Kroger reported financial results for the fourth quarter and full fiscal year 2025, delivering an earnings beat despite softer sales as the grocery chain continues to navigate a price sensitive consumer environment. Strong digital growth and increased demand for private label products helped support profitability during the quarter.

Revenue and Sales Trends

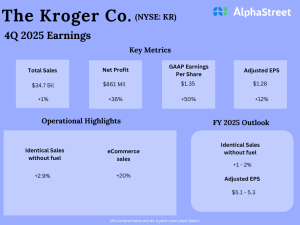

For the fourth quarter of fiscal 2025, Kroger reported:

-

Total sales: $34.73 billion

-

Identical sales (excluding fuel): modest growth, reflecting continued demand for grocery staples

-

Digital sales: up about 20% year over year, driven by strong pickup and delivery demand through partners such as Instacart, DoorDash, and Uber Eats.

The grocery sector continues to benefit from the “eat-at-home” trend, where consumers prepare meals at home more frequently due to higher restaurant prices and economic uncertainty.

However, competition from large retailers such as Walmart and Target has intensified price pressure across the industry.

Earnings and Profitability

Kroger delivered stronger-than-expected earnings in the quarter:

-

Adjusted EPS: $1.28 per share, beating analyst expectations of about $1.20.

Profitability benefited from:

-

Strong private-label product sales

-

Improved cost discipline

-

Continued expansion of higher-margin digital and media businesses.

Despite the earnings beat, revenue performance was slightly below market expectations due to cautious consumer spending patterns.

Full Year FY2025 performance

For the full fiscal year 2025, Kroger maintained stable performance despite macroeconomic headwinds.

Key metrics include:

-

Annual revenue: approximately $147 billion

-

Net income: roughly $2.67 billion

-

Continued growth in digital sales and private-label brands.

The company has also been investing in alternative profit businesses, including retail media and data analytics, which generate higher margins compared with traditional grocery retail.

Strategic Initiatives and Operational Focus

Kroger continues to focus on several strategic priorities:

Digital and e-commerce expansion

The company is increasing investment in digital grocery ordering and delivery partnerships, which have become a critical channel for growth.

Private Label products

Kroger’s store brands remain a key driver of customer loyalty, particularly among value conscious shoppers.

Operational efficiency

Management is streamlining operations and optimizing its fulfillment network to improve profitability and reduce costs.

These initiatives are designed to help Kroger maintain market share in a highly competitive grocery market.

Management Commentary

Management acknowledged that consumers remain price sensitive due to inflation and economic uncertainty.

The company is responding by:

-

Expanding promotions and loyalty programs

-

Increasing private label offerings

-

Improving value perception across its stores.

Leadership also emphasized that digital grocery services and retail media platforms represent long-term growth opportunities for the business.

Outlook

Kroger provided guidance for fiscal 2026:

-

Identical sales growth (excluding fuel): 1%–2%

-

Adjusted EPS: $5.10–$5.30.

The outlook reflects expectations of modest growth as the company continues to manage competitive pricing pressures and changing consumer spending patterns.

Key Takeaways

1. Earnings resilience despite sales pressure

Kroger continues to deliver profit growth even as revenue growth remains modest.

2. Digital grocery becoming a core growth engine

Pickup and delivery services are driving strong digital sales growth.

3. Private Label strategy strengthening margins

Store brands provide higher margins and help retain value-focused customers.

4. Competitive grocery environment intensifying

Price competition from large retailers and discount chains remains a key challenge.

Bottom Line

Kroger’s Q4 FY2025 results demonstrate the company’s ability to maintain profitability in a competitive grocery market, supported by strong digital growth and private-label sales. While revenue growth remains modest, Kroger’s focus on operational efficiency, digital expansion, and value-oriented offerings positions the retailer for steady performance in fiscal 2026.

To view the company’s previous earnings and latest concall transcripts, click here to visit the Alphastreet news channel.