Shares of Lowe’s Companies, Inc. (NYSE: LOW) stayed green on Wednesday. The stock has gained over 9% in the past three months. The home improvement retailer delivered mixed results for the second quarter of 2024 and lowered its outlook for the full year due to persistent macroeconomic challenges. Here are a few points to note about its performance in Q2:

Mixed results

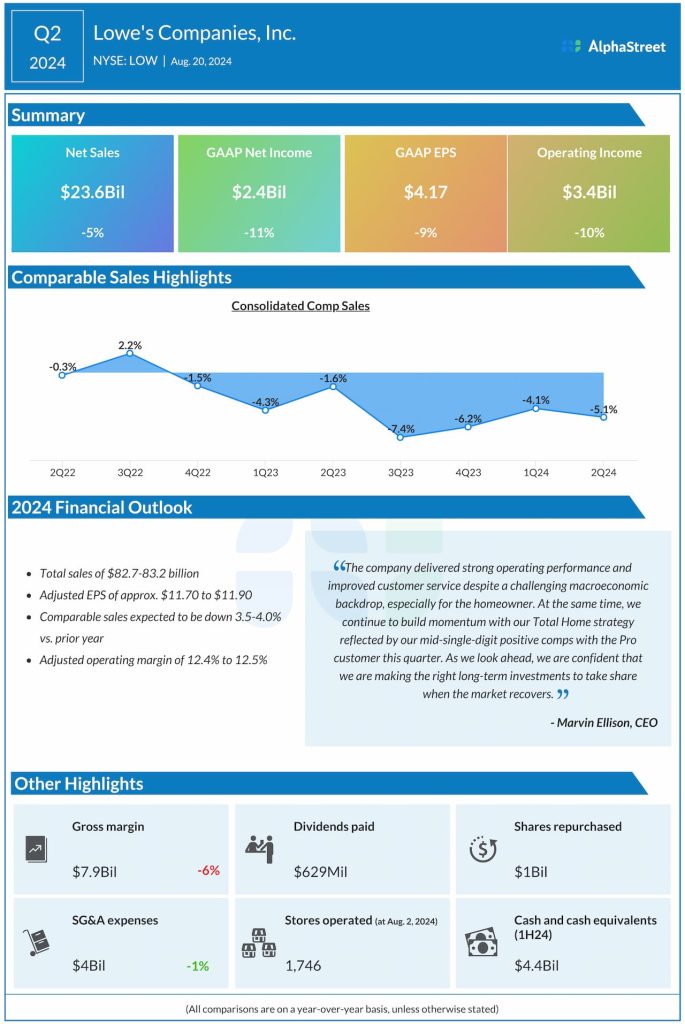

Lowe’s net sales in Q2 2024 decreased 5% year-over-year to $23.6 billion and missed expectations. Comparable sales decreased 5.1% due to pressure in DIY big ticket discretionary spending, and adverse weather impacting seasonal and outdoor category sales. GAAP EPS decreased 9% to $4.17 compared to last year. Adjusted EPS amounted to $4.10, which surpassed projections.

Pressure in DIY, strength in Pro

During the quarter, Lowe’s continued to see softness in DIY demand, particularly in bigger ticket discretionary projects. In addition, harsh weather conditions negatively impacted sales in seasonal and other outdoor categories.

Meanwhile, the company delivered mid-single-digit positive comps in the Pro segment in Q2, as it continues to gain traction with its small to medium-sized Pro customers. On its quarterly conference call, Lowe’s said that as per a recent survey, the backlogs of its Pro customers remain healthy and consistent with last year. It also indicated that 75% of pros are confident in landing new business.

Comparable average ticket inched up 0.8% in Q2, helped by strength in Pro-heavy categories. Comparable transactions declined 5.9%, due to pressure on DIY spend and lower seasonal transactions. This drop was partly offset by a rise in Pro transactions.

During the quarter, Lowe’s achieved positive comps in categories such as building materials and rough plumbing. The weakness in DIY discretionary projects impacted categories like flooring, kitchen, and bath. Adverse weather negatively impacted categories like lawn and garden.

Guidance cut

Lowe’s lowered its outlook for the full year of 2024 against a challenging home improvement backdrop and weak consumer sentiment. It now expects total sales of $82.7-83.2 billion versus the previous range of $84-85 billion. Comparable sales are now expected to decline 3.5-4.0% as opposed to the prior expectation of a decline of 2-3%. Adjusted EPS is now expected to range between $11.70-11.90 versus the previous range of $12.00-12.30.