Shares of Hormel Foods Corporation (NYSE: HRL) turned green in midday trade on Thursday although the company delivered mixed results for the second quarter of 2025 and narrowed its guidance for the full year. While sales were up slightly compared to the year-ago period, earnings witnessed a decline. The branded foods provider anticipates strong growth in the second half of the year even as it faces a dynamic environment.

Revenue miss, earnings in-line

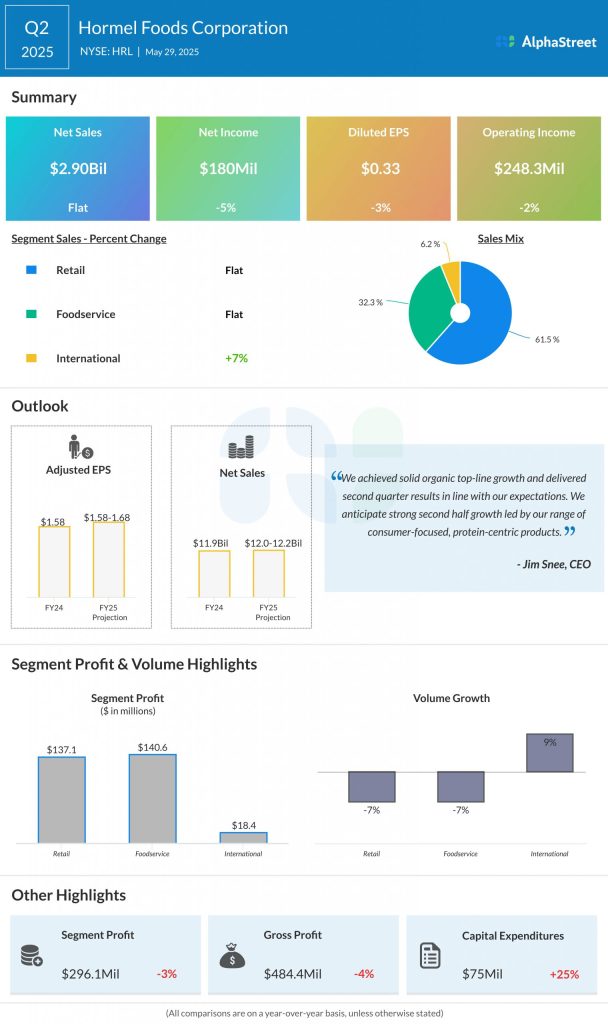

In the second quarter of 2025, Hormel’s net sales rose slightly year-over-year to $2.90 billion but narrowly missed estimates of $2.91 billion. GAAP earnings per share decreased 3% to $0.33. Adjusted EPS of $0.35 fell 8% YoY but was in line with estimates.

Business performance

Net sales in the Retail segment remained flat in Q2 as high-single-digit growth in the Mexican portfolio and value-added turkey products were offset by the impacts of promotional timing. Volume declined 7%, mainly due to lower commodity shipments and contract manufacturing. Flagship and rising brands performed well in the quarter, with gains from Planters and Jennie-O turkey.

The Foodservice segment saw net sales remain flat in the second quarter while organic sales grew 4%. Organic sales growth was broad-based with gains from the customized solutions business and the turkey portfolio. The company saw strong sales and volume growth for branded products like Jennie-O, Hormel Fire Braised meats, and Café H globally inspired proteins.

Volumes in the Foodservice division fell 7% while organic volumes were down 1%. Volumes grew in several categories despite industry softness, but this growth was offset by reduced commodity shipments.

The International segment posted 7% growth in sales and 9% growth in volume in Q2. The top line benefited from double-digit volume and sales growth in exports, and growth in China. The China business benefited from momentum in the retail and foodservice channels as well as innovative product launches.

Narrowed guidance

Hormel narrowed its guidance for fiscal year 2025. The company now expects net sales of $12.0-12.2 billion. Organic sales is expected to grow 2-3%, assuming growth across all segments, increased brand investments, and innovation. GAAP EPS is expected to be $1.49-1.59 while adjusted EPS is expected to be $1.58-1.68.