Shares of Southwest Airlines Co. (NYSE: LUV) plunged 9% on Thursday after the company delivered mixed results for the second quarter of 2023. Revenue beat expectations but earnings fell short. The stock has dropped 13% over the past 12 months. Here’s a look at the key takeaways from the earnings report:

Mixed results

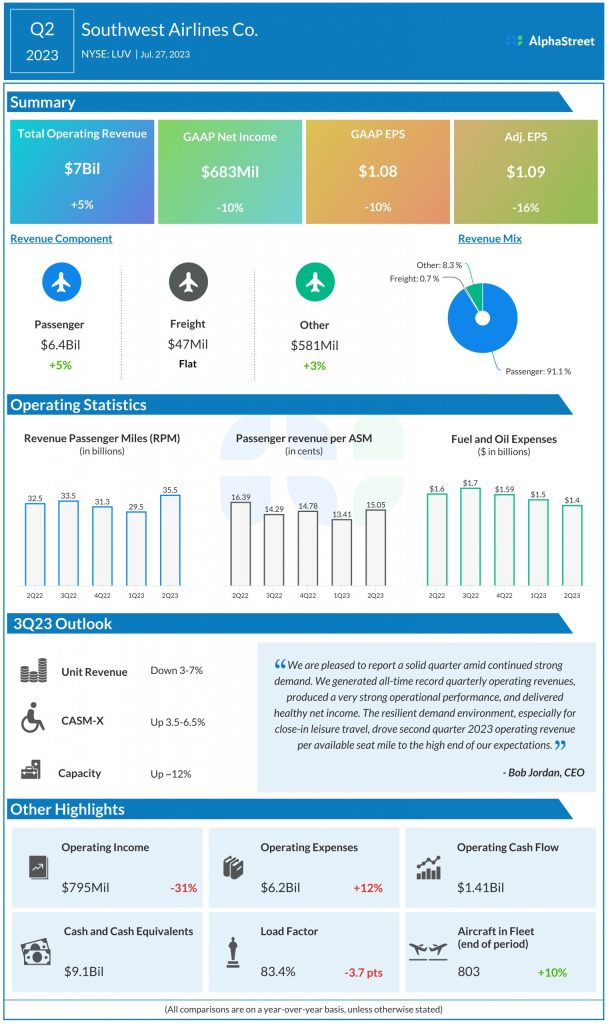

Southwest reported total operating revenue of $7 billion in Q2 2023, which was up 5% year-over-year and ahead of estimates of $6.9 billion. GAAP net income declined 10% YoY to $683 million, or $1.08 per share. Adjusted EPS fell 16% to $1.09, missing projections of $1.10.

Trends

Southwest continued to see strong demand, especially for leisure travel. Managed business revenues improved sequentially helped by growth in corporate accounts and passengers. Managed business revenues are seeing a recovery but are not yet at pre-pandemic levels.

Revenue per available seat mile (RASM), or unit revenues, decreased 8.3% in Q2. Passenger unit revenues were down 8.2%. Traffic was up 7.5% while capacity was up 14.1%. Load factor was 83.4%. Cost per available seat mile, excluding fuel and oil expense, special items, and profit-sharing expense (CASM-X) was up 7.5% in Q2.

Southwest said its network is largely restored but not yet optimized. The company anticipates its network optimization efforts to support margin expansion in the coming year.

“We are working to align our network, fleet plans, and staffing to better reflect the current business environment. While business revenues continue to recover, they are not back to pre-pandemic levels—therefore, we are revamping our 2024 flight schedules to reflect post-pandemic changes to Customer travel patterns. We estimate these meaningful network optimization efforts and the continued maturation of our development markets will contribute roughly $500 million in incremental year-over-year pre-tax profits in 2024, which we believe will support another year of margin expansion.” – CEO Bob Jordan

Outlook

For the third quarter of 2023, Southwest expects unit revenues to be down 3-7% and capacity to be up around 12% year-over-year. CASM-X is expected to be up 3.5-6.5% YoY while economic fuel costs per gallon are estimated to range between $2.55-2.65.

For the full year of 2023, capacity is expected to be up 14-15% YoY. CASM-X is expected to be down 1-2% while economic fuel costs per gallon are projected to be $2.70-2.80.