Shares of JM Smucker Co. (NYSE: SJM) have gained 7% over the past 12 months. The company continues to face challenges from inflation and supply chain disruptions and expects these pressures to continue in the near term. It continues to invest in its business and reshape its portfolio as part of its efforts to focus more on its high-growth categories.

Sales and demand

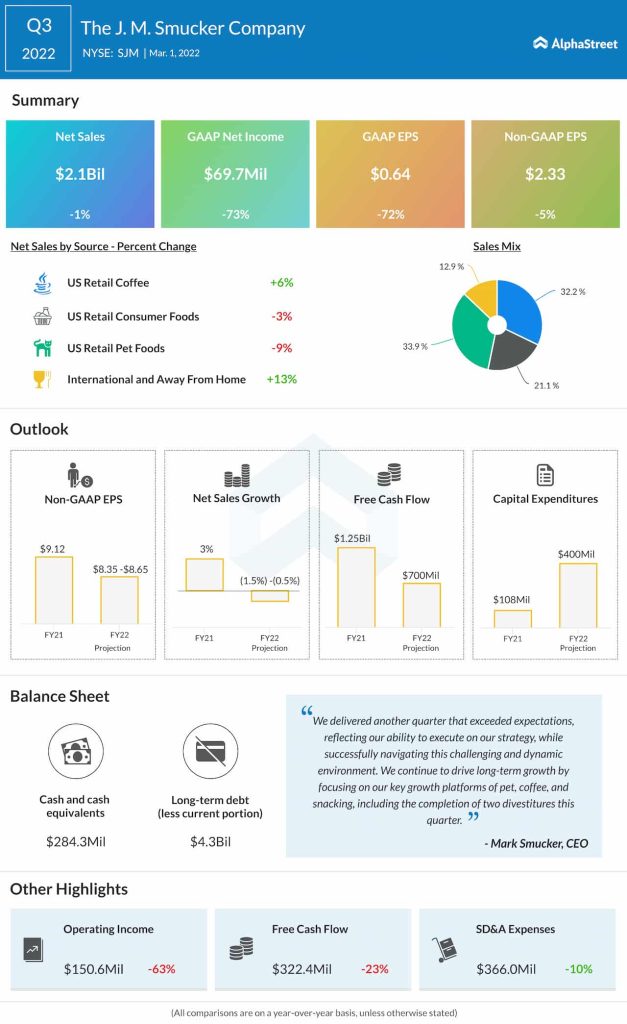

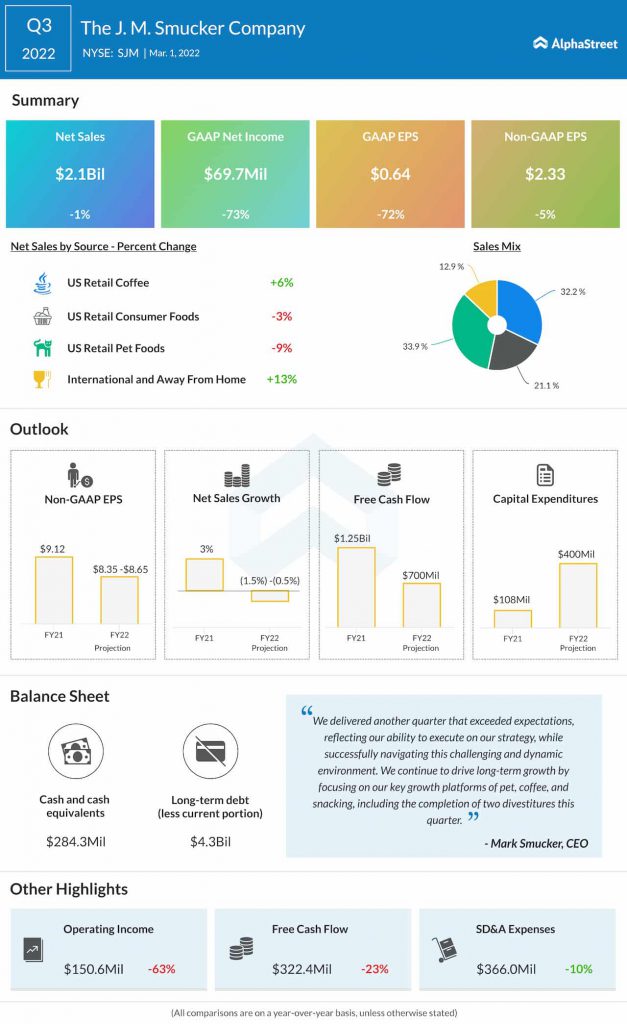

JM Smucker continues to see strong demand for its brands. While net sales decreased 1% during the third quarter of 2022, comparable sales increased 4%, driven by strong performance from the company’s leading brands in coffee, frozen sandwiches, pet snacks and cat food.

The company continues to revamp its portfolio. The divestitures of its Private Label Dry Pet Food business and Natural Beverage and Grains businesses in Q3 will help it focus more on the categories that have higher growth opportunities.

Within the Pet Foods business, growth in dog snacks and cat food was not adequate enough to offset declines in dog food which led to a comparable sales decline of 1%. As supply chain disruptions continue to hurt this business, JM Smucker is allocating supply and production to its more profitable brands, such as Meow Mix cat food.

Coffee saw sales growth of 6% with growth in all brands as the pandemic-fueled trend of at-home coffee consumption continued to stick. This growth was led by the Dunkin and Café Bustelo brands, which saw increases of 12% and 15% respectively in consumer takeaway.

The Consumer Foods business recorded comparable net sales growth of 4%, driven by a 30% growth in Uncrustables frozen sandwiches. Uncrustables is well on its way to becoming a $1 billion brand in annual net sales over the next five years as SJM continues to invest meaningfully in this brand.

For fiscal year 2022, SJM expects net sales to decline 1.5% to 0.5% from the previous year. Comparable net sales are expected to increase approx. 4.5% at the midpoint of the guidance range, reflecting momentum in brands and benefits from higher pricing actions.

Inflation and supply chain headwinds

During the third quarter, JM Smucker’s bottom line was hurt by higher costs. Supply chain and transportation constraints, along with labor shortages, impacted the company’s ability to fully meet demand. The bottom line will continue to be pressured due to the time lag between the pricing actions being implemented and taking effect.

In Q3, higher costs for commodities, manufacturing and transportation led to an 8% drop in adjusted gross profit and a 6% decrease in adjusted operating income. All these factors led to a 5% decline in adjusted EPS to $2.33.

SJM expects gross profit margin to be around 35% in FY2022 as higher cost inflation is expected to offset higher pricing and cost and productivity savings. Adjusted EPS for the full year is now expected to range between $8.35-8.65 versus the previous range of $8.35-8.75.

Click here to read the full transcript of JM Smucker’s Q3 2022 earnings conference call