Shares of Lowe’s Companies, Inc. (NYSE: LOW) stayed red on Friday. The stock has gained over 8% in the past three months. The home improvement retailer saw sales and earnings grow in the fourth quarter of 2025 versus the previous year. However, it remains guarded in its outlook for the upcoming fiscal year as housing market challenges show no sign of abatement.

Q4 performance

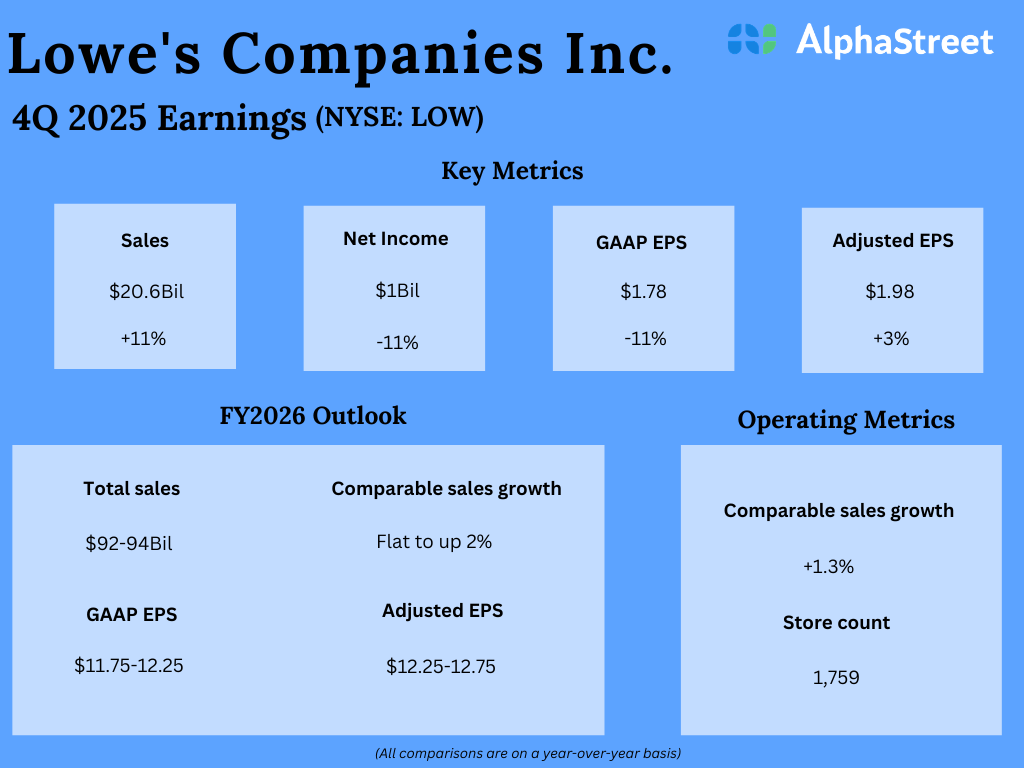

Lowe’s total sales increased 11% year-over-year to $20.6 billion in the fourth quarter of 2025. Comparable sales grew 1.3%, driven by growth in Pro, online, and home services sales. Comps also benefited from a strong holiday season as well as winter storm activity. On an adjusted basis, earnings increased 2.6% to $1.98 per share.

As mentioned on the quarterly call, winter storm-related demand boosted comp sales by approx. 50 basis points in Q4. Comps were positive in November, helped by early holiday season gains, and following a dip in December, they rebounded to nearly 6% in January, fueled by storm-related demand. Comparable average ticket rose 3.6%, driven by higher prices and a mix into Pro and appliances, although comparable transactions were down 2.3%.

Lowe’s online sales grew 10.5% in Q4, with record gains during the holiday season on Black Friday and Cyber Monday. Home services saw high single-digit growth during the quarter.

Also Read: Key metrics from Lowe’s (LOW) Q4 2025 earnings results

Continued housing market pressures

The housing market remains pressured as inflation and higher mortgage rates continue to weigh on affordability. Although consumer spending has remained resilient, consumers are still reluctant to make big-ticket discretionary purchases. As high mortgage rates continue to pressure home sales and new home starts, Lowe’s expects a pickup in housing and home improvement markets to take time.

On the other hand, higher home prices and an aging housing stock are likely to drive demand for home repairs and remodels. The rising need for new homes is also expected to drive pent-up demand when the market improves. Lowe’s forecasts the home improvement market to be roughly flat in a range of down 1% to up 1% in 2026.

Outlook

Lowe’s outlook for fiscal year 2026 reflects the ongoing uncertainty in the home improvement market. The company expects total sales to be $92-94 billion, representing a YoY increase of approx. 7-9%. The ADG and FBM acquisitions are expected to contribute approx. $8 billion to sales. Comparable sales are expected to be flat to up 2% versus the previous year. GAAP EPS is expected to be $11.75-12.25 and adjusted EPS is expected to be $12.25-12.75.