Shares of General Mills, Inc. (NYSE: GIS) were down slightly on Wednesday despite the company delivering better-than-expected results for the first quarter of 2024. The stock has dropped 21% year-to-date and 19% over the past three months. Here are a few key points from the Q1 earnings report:

Results beat expectations

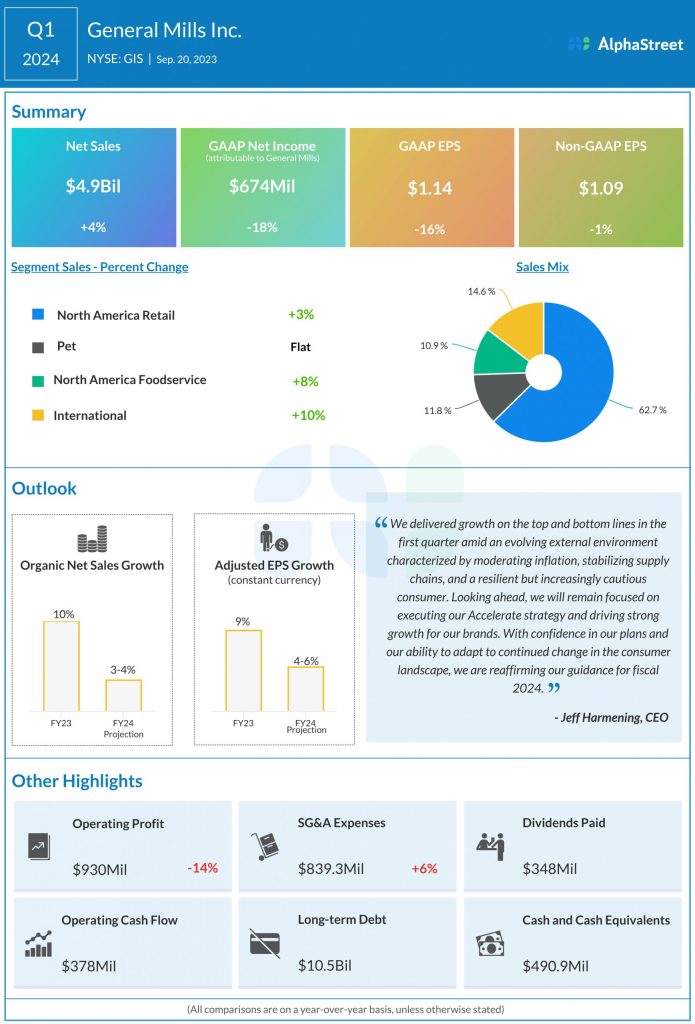

General Mills’ net sales increased 4% year-over-year to $4.9 billion in Q1 2024, beating estimates of $4.8 billion. Organic sales also grew 4%. The top line growth was driven by favorable price realization and mix but was partly offset by lower pound volume.

GAAP net income decreased 18% to $674 million while EPS declined 16% to $1.14. Adjusted EPS fell 1% in constant currency to $1.09 but managed to surpass projections of $1.08. Gross margin rose 540 basis points to 36.1%.

Category performance

In the first quarter, General Mills recorded sales growth across all of its segments except Pet, which remained flat compared to the prior-year period.

Within the North America Retail (NAR) Segment, retail sales growth for at-home food moderated from the levels seen in FY2023 but remained high compared to the pre-pandemic period. The NAR segment saw net sales growth of 3% in Q1. Sales grew 8% in US Snacks and 3% in US Morning Foods but dipped 1% in US Meals & Baking Solutions.

GIS also saw strong sales growth in its North America Foodservice and International segments, which together make up 25% of its global sales. In Q1, North America Foodservice sales rose 8% while International sales grew 10%. The Foodservice segment benefited from a rise in traffic in non-restaurant away-from-home food channels while the International segment gained from retail sales growth in ice cream, Mexican food, and snack bars.

Sales in the Pet segment remained flat in Q1 as economic uncertainty led to consumers looking for products that offer more value and opting for smaller pack sizes. With pet owners spending more time away from home, the pet treats and wet food segments remain challenged. In Q1, net sales rose in the mid-single-digits in dry food. Wet food remained roughly flat while treats saw a double-digit decline. There is more pressure on the premium category in particular.

Reaffirms outlook

General Mills expects its performance in fiscal year 2024 to be impacted the most by consumers’ economic health, the moderating rate of input cost inflation, and supply chain stability. The company expects input cost inflation for the year to be approx. 5% of total cost of goods sold. Based on these factors, GIS reaffirmed its outlook for FY2024. It expects organic sales growth of 3-4% and adjusted EPS growth of 4-6% in constant currency.