The COVID-19 pandemic has driven up sales for supermarket chains as people stock up on groceries and essentials. The Kroger Co. (NYSE: KR) is among those who benefited from this trend. The company’s investments in its brand portfolio and its digital channel as well as its focus on reducing costs have proven beneficial yet again.

Quarterly performance

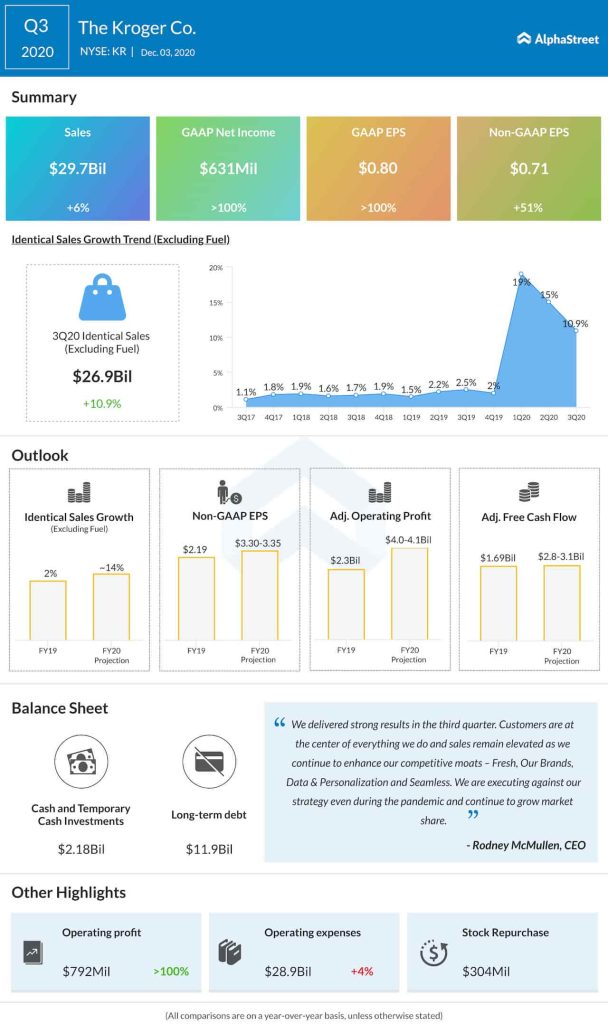

For the third quarter of 2020, Kroger delivered a 6% increase in total sales, which totaled $29.7 billion but came in shy of market projections. Adjusted EPS jumped 51% to $0.71 beating Street estimates. Same-store sales rose nearly 11%, with the meat and produce departments seeing significant growth.

Growth drivers

During the pandemic, Kroger managed to increase its market share and has seen rising demand for premium products. The company is seeing increased basket sizes as people have started to cook more meals at home.

Kroger is rolling out new products under its brands in categories like fresh soup, entrees, pizzas and sandwiches. The company is gaining market share in segments such as fresh produce, prepared foods and specialty cheese.

During the quarter, Kroger’s brands grew 8.6% and the company unveiled 250 new products in categories that are seeing rising demand such as fresh produce, frozen grocery and plant-based foods.

Another significant growth driver during the quarter is the digital channel. Kroger’s investments in its digital business and its efforts to improve its fulfillment network by taking advantage of its physical stores and rolling out new pickup and delivery options has proven beneficial.

Digital sales rose 108% during the third quarter, contributing approx. 4.6% to identical sales, ex fuel. The company’s network of more than 2,200 pick-up locations and 2,450 delivery locations helps it reach 98% of its customer base. Kroger will open two new fulfillment centers in Ohio and Florida in early 2021 to expand its delivery capabilities.

The majority of Kroger’s digital customers shop both in-store and online and they not only visit more often but also spend double on average compared to those who only shop at stores. The company believes its strong network will help drive growth even after the pandemic subsides. Digital sales was incrementally profitable and the company is focused on improving its digital profitability by increasing basket size, improving sales mix and reducing the cost of fulfilling orders.

Outlook

Kroger sees the trend of meals at home continuing throughout this year and has raised its full-year 2020 guidance in light of its strong sales and market share gains. The company expects identical sales, ex fuel, to increase around 14%. Adjusted EPS is estimated to grow approx. 50-53% to a range of $3.30-3.35. The retailer remains on track to achieve $1 billion in cost savings in 2020 under its Restock Kroger initiatives.

Stock

Kroger’s shares stayed in red territory on Friday as experts raised concerns that the gains seen by retailers during the pandemic are likely to slow down once things normalize in a post-COVID world. The increase in costs due to COVID-related expenditure for the rest of the year is another cause of worry. The stock has dropped 13% over the past three months.

Click here to read the full transcript of Kroger’s Q3 2020 earnings conference call