Shares of McCormick & Company Inc. (NYSE: MKC) stayed red on Wednesday. The stock has gained 23% over the past three months. The spices and condiments manufacturer is scheduled to report its third quarter 2024 earnings results on Tuesday, October 1, before markets open. Here’s what to expect from the earnings report:

Revenue

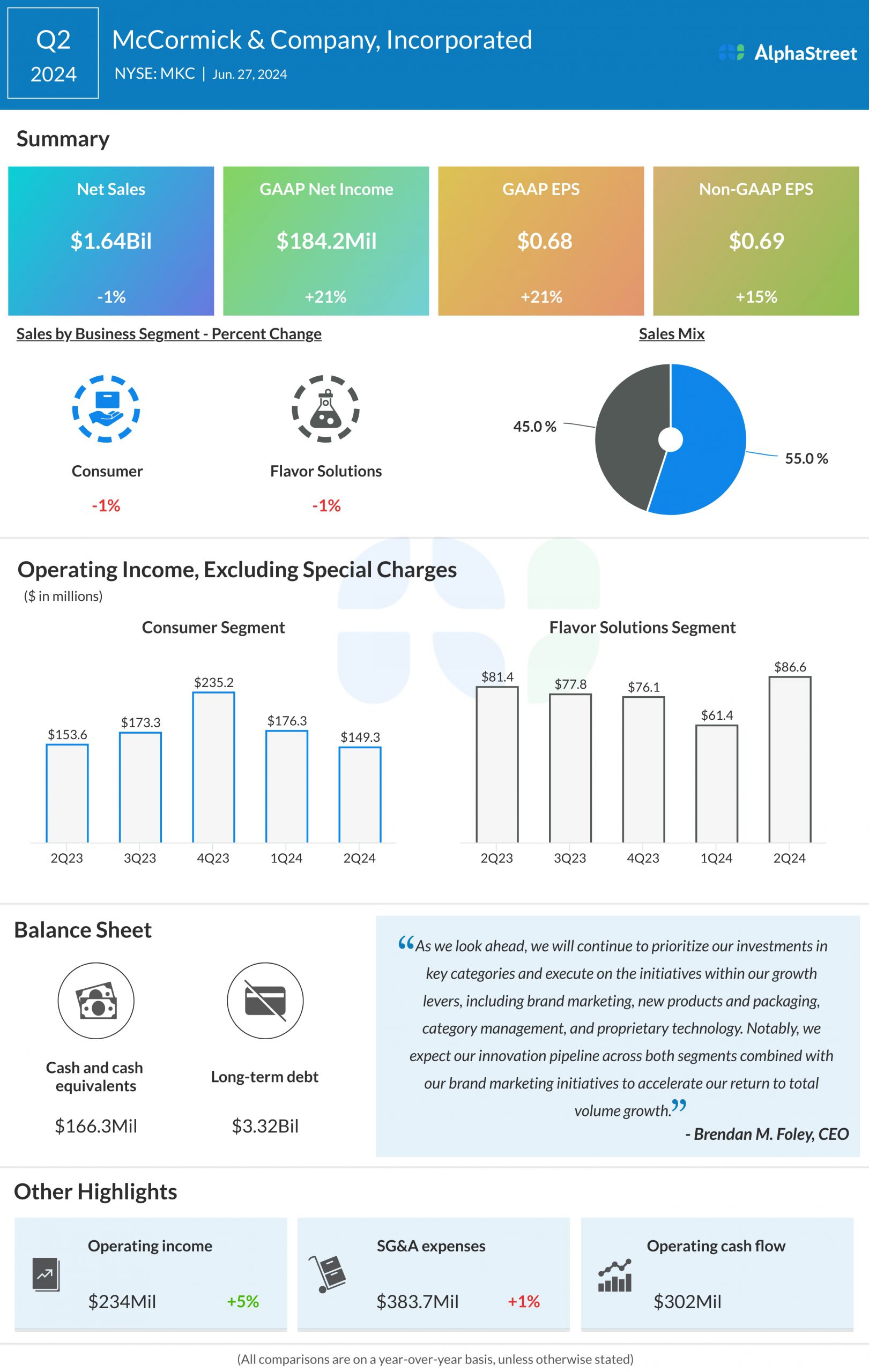

Analysts are projecting revenue of $1.67 billion for McCormick in the third quarter of 2024. This represents a slight dip from $1.68 billion reported in the same period a year ago. In the second quarter of 2024, sales dropped 1% year-over-year to $1.64 billion.

Earnings

The consensus estimate for EPS in Q3 2024 is $0.67, which represents an increase from adjusted EPS of $0.65 reported in Q3 2023. In Q2 2024, adjusted EPS rose 15% YoY to $0.69.

Points to note

Against an inflationary backdrop, consumers continue to seek value. They are purchasing only essentials and are cooking more meals at home. As fewer people opt to dine out, restaurant traffic, especially in quick service restaurants (QSRs) has seen a slowdown.

These trends led to declines in McCormick’s sales and volumes in the second quarter. Volume growth in the Consumer segment was offset by volume declines in the Flavor Solutions segment, which was impacted by softness in QSR and packaged food customers’ volumes.

However, the company’s investments in its Consumer segment have been paying off and they are expected to help drive volume improvement for the division in the latter half of 2024. Volume growth in core categories is helping to offset the declines in prepared foods categories, like frozen.

McCormick is expected to benefit from its broad and diversified product portfolio that allows it to cater to changing consumer preferences. At-home food consumption has driven demand for categories like spices and seasonings, condiments, and sauces.

The seasonings-maker anticipates a pickup in volumes in the back half of the year for its Flavor Solutions segment as well, driven meaningfully by product innovation. New products are expected to be a material contributor to top line growth in the latter half of the year.

Last quarter, McCormick’s gross margin expanded by 60 basis points, helped by cost savings from its Comprehensive Continuous Improvement (CCI) program. The CCI and GOE programs are expected to help in generating cost savings and driving margin expansion for the full year, which could benefit the third quarter as well.