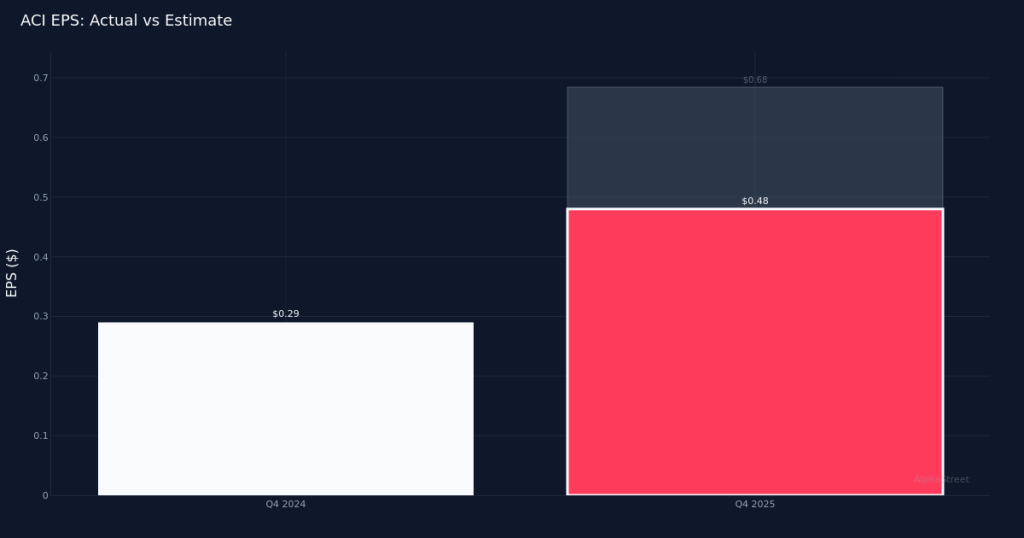

Albertsons delivered a stark earnings miss in Q4 2025, falling 29.4% short of analyst expectations despite posting strong year-over-year revenue growth. The grocery chain reported adjusted EPS of $0.48 versus the $0.68 consensus estimate, a disappointing result that sent shares down 3.1% to $16.32. While revenue climbed 7.8% to $20.25 billion from $18.80 billion in the year-ago period, the quality of that growth deteriorated significantly as operational efficiency eroded and financing costs mounted.

The earnings miss reflects fundamental margin compression rather than top-line weakness, exposing the fragility of Albertsons’ operating model in the current environment. Net margin collapsed from 0.9% a year ago to negative 2.4% in the current quarter, a striking 3.3 percentage point deterioration. Operating margin similarly turned negative at -2.5%, suggesting the company faced severe operational headwinds that overwhelmed revenue gains. This stands in sharp contrast to the bottom-line EPS performance, which actually surged 65.5% year-over-year from $0.29 to $0.48. The divergence between improving EPS and collapsing margins signals that this quarter’s results reflect unusual items or calendar effects rather than sustainable operational improvement. Gross margin dropped to 27.2% from 27.4% in the year-ago quarter.

Revenue growth accelerated modestly on a nominal basis, but identical sales growth of just 0.7% reveals anemic organic momentum. The 7.8% reported revenue increase substantially outpaced the identical sales figure, indicating that much of the growth came from non-comparable sources—likely the extra week in the fiscal calendar referenced by management. This calendar quirk makes year-over-year comparisons treacherous and suggests underlying business momentum remains weak. The 0.7% identical sales growth barely outpaced inflation and reflects the brutally competitive grocery landscape where price wars and promotional intensity continue to pressure market share. With 2,244 total retail stores in the portfolio, Albertsons’ store productivity appears to be stagnating rather than improving.

Rising interest expense emerged as a significant earnings headwind, though management took proactive steps to address the capital structure. According to management commentary, “Q4 interest expense increased $40 million to $141 million, compared to $101 million last year, due to higher borrowings and the extra week in the fourth quarter of 2025 compared to 2024.” This 40% increase in interest costs directly pressured profitability and helps explain the margin compression despite revenue growth. Management attempted to mitigate future pressure by refinancing, noting: “Finally, in the fourth quarter, we opportunistically refinanced $2.1 billion of existing bonds in two tranches, $1.2 billion of 5.625% notes due 2032 and $900 million of 5.75% tack-on notes due 2034.” While this extends maturities and provides breathing room, the elevated absolute level of interest expense will continue to constrain earnings power.

Cash generation remained robust despite the margin weakness, providing some reassurance about underlying business health. Operating cash flow reached $2.37 billion in the quarter, and free cash flow of $527.3 million demonstrates the company’s ability to convert sales into cash even while reported margins turned negative. This cash generation capability suggests the negative margins may indeed reflect timing issues, one-time costs, or calendar effects rather than fundamental business deterioration. The substantial gap between operating cash flow and free cash flow implies heavy capital investment, consistent with management’s references to productivity initiatives.

Fiscal 2026 guidance of $2.22 to $2.32 in adjusted EPS appears conservative but signals limited visibility into margin recovery. The midpoint of $2.27 translates to quarterly earnings of roughly $0.57, only modestly above the current quarter’s $0.48 result. This tepid outlook suggests management does not anticipate rapid margin expansion or significant operating leverage in the coming year. Management attempted to project confidence, stating: “Adjusted EBITDA is expected to be in the range of $3.85 billion to $3.925 billion, representing growth of approximately 2.5% at the top end of the range, excluding the 53rd week impact in 2025.” The emphasis on excluding the calendar benefit highlights how modest underlying growth expectations truly are. Management also emphasized productivity efforts, noting: “And, again, as I mentioned before, when you look at the results from FY ’25, we’ve shown that we can actually deliver strong productivity and strong EBITDA flow-through.” This defensive posture suggests management faces skepticism about their ability to reignite margin expansion.

The stock’s muted 2.5% decline understates the severity of the earnings miss, potentially reflecting low expectations or merger speculation. A 29.4% earnings shortfall would typically trigger a more severe selloff, but the relatively contained reaction at $16.32 suggests investors may have already priced in operational challenges or remain focused on potential strategic alternatives. The company’s zero-for-one beat rate over the last quarter—the only period with available track record data—establishes a worrying pattern of underwhelming execution relative to expectations.

The fundamental tension facing Albertsons centers on whether margin compression proves transitory or structural. Revenue growth capability appears intact despite weak identical sales, but the company’s ability to translate that growth into profits has clearly deteriorated. The interest expense burden will persist regardless of operational improvements, creating a higher hurdle for meaningful earnings expansion. Management’s productivity rhetoric must translate into tangible margin recovery for the fiscal 2026 guidance to prove credible.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.