The recent financial performance of Levi Strauss & Co. (NYSE: LEVI) shows the company has effectively navigated macroeconomic uncertainties and inflationary pressure. After shrugging off COVID-related headwinds, the casual clothing retailer got back on track quickly, supported by strong customer demand across all business segments and geographical regions.

But the uptrend is yet to reflect on the performance of the San Francisco-based denim giant’s stock, which has remained on a losing streak for more than a year now. Meanwhile, the market’s indifference to last week’s positive second-quarter results can be linked to the muted performance of the overall stock market. LEVI’s value has nearly halved since peaking early last year. The compelling valuation, combined with the management’s initiatives to enhance shareholder value through share repurchase and strategic M&A deals make the stock a good bet.

Buy LEVI?

Market watchers are quite bullish on LEVI, and the impressive target price underscores the positive view. In short, it is a good time to buy the stock now because profitability is on an upward trajectory and cash flows are quite healthy. With the worst of the pandemic almost over, consumers are once again adding discretionary items like clothes and footwear to their shopping list. That is good news for Levi Strauss’ shareholders.

Read management/analysts’ comments on Levi Strauss’ Q2 2022 earnings

Of late, there have been strong efforts to ramp up the e-commerce platform and strengthen the direct-to-customer channel, which contributes significantly to sales. It was the company’s digital capabilities that enabled it to recover rather quickly from the slowdown experienced soon after the onset of the pandemic.

Levi Strauss CEO Chip Bergh said in a recent interaction with analysts: “Our e-commerce business remains healthy, with revenue continuing to far exceed pre-pandemic levels. We did see a moderation in online traffic as consumers returned to shopping in our stores in large numbers. E-commerce remains an important driver of our growth algorithm, and we are committed to tripling its size over the next five years after successfully growing e-commerce into nearly a $0.5 billion business over the last decade.”

