Lyft Inc. (NASDAQ: LYFT) reported a wider loss in the second quarter due to stock-based compensation and related payroll tax expenses, primarily due to RSU expense recognition in connection with its initial public offering.

The bottom line was narrower than the analysts’ expectations while the top line exceeded consensus estimates. Further, the company guided third-quarter revenue above the Street’s view and raised its revenue guidance for the full year 2019. Following this, the stock advanced over 10% in the after-market session.

Net loss was $644.24 million, wider than a loss of $178.9 million in the previous year quarter. On a per-share basis, the loss narrowed to $2.23 from $8.48 a year earlier due to the higher weighted average number of shares outstanding. Adjusted loss per share improved to $0.68 from $8.37 a year ago.

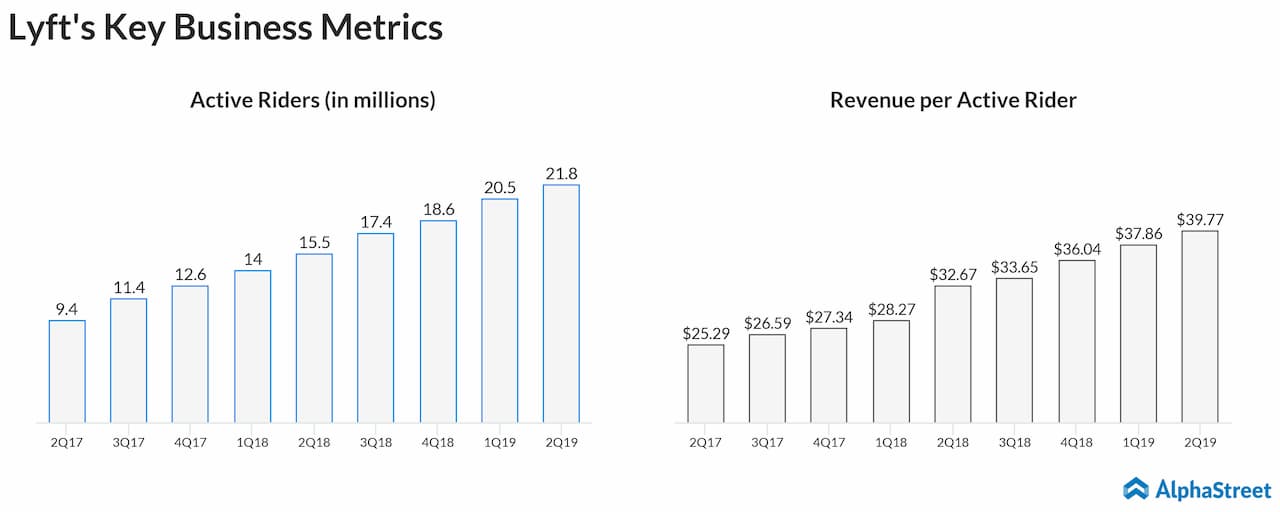

However, revenues climbed by 72% to $867.3 million, driven by better-than-expected active rider growth and revenue per active rider monetization. Active riders jumped by 41% year-over-year and revenue per active rider grew by 22%.

For the third quarter, Lyft expects total revenues to grow by 54-56% to the range of $900 million to $915 million and an adjusted EBITDA loss of $190 million to $210 million.

For fiscal 2019, the company lifted revenue outlook to the range of $3.47 billion to $3.5 billion from the previous range of $3.275 billion to $3.3 billion. The annual revenue growth rate is raised to the range of 61% to 62% from the prior range of 52% to 53%. Adjusted EBITDA loss guidance is narrowed to the range of $850 million to $875 million from the earlier estimate range of $1.15 billion to $1.175 billion.

Also read: Ford Motor Q2 earnings review

For the second quarter, Lyft reported an 88% jump in contribution to $398.9 million from the previous year quarter. Contribution margin increased to 46% from 42.1% a year ago.

The company said it remained focused on reshaping transportation and is pleased with the continued improvement in market conditions. This environment along with its execution is translating to strong revenue growth and sales and marketing efficiencies. As a result of this positive momentum, Lyft anticipates 2019 losses to be better than previously expected and updated its outlook.

Lyft’s rival Uber Technologies (NYSE: UBER) will be reporting its second quarter earnings results on Thursday after the market close. Analysts expect the company to report a loss of $3.20 per share on revenue of $3.39 billion for the second quarter.

Shares of Lyft ended Wednesday’s regular session up 2.71% at $60.29 on the Nasdaq. The stock has risen over 1% in the past three months while it has fallen over 22% since the IPO.