|Rev $91.7M|Net Loss $1.4M

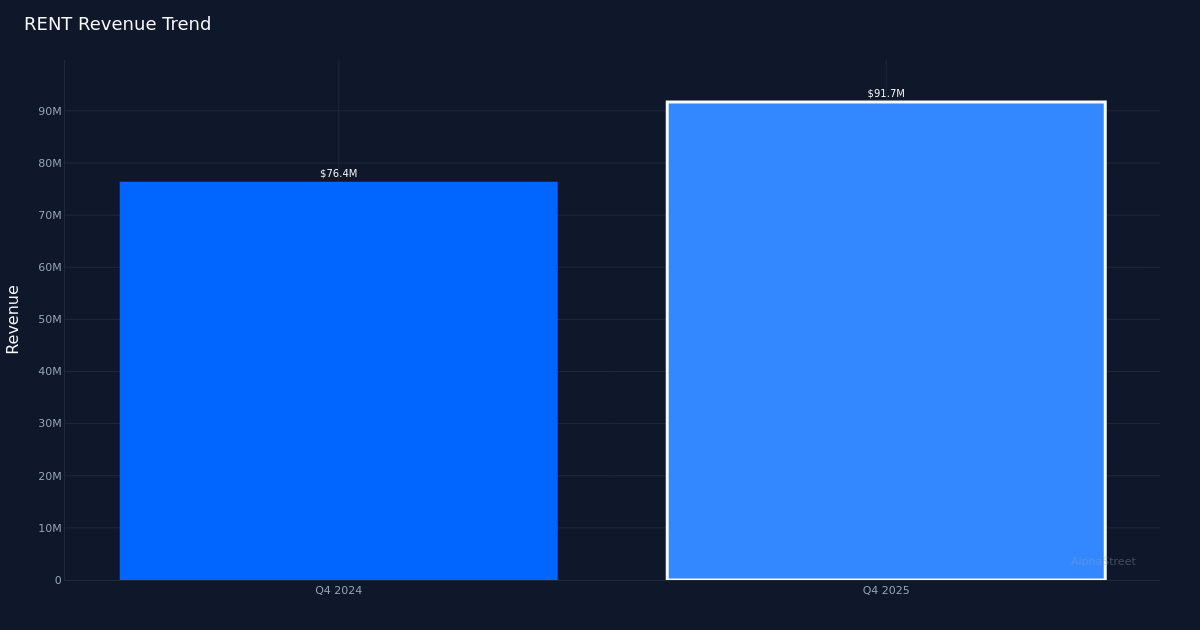

Rent the Runway, Inc. (NASDAQ: RENT) delivered a dramatic swing toward profitability in Q4 2025, narrowing its loss per share to $0.04 from $3.27 a year ago while crushing analyst expectations. The strong beat reflects fundamental operational improvement rather than financial engineering, as the apparel rental platform posted $91.7M in revenue—a 20.0% year-over-year surge—while simultaneously compressing net margin losses from negative 17.5% to negative 1.5%, a 16.0 percentage point improvement. This represents a rare combination in turnaround stories: accelerating top-line growth paired with margin improvement, suggesting the business model is approaching an inflection point toward sustained profitability.

The quality of this performance rests on genuine operational leverage rather than cost-cutting desperation. Gross margin reached 38.6% with gross profit of $35.4M, while operating loss came in at $1.5M. Adjusted EBITDA hit $18.3M, indicating meaningful cash generation capability despite a reported net loss of $1.4M. The 16.0 percentage point improvement in net margin versus Q4 2024 demonstrates that revenue growth is flowing through to the bottom line with increasing efficiency. This is revenue-driven margin expansion—the business is scaling profitably, not merely cutting to survive. The near-breakeven operating margin suggests the company stands within striking distance of positive operating profitability, a critical threshold for rental business models that carry heavy fixed costs in logistics and inventory management.

The revenue trajectory shows consistent acceleration with sequential momentum building. The $91.7M revenue represents a $4.1M increase from the prior quarter, translating to 4.7% sequential growth. The 20.0% year-over-year growth rate stands as particularly impressive given the company’s comparison against a less depressed prior-year base—Q4 2024 revenue of $76.4M wasn’t a pandemic trough. The limited four-quarter trend data shows Q4 2024 at $76.4M versus Q4 2025 at $91.7M, a clean 20.0% expansion that suggests the business has achieved genuine growth inflection rather than temporary promotional spikes.