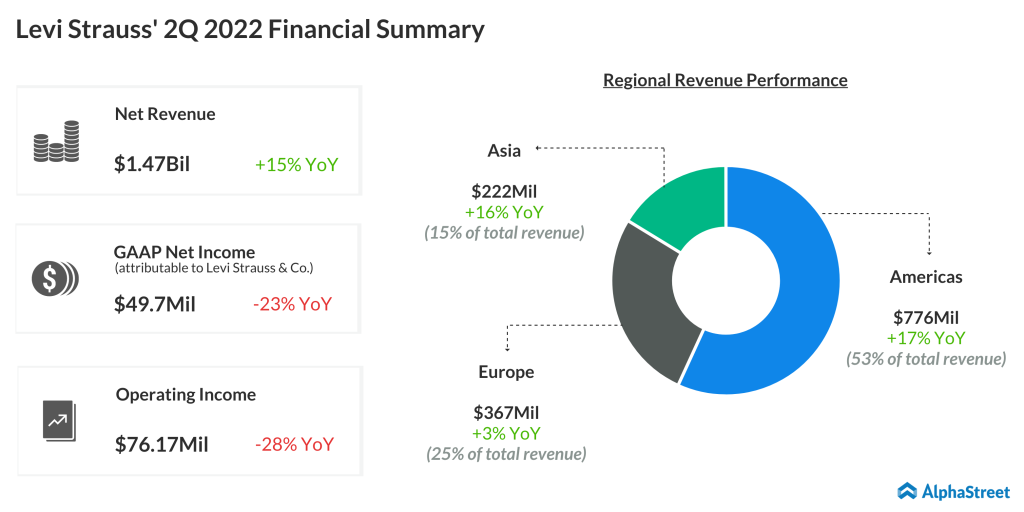

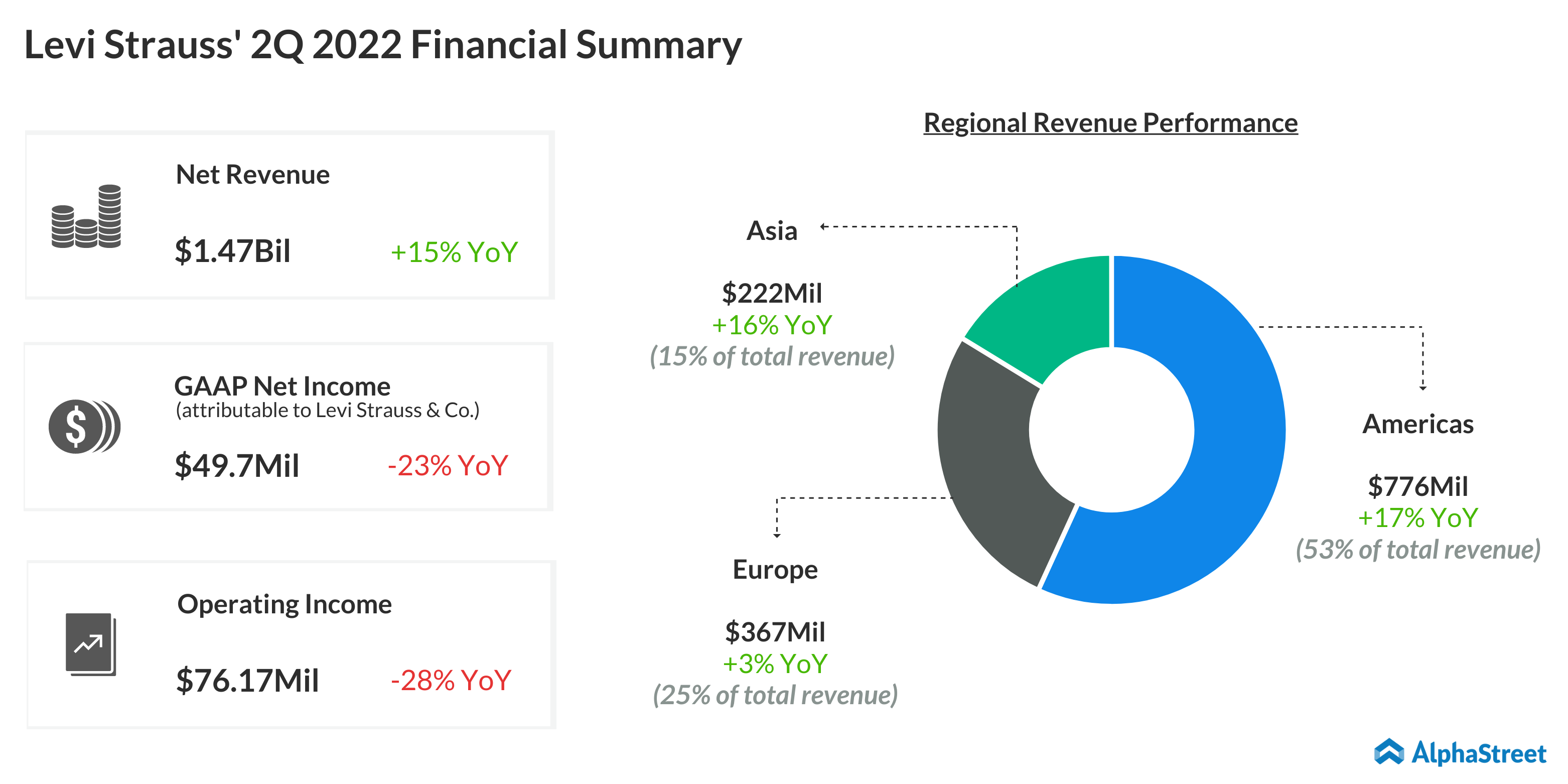

Reflecting double-digit growth across all the key geographical segments, Levi Strauss’ second-quarter revenues rose 15% annually to $1.47 billion, which also surpassed the market’s expectations. Consequently, adjusted profit moved up to $0.29 per share from $0.23 per share in the corresponding period of 2021.

Key Data

The top line continues to benefit from the brand-led, direct-to-customer business model and diversified portfolio. The management has reaffirmed the full-year guidance while stressing its commitment to consistently creating value for shareholders. Interestingly, the company has an impressive track record of generating better earnings than widely expected.

Highlights of Levi Strauss’ Q1 2022 financial report

In a move aimed at diversifying the business, Levi Strauss last year acquired Beyond Yoga, marking its foray into the activewear segment. The deal helped the company expand its women’s wear footprint and allocate global resources and the digital ecosystem to further grow the Beyond Yoga brand.

Risks

But no business is immune to the lingering macro uncertainties and geopolitical issues. Going forward, consumer sentiment would largely depend on economic recovery and easing of inflation pressure. A key risk facing Levi Strauss is that customers are likely to cut down spending on non-essential items when their purchasing power is squeezed. Another concern is the supply chain crisis facing the broad retail sector.

Levi Strauss’ stock this week slightly recovered from a two-year low but continued to trade below its 52-week average. It has lost about 33% since the beginning of the year.