Chipmaker Micron Technology Inc. (NASDAQ: MU) is among the semiconductor firms most affected by the demand-supply imbalance the industry is witnessing, and the recent China sanctions have added to its problems. In the past year, Micron’s shares went through a series of ups and downs but maintained a modest uptrend. Earlier, MU had slipped to a two-year low after peaking in January last year.

China Ban

Micron suffered a setback earlier this year after the Chinese government imposed a ban on its memory and storage chips, impacting sales to several companies headquartered in China. Considering the company’s high exposure in that market, the ban will continue to have a negative impact on revenues. It is also affecting the company’s recovery from the pandemic-induced supply-chain disruption and the demand-supply gap.

Of late, there has been a dip in new orders, and that resulted in inventory buildup. While the management is taking measures to overcome the crisis, for the time being, the topline will likely remain under pressure since China and Hong Kong account for about a fifth of the company’s revenues. Meanwhile, Micron stands to benefit from the growing demand for AI-supported systems due to the extensive use of memory chips in them.

Q4 Report Due

Micron’s fourth-quarter earnings report is scheduled for release on September 27, after the closing bell. The bottom line is expected to remain in the negative territory this time too. Market watchers forecast a loss of $1.18 per share for the August quarter, excluding one-off items, compared to earnings of $1.45 per share in the fourth quarter of 2022. The bearish outlook reflects an estimated 41% fall in revenues to $3.91 billion.

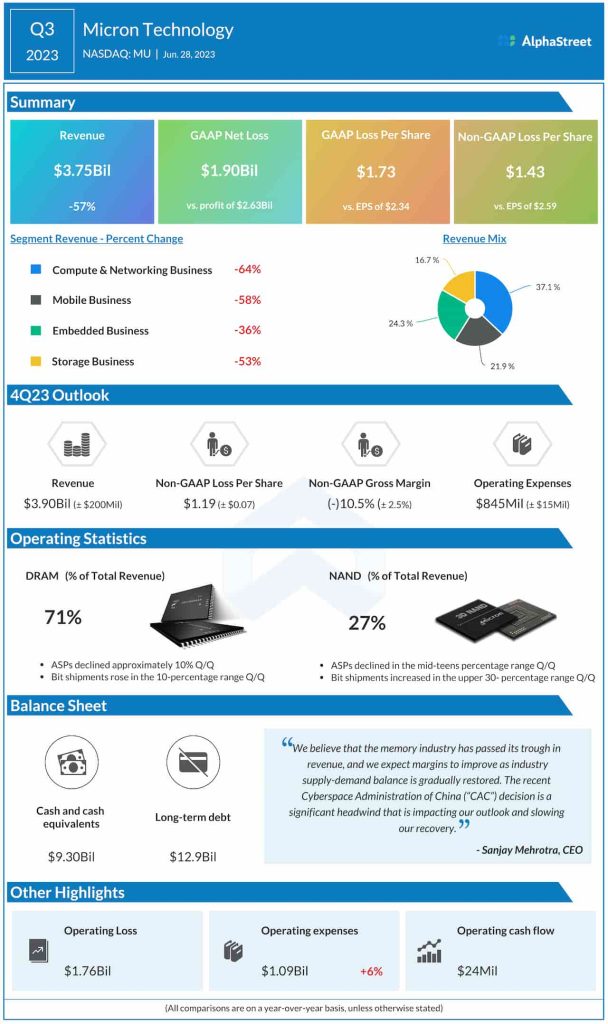

The guidance issued by the company a few months ago projects fourth-quarter revenues of approximately $3.90 billion and an adjusted net loss of $1.19 per share. The management is looking for an adjusted gross margin of around (-)10.5% and operating expenses of approximately $845 million.

“Market recovery can accelerate if there is further reduction in industry production and these cuts are sustained well into calendar 2024. In response to the industry environment, Micron has taken decisive actions to bring our supply back in balance with demand. We expect Micron’s year-on-year bit supply growth to be meaningfully negative for DRAM. We also expect to produce fewer NAND bits in calendar 2023 than in calendar 2022. Our fiscal 2023 CapEx plan of $7 billion is down more than 40% from last year, with WFE down more than 50%. We continue to expect fiscal 2024 WFE to be down year-on-year,” said Micron’s CEO Sanjay Mehrotra at the last earnings call.

Loss in Q3

In the most recent quarter, Micron incurred a third consecutive loss, but it was better than the outcome analysts had predicted. In the trailing two quarters, the bottom line missed estimates, reserving the long-term trend of consistent earnings beats. Third-quarter revenues declined a dismal 57% to $3.75 billion but exceeded Wall Street’s expectations. All four operating segments contracted in double digits.

On Wednesday, shares of Micron opened slightly above $70, which is up 42% from last year. They traded lower in the early hours of the session.