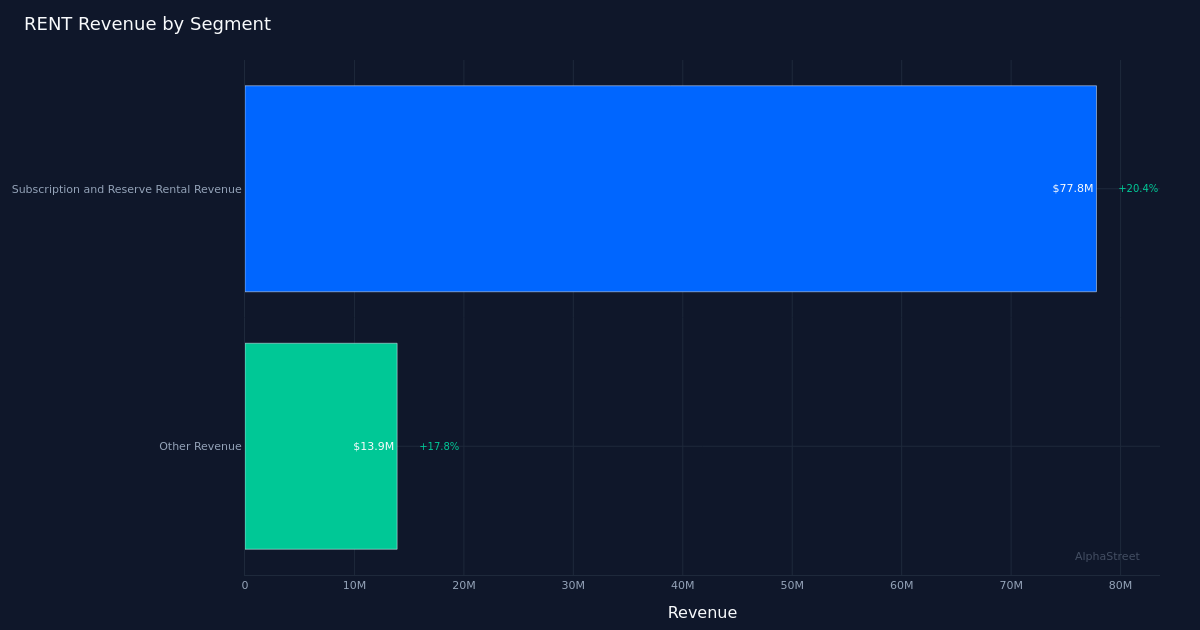

Segment dynamics reveal balanced growth across the core rental model and ancillary revenue streams. Subscription and Reserve Rental Revenue—the platform’s primary engine—generated $77.8M with 20.4% growth, while Other Revenue contributed $13.9M with 17.8% growth. Management attributed the core rental growth to structural improvements: “Subscription and reserve rental revenue was up $13.2 million, or 20.4% year-over-year in Q4 ’25, primarily due to higher average subscribers and higher average revenue per subscriber due to the subscription price increase effective August 1st, partially offset by lower reserve revenue versus Q4 ’24.” The commentary reveals a deliberate monetization strategy—the August price increase is flowing through to revenue per subscriber while the subscriber base itself expands to 143,796 Active Subscribers. Notably, the 17.8% growth in Other Revenue indicates the company is successfully diversifying beyond its primary offering.

The subscriber economics tell a compelling unit economics story. With 143,796 Active Subscribers generating $77.8M in Subscription and Reserve Rental Revenue over the quarter, the company demonstrates improving monetization. The price increase implemented on August 1st appears to have landed without triggering subscriber churn—subscriber counts grew while average revenue per subscriber expanded, the ideal outcome for a subscription business testing pricing power. This dual expansion validates the platform’s value proposition: customers are willing to pay more even as new cohorts continue joining.

The dramatic earnings beat versus expectations suggests the Street significantly underestimated the business transformation underway. The strong earnings beat reflects that the company is approaching profitability far faster than external observers modeled. This disconnect creates potential for multiple expansion if the company can sustain this trajectory and guide toward positive earnings in upcoming quarters.

The stock’s 2.7% initial gain to $5.79 represents a muted response given the magnitude of operational improvement. The modest uptick likely reflects either lingering skepticism about sustainability or technical constraints from the stock’s position in its trading range. For a company that just posted near-breakeven results while growing revenue 20.0%, the market reaction suggests considerable upside remains if management can demonstrate this isn’t a one-quarter anomaly but rather a new normalized performance level.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.