Ladder Capital Corp (NYSE: LADR) shares fell 4.48% on Thursday closing at $10.56. The decline followed the release of the company’s Q4 and full-year 2025 financial results, which missed analyst estimates for both revenue and earnings. The stock traded between an intraday high of $11.03 and a low of $10.53.

Market Capitalization

As of the market close on February 5, 2026, Ladder Capital Corp had a market capitalization of approximately $1.35 billion.

Latest Quarterly Results

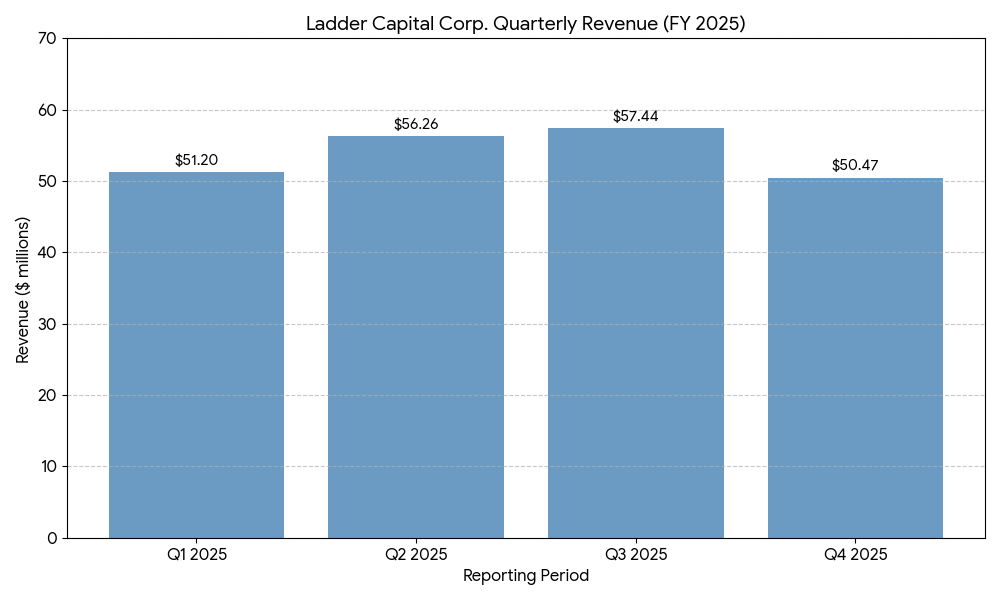

For the quarter ended December 31, 2025, Ladder Capital reported consolidated revenue of $50.47 million, a 26.4% decrease compared to $68.62 million in the prior-year period. Net income for the quarter was $15.9 million, or $0.13 per diluted share. Distributable earnings, a non-GAAP measure, were $21.4 million, or $0.17 per share, compared to $0.27 per share in the fourth quarter of 2024.

Q4 Segment Highlights

• Lending: Net interest income totaled $22.3 million, down from $27.2 million in the year-ago quarter. The company’s total loan portfolio carrying value was $2.20 billion with a weighted average yield of 7.7%.

• Real Estate: Real estate operating income was $25.1 million, compared to $23.4 million in the fourth quarter of 2024.

• Investment Securities: The company reported $433 million in loan originations during the quarter.

Full-Year Results Context

For the full year 2025, Ladder Capital reported total revenue of $215.4 million and a net profit of $64.2 million or $0.51 per share. Distributable earnings for the year were $109.9 million or $0.84 per share. Financial data for the fiscal year indicated a contraction in annual revenue and distributable earnings compared to 2024 results.

Business & Operations Update

In 2025, Ladder Capital achieved investment-grade credit ratings of Baa3 from Moody’s and BBB- from Fitch Ratings. The company reported the expansion of its access to the unsecured corporate bond market and a reduction in its overall cost of capital. Operational focus remained on its diversified commercial real estate (CRE) investment strategy, primarily originating fixed and floating-rate first mortgage loans.

The company closed over $250 million in new loans from January 1 through February 4, 2026. Ladder Capital also maintained liquidity of $608 million, including $570 million of undrawn revolver capacity, and continued its stock repurchase program with $90.6 million available at year-end.

Capital Structure Update

As of December 31, 2025, Ladder Capital reported an undepreciated book value per share of $13.69. The company’s total loan portfolio stood at $2.20 billion. The capital structure remains diversified across an unencumbered asset pool and unsecured debt. The company’s CECL (Current Expected Credit Losses) allowance was reported at $0.37 per share.

Equity Analyst Commentary

Institutional research notes attributed the stock’s downward movement to a miss in net interest income and a decline in the weighted average yield of the portfolio. Zacks Equity Research noted that the fourth-quarter distributable EPS of $0.17 missed the consensus estimate of $0.23, representing a negative earnings surprise. Analysts highlighted that while the company has outperformed the broader market year-to-date, the immediate price movement was impacted by the deviation from quarterly revenue expectations.

Guidance & Outlook

Management indicated that the company enters 2026 with more than $400 million of additional loans in its pipeline. Monitoring factors for the upcoming year include the pace of loan originations, the impact of the newly acquired investment-grade status on capital allocation, and the stabilization of interest rate spreads within the CRE lending environment.

Performance Summary

Ladder Capital shares closed 4.48% lower today at $10.56. The company reported a 26.4% year-over-year decline in fourth-quarter revenue to $50.47 million and a distributable EPS miss of $0.17 against estimates. Lending segment income contracted, while real estate operating income saw a marginal increase. The company maintains an investment-grade rating and a pipeline of $400 million in prospective loans.