase of $3.5 million, or 8.2%, compared to the year-ago period. This represents an increase of $1.0 million, or 2.2%, from Q3 2025. Full-year 2025 net interest income totaled $180.0 million, an increase of $13.8 million, or 8.3%, from 2024.

3. Net Interest Margin: The net interest margin for Q4 2025 was 3.62%, representing an eight basis point increase from the linked quarter and 17 basis points above the year-ago period. Full-year 2025 net interest margin improved to 3.56% from 3.38% in 2024.

4. Return on Assets and Equity: Q4 2025 return on average assets was 1.35% and return on average equity was 14.75%, reflecting strong profitability metrics. Tangible common equity ratio increased to 8.65% as of December 31, 2025.

Loan and Deposit Growth

Net growth in loans during Q4 2025 totaled $78.0 million, representing annualized growth of 7.4% from September 30, 2025. Total loans reached $4.28 billion at December 31, 2025, compared to $4.04 billion at year-end 2024, primarily driven by growth in commercial loans. Net growth in total deposits, excluding brokered deposits, was $57.1 million during Q4 2025, representing annualized growth of 4.8% from September 30, 2025. Total deposits reached $4.76 billion at December 31, 2025, an increase of $107.6 million from year-end 2024.

Key Business Metrics

· Commercial Loans: Commercial loan portfolio totaled $2.21 billion at December 31, 2025, compared to $1.94 billion at year-end 2024. Strong growth in commercial lending reflects the organization’s strategic focus on this high-value segment.

· Mortgage Lending: Mortgage loan portfolio totaled $1.52 billion at December 31, 2025, compared to $1.52 billion at year-end 2024. Mortgage lending activities remained relatively stable with quality originations throughout the period.

· Capital Strength: Shareholders’ equity totaled $503.0 million, or 9.14% of total assets at December 31, 2025, compared to $454.7 million, or 8.52% at year-end 2024. Tangible common equity reached $473.7 million, or $23.05 per share, compared to $424.9 million, or $20.33 per share at year-end 2024.

· Asset Quality: Non-performing loans totaled $23.1 million, or 0.54% of total portfolio loans at December 31, 2025. The allowance for credit losses totaled $63.4 million, or 1.48% of total portfolio loans, compared to $59.4 million, or 1.47% at year-end 2024.

FINANCIAL TRENDS — CHARTS

The following charts present Independent Bank Corporation’s operating performance and market trends.

Chart 1: Quarterly Net Interest Income Trend

Note: Net Interest Income presented represents quarterly consolidated operations. Values reflect total interest income less interest expenses across all banking operations.

Chart 2: Balance Sheet Growth Comparison

Note: Balance sheet metrics reflect consolidated financial position at period end. Asset growth driven by increased loan portfolio and operational expansion.

BUSINESS & OPERATIONS UPDATE

· Commercial Banking Division: Primary revenue source from commercial lending across Michigan’s Lower Peninsula. Strong commercial loan growth of 14.2% year-over-year demonstrates expansion in this strategic segment. Commercial relationships represent significant portion of net loan growth with emphasis on relationship-based lending.

· Mortgage Banking Operations: Residential mortgage lending continued throughout the period with quality originations. Mortgage servicing operations generated income of $0.9 million in Q4 2025. Mortgage banking contributed to diversified revenue streams and customer relationship expansion.

· Deposit Franchise Strength: Core deposit gathering focused on relationship-based approach with growth in savings, interest-bearing checking, and business deposits. Deposit base totaled $4.76 billion with stable customer retention across all regions.

· Capital Returns to Shareholders: Board of Directors authorized 2026 share repurchase plan authorizing purchase of 1,100,000 shares, approximately 5% of outstanding common stock. During 2025, the company repurchased 407,113 shares at aggregate cost of $12.4 million.

CREDIT QUALITY AND ASSET QUALITY METRICS

Independent Bank maintains disciplined credit risk management with non-performing loans of $23.1 million, or 0.54% of total portfolio loans. The allowance for credit losses to total non-performing loans ratio of 274.33% demonstrates conservative provisioning practices. Credit quality metrics improved from prior periods with appropriate reserves established across the portfolio. The provision for credit losses was $1.9 million in Q4 2025 compared to $2.2 million in Q4 2024, reflecting manageable credit trends.

LIQUIDITY, CAPITAL STRENGTH & REGULATORY POSITION

Independent Bank maintains strong liquidity and capital positions well above regulatory requirements. The bank’s subsidiary remains significantly above “well capitalized” status with Tier 1 capital to average total assets of 9.36%, compared to the 5.00% well-capitalized minimum. Tier 1 common equity to risk-weighted assets totaled 11.24%, exceeding the 6.50% requirement. Total capital to risk-weighted assets reached 12.49%, above the 10.00% well-capitalized threshold. The organization maintains approximately $774.2 million in unused FHLB credit lines and $1.24 billion in FRB credit availability.

OPERATIONAL PERFORMANCE & EFFICIENCY METRICS

Non-interest expenses totaled $36.1 million in Q4 2025, compared to $37.0 million in the prior-year quarter, reflecting improved operational efficiency and cost management. Full-year 2025 non-interest expenses totaled $138.2 million versus $135.1 million in 2024. The company continues to balance necessary technology investments with disciplined expense management. Operating metrics demonstrate the organization’s ability to generate strong earnings while maintaining competitive service delivery.

GUIDANCE AND OUTLOOK CONSIDERATIONS

· Loan Growth: Management projects continued commercial loan growth driven by strong pipeline and market expansion in Michigan region. Loan originations expected to continue with disciplined underwriting standards.

· Deposit Growth: The organization expects continued deposit growth from relationship-based gathering strategies. Mix of deposit products supports customer convenience and competitive positioning.

· Net Interest Margin: Net interest margin benefited from balance sheet repricing and improved interest rate environment. Future margin subject to Federal Reserve policy and competitive rate dynamics.

· Capital Management: Strong capital position supports 5% share repurchase plan and dividend distributions. Capital generation from earnings retention provides flexibility for strategic initiatives.

· Regulatory Environment: Banking regulatory framework continues to evolve with compliance requirements impacting profitability. Management maintains proactive approach to regulatory developments.

PERFORMANCE SUMMARY

Independent Bank Corporation demonstrated strong financial performance in fourth quarter 2025 with substantial net interest income growth and margin expansion. Net income of $18.6 million reflects operational excellence and disciplined management across core banking operations. Loan portfolio growth of $237.5 million year-over-year and deposit growth of $107.6 million underscore the organization’s market position and customer relationships. Asset quality metrics remain stable with conservative credit provisioning. Capital strength and liquidity position provide platform for continued growth and shareholder returns. The Board’s authorization of 5% share repurchase plan reflects confidence in earnings trajectory. Management positioned to capitalize on regional market opportunities while maintaining disciplined risk management. Founded in 1864 as First National Bank of Ionia, the organization brings 160+ years of banking experience to Michigan markets